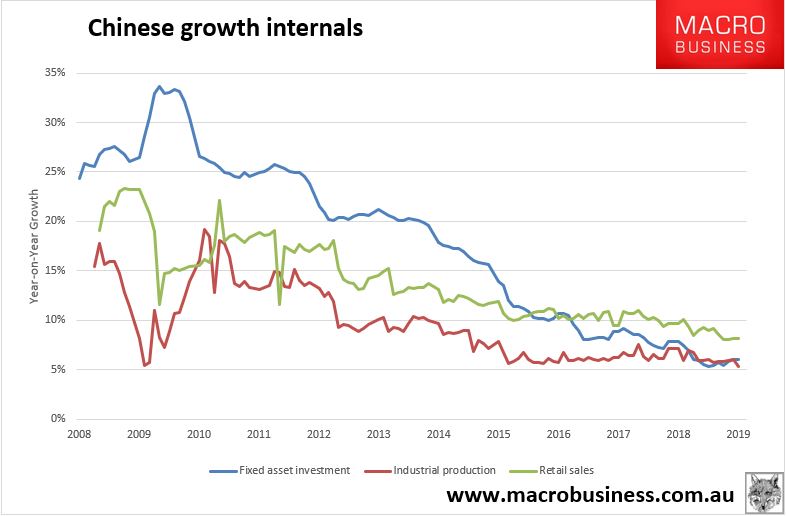

China dumped its Jan/Feb growth data this afternoon. It is staggering. The headline numbers were pretty hum drum with with fixed asset investment at 6.1%, industrial production at 5.3% and retail sales at 8.2%:

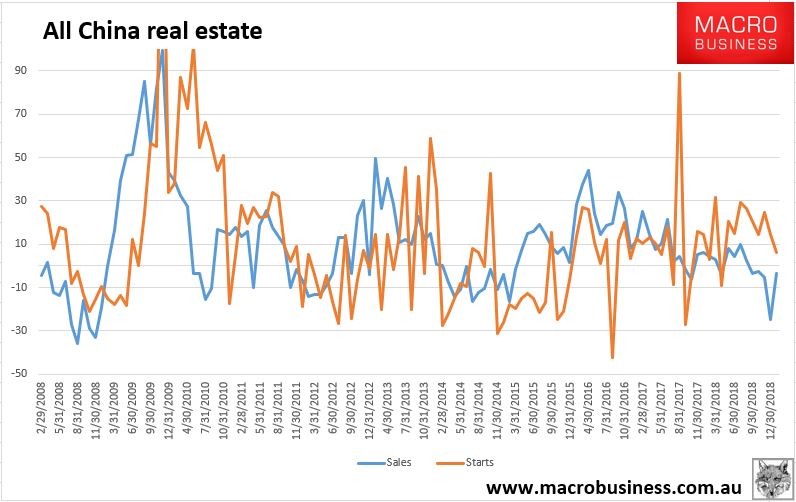

Under the bonnet, the all important real estate sector remains a mixed bag with sales still down 3.6% year on year though improved from December’s big fall:

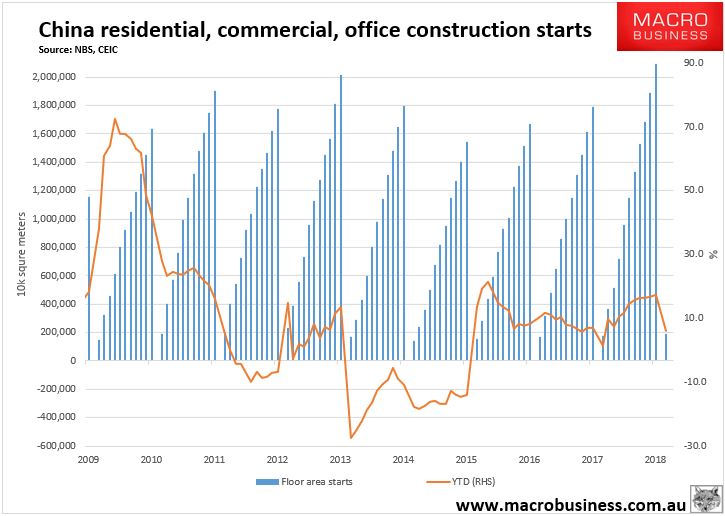

Yet floor starts continue to pile it on regardless, up 6% year on year:

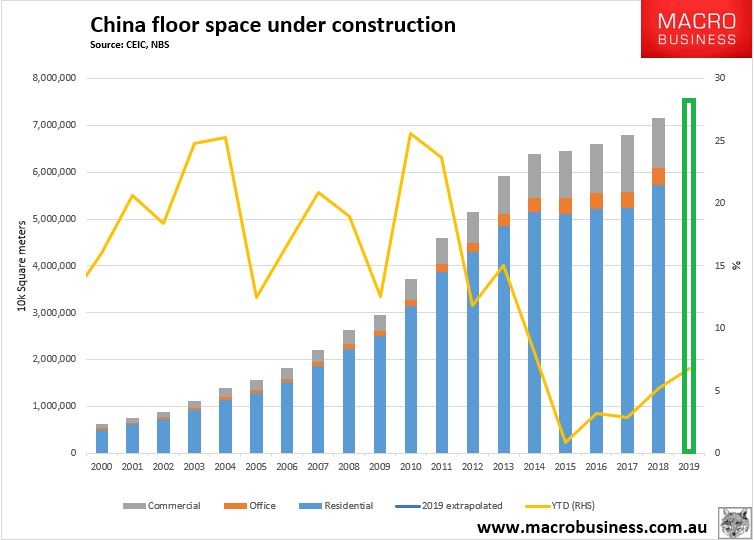

Total floor area under construction is now up an insane 6.8% from what was already mind-boggling levels (albeit over only the first two months and should pull back from here):

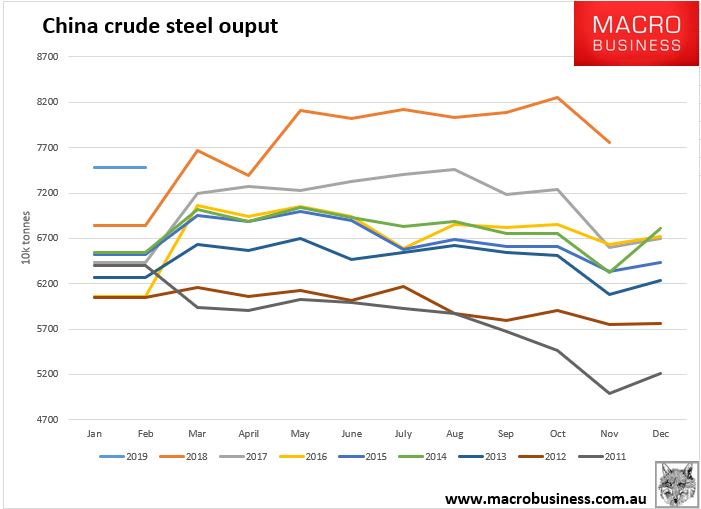

Crude steel output was simply massive at 77.6mt averaged for the two months. This is not even driven by last year’s shift of illegal production into official figures so must represent a giant stock build:

This is a construction powerhouse the likes of which the world has never seen before nor ever will again. That it can drive itself higher from such lofty altitudes leaves me quite out of breath. When it ends it will also leave the greatest overhang of unproductive debt in the history of the world and economic stagnation that will last one hundred years.

Will it peak here? Credit still suggests so:

But the stimulus, such it is, will likely support real estate construction at the margin.

There’s no immediate threat here for bulk commodities but some kind of easing off in construction demand is still the base case as the year progresses given the slowdown in real estate sales and deceleration in starts.