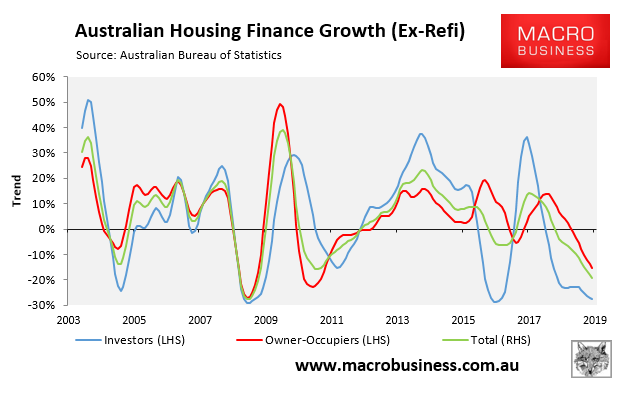

Yesterday’s Lending to households and businesses release from the ABS revealed that total mortgage lending (excluding refinancings) tanked by 19.2% in the year to January 2019 in trend terms, driven by an epic 27.7% crash in investor commitments, whereas owner-occupied commitments also fell by 15.4%:

As shown above, annual investor mortgage growth is a whisker above the GFC low, which was quickly followed by a sharp V-shaped recovery.

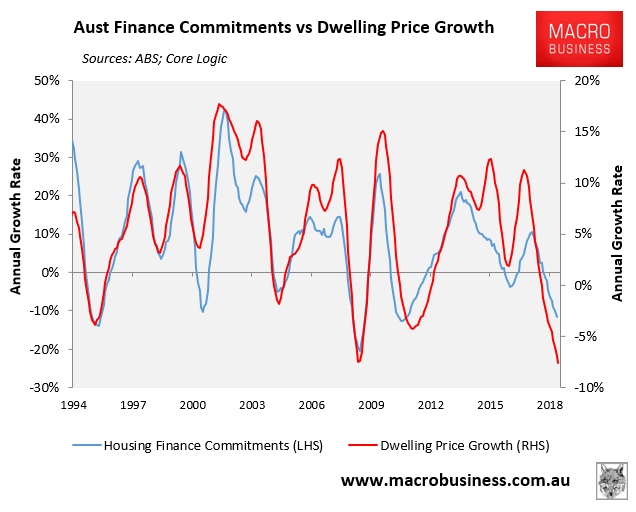

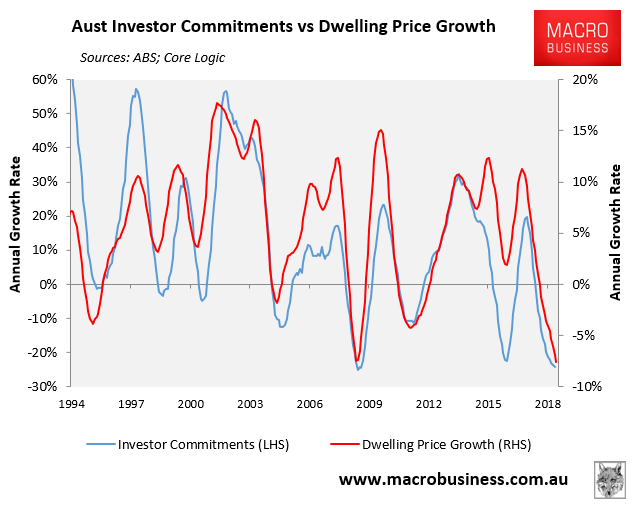

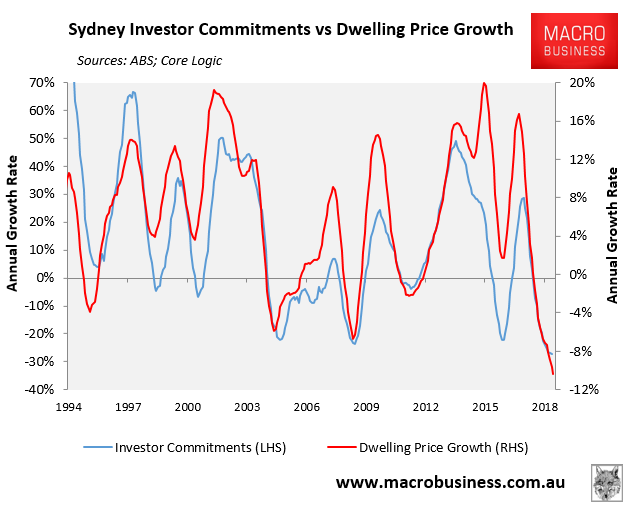

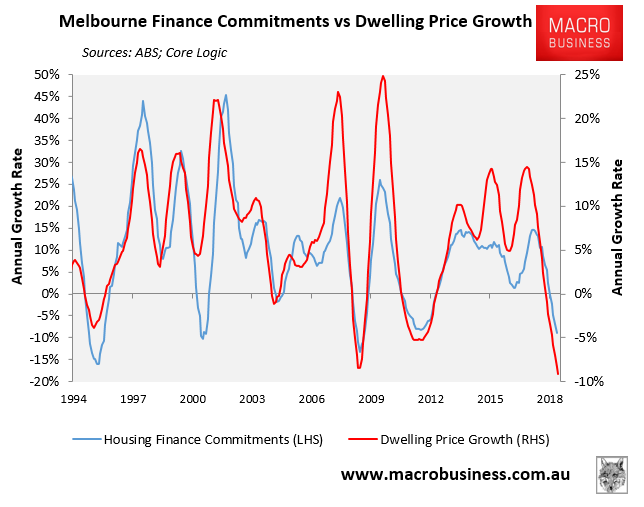

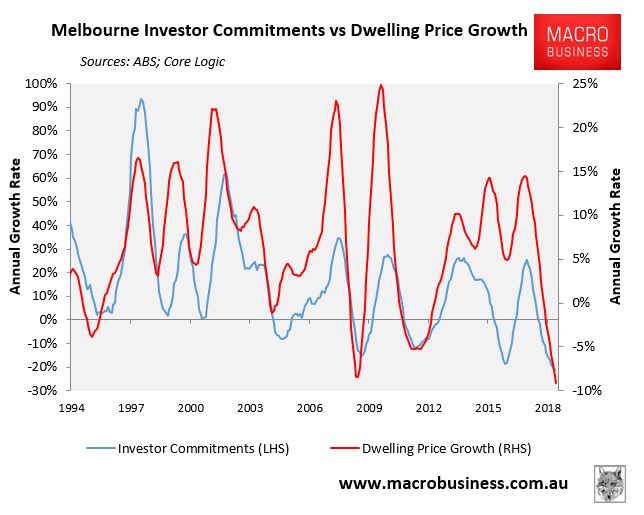

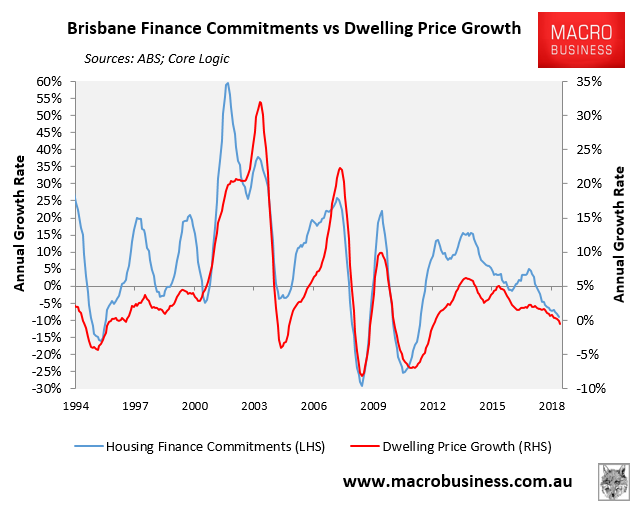

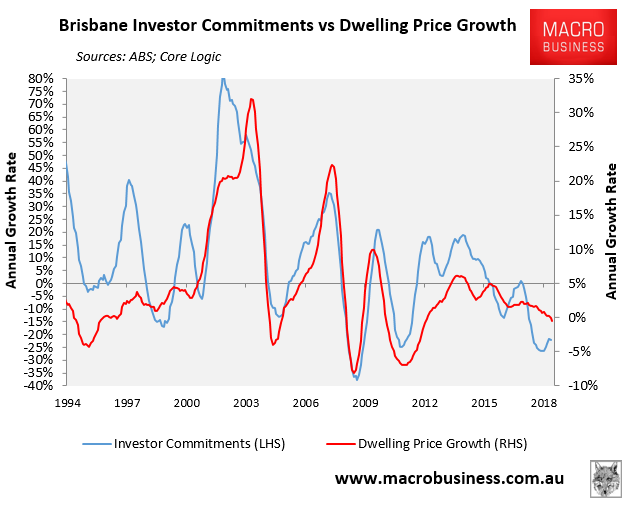

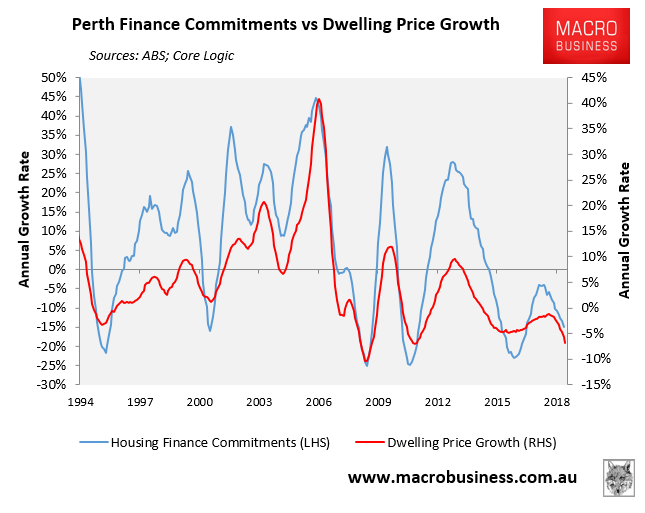

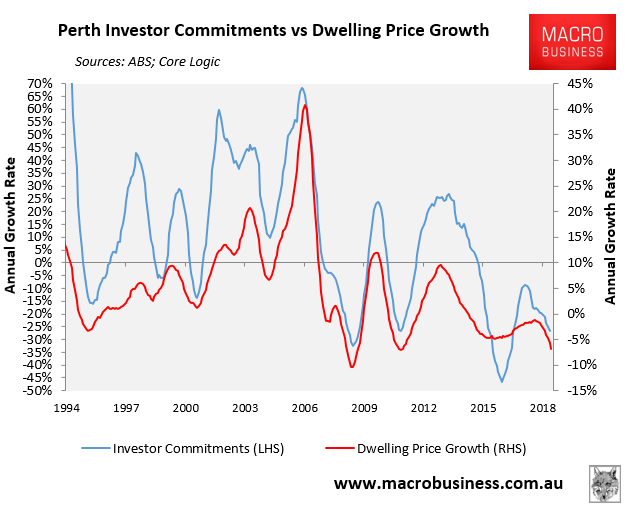

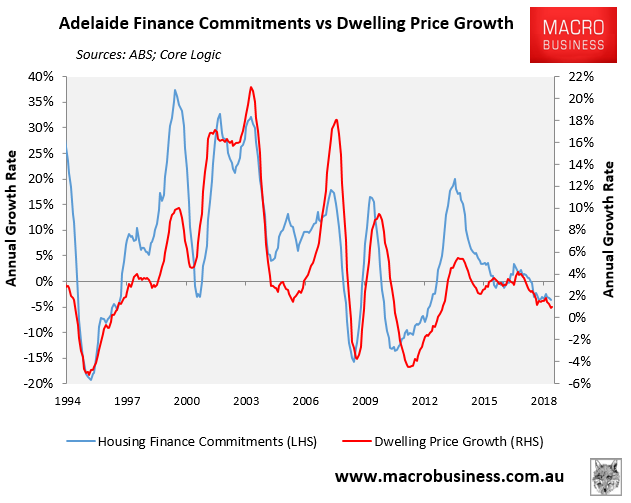

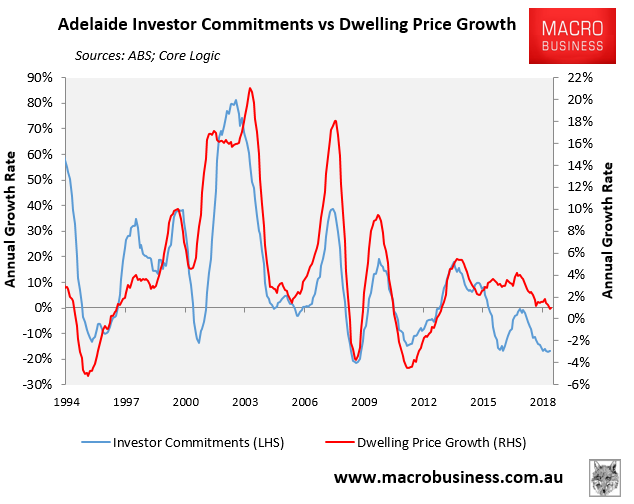

As regular readers of MB will know, we consider the flow of housing and investor finance commitments to be the premier indicators for dwelling value growth. This view is based on the incredibly strong historical correlation between finance and prices, as illustrated by the next charts:

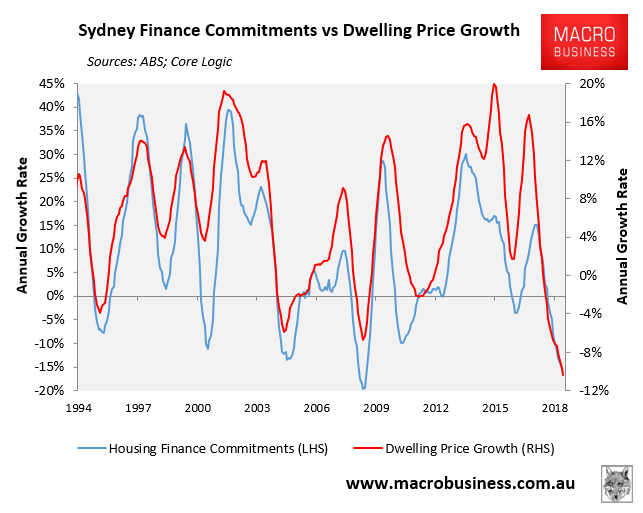

As you can see from the above charts, investor and housing finance growth as well as dwelling price growth has crashed across Sydney, Melbourne and Perth, and is also soft in Brisbane and Adelaide.

The decline is particularly dire in the investor mecca of Sydney, where investors remain the marginal price setter.

We already know that investors face stiff headwinds over the foreseeable future due to:

- Ongoing uncertainty following the Hayne Royal Commission, especially around the Household Expenditure Measure and legal action by ASIC against the banks, as well as various class actions by aggrieved borrowers;

- The possibility of further out-of-cycle mortgage rate rises; and

- Labor’s negative gearing and capital gains tax reforms in the likely event that it wins the next federal election.

Until housing finance turns and begins to rise, Australian housing will crash.