DXY broke out Friday night as EUR crashed and CNY fell:

Normally that combination would smash the Australian dollar but instead it rallied against all DMs:

And most EMs:

Playing catch-up for last week’s weakness I guess. CFTC positioning remains very short:

Gold was hit as DXY powers up:

But oil fell:

And metals beyond the nickel squeeze:

Big miners tracked the bear market rally in iron ore:

EM stocks held on:

But EM junk is breaking, a very bad sign for risk:

The Treasury curve was squashed again:

Bunds were on fire:

Aussie bonds tracked US:

Stocks were flat:

The rampaging DXY is now the central the question for markets. The rocket fuel is a crashing EUR, via Reuters:

Traders had varied explanations for the drop, including that month-end rebalancing of portfolios heightened an existing bias. The longer-term trend, which has seen the euro fall 0.90% in August, has been driven by an economic slowdown in Europe among other factors.

“We had a quick 50-odd point drop, which seems to be month-end related. Clearly the euro has been quite soft for some time. We touched below $1.10 earlier in August and we’ve struggled really to rebound from that point. The underlying softness that we’ve seen persist in the past month seems very much intact,” said Shaun Osborne, chief foreign exchange strategist at Scotia Capital.

The move also began shortly after President Donald Trump tweeted that the euro was dropping “like crazy” and lamented the state of the U.S. dollar, attributing its strength to Federal Reserve policy. A weaker dollar would send the euro higher, suggesting the tweet did not have a direct effect on the pair. The euro was last trading at $1.0976 against the dollar, down 0.71% on the day.

Poor euro zone economic data on Thursday reinforced views that the European Central Bank would cut its benchmark interest rate and announce a new round of quantitative easing at its September meeting. Christine Lagarde, the ECB’s next president, said the central bank still has room to cut rates if necessary, though divisions remain within the ECB.

As I have pointed out many times, a falling EUR is very bearish for AUD/USD. Indeed they very correlated:

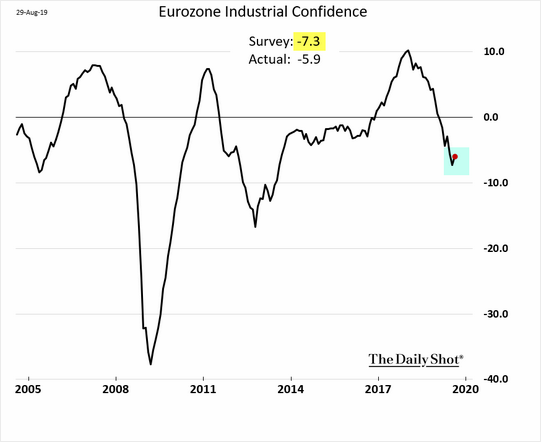

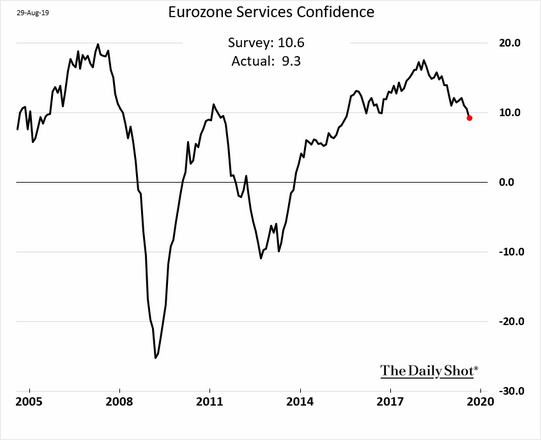

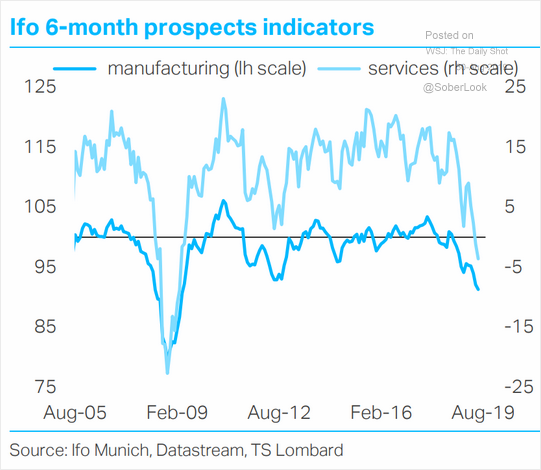

There is no doubt that EUR should be falling. The European economy is very weak and getting weaker. Led by German industry:

But drawing in services:

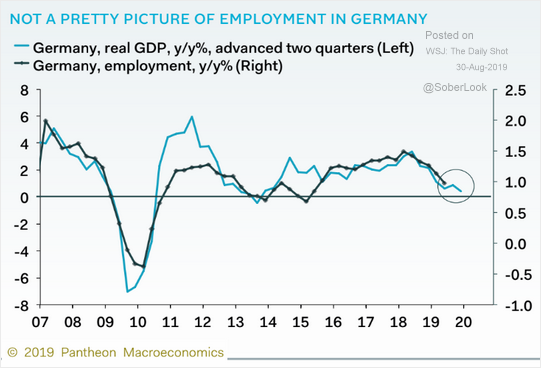

As jobs go:

The ECB is going have to fire off some kind of super-bazooka. And all of this before we see any fallout from a hard Brexit.

On the US side of the equation we have weakening growth but a much stronger labour market, much stronger inflation owing to tariffs, much lower exposure to falling global demand and a Federal Reserve that is more delayed by all of it, to the immense frustration of El Trumpo.

So, if we’re going to see DXY grind higher then obviously enough the AUD will grind lower. But there is another problem that could make it all a lot more volatile. A rising USD is always very negative for capital flows into EMs. They borrow a lot of money in USD-denominated loans so a rising DXY is effectively tightening monetary policy. This creates a feedback loop of capital flows out of EMs and into DXY, from the periphery to the centre.

Before long you begin to see credit stress at the margins of EM bond markets as junk spreads blow out. That is what is happening now. As DXY rises and EMs fall, then commodities give up the ghost. If oil is drawn in then the next domino to fall is the US junk bond market, followed by stocks:

These dynamics have determined every big stock market correction of the last three years and each time the AUD has gotten slaughtered as well.

If oil goes, we all go into year end.