And now for a terms of trade shock. Just what an income denuded, surplus-obsessed, stall speed economy does not need.

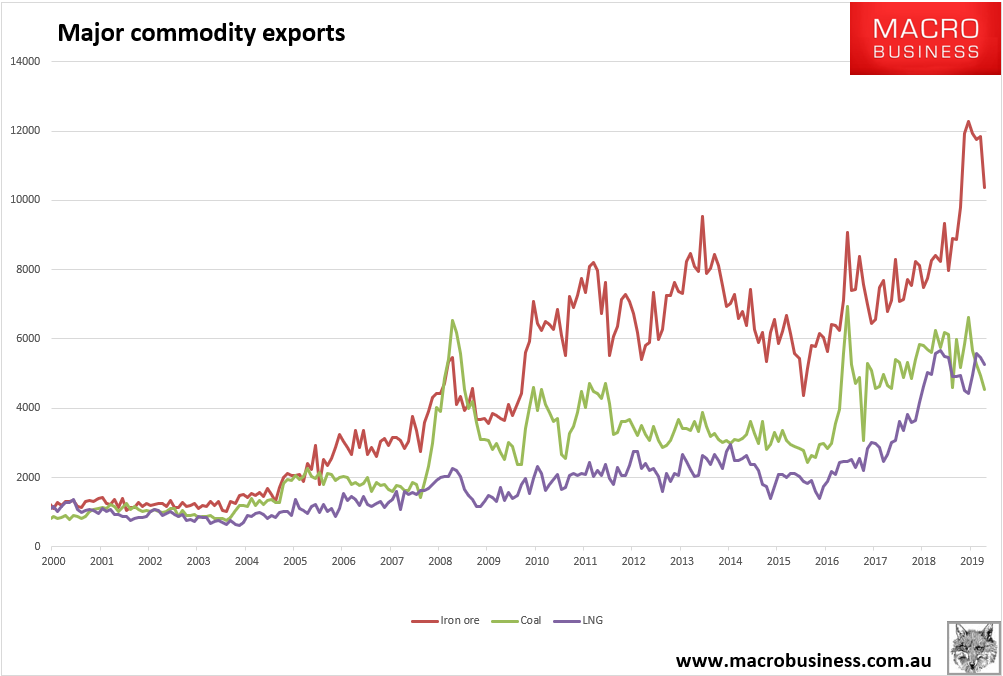

Yesterday’s trade balance numbers finally registered the inevitable as it fell from a surplus of $6.8bn to $4.5bn on the back of clubbed bulk commodoty prices:

This is just the beginning. My base case for next year is for $60 iron ore and thermal coal plus $120 for coking coal as Chinese realty slows. This will erase the trade surplus completely.

Nor do I expect it get better from there. The major driver is actually supply side adjustment in bulk commodity markets as earlier shocks dissipate. There is another 150mt of iron ore coming to market out to 2022. Scrap will keep rising too. Then the Simandou Pilbara killer looms in 2026.

We could easily see iron ore at $50 in 2021 and $40 in 2022.

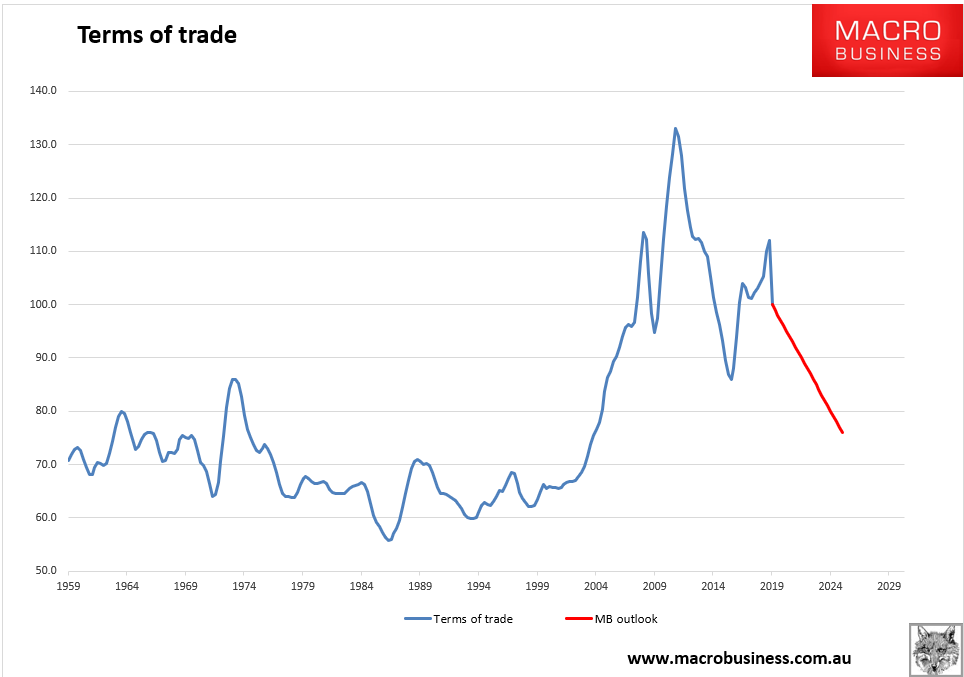

As a base case, I see the terms of trade falling away at good pace from here in a reversion to mean pattern as China goes ex-growth:

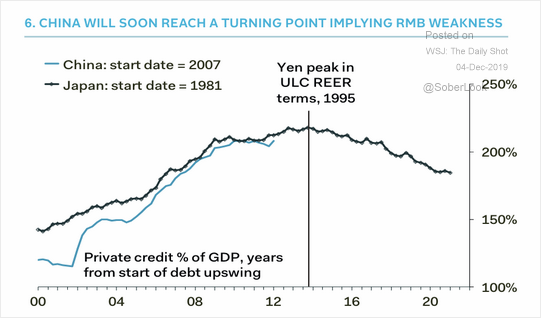

This is not a global shock scenario. It only assumes the stready slowing of China to 4% growth which will be, in reality, virtual zero. Check out the China versus Japan development analogy:

This will lay waste to Australian nominal GDP, destroy the Budget outlook and eviscerate wages. It is the basis for my long term forecast of the Australian dollar at 40 cents as the housing market gives up the ghost for good.

If you think that sounds extreme, consider that it took four years for the currency to fall 40% from the China boom peak. Is it really such a big call to see that repeated over the next six?

Australians have had a tough time of it in the past ten years but the next ten will be worse.

David Llewellyn-Smith is Chief Strategist at the MB fund and MB Super which is overweight international shares that will benefit from a falling Australian dollar.