Over many years, this site has shown that Australia’s compulsory superannuation system is an inefficient, costly monster that needs fundamental reform.

Our critique has often been centred around the inefficient and inequitable way that superannuation concessions are distributed, which perversely gives the greatest tax concessions to those that least need it least and are least likely to go on the Aged Pension – higher income earners.

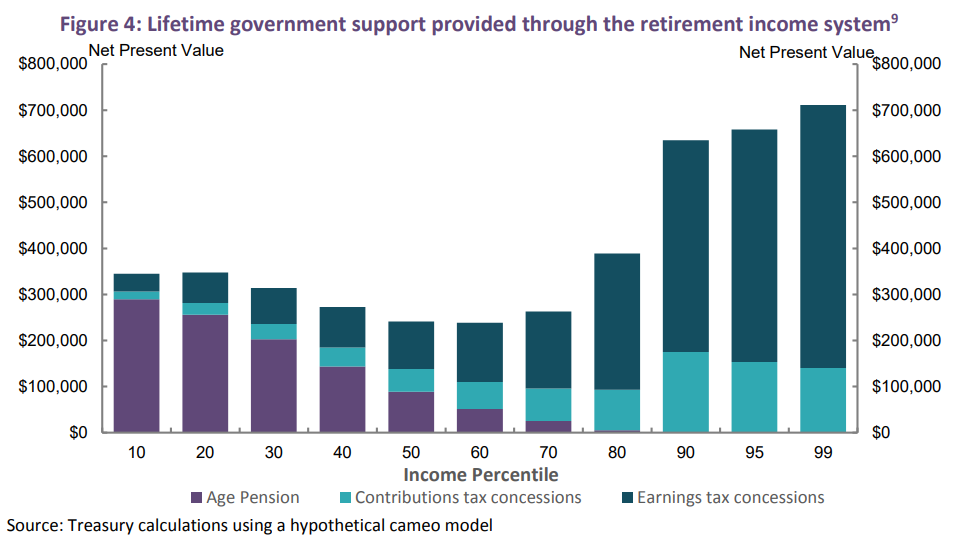

This is illustrated clearly by the below chart from the Australian Treasury, which is explained as follows by Richard Denniss – chief economist at The Australian Institute:

In Australia, taxpayers contribute 10 times as much money to the superannuation accounts of the people in the richest 1% than they contribute to the people in the poorest 10% of workers.

Put another way, the graph below also shows that, over the course of their lives, those Australians lucky enough to be in the top 1% of income earners will receive over $700,000 in taxpayer contributions to their personal superannuation account, while those in the bottom 10% will receive less than $50,000.

Advertisement

Thus, the $43 billion a year in tax concessions for superannuation are really a case of reverse ‘Robin Hood’, since they lavish massive taxpayer assistance to the wealthy, in turn worsening inequality.

Moreover, the poor targeting of tax concessions means that Australia’s superannuation system costs the federal budget more than its saves in Aged Pension costs. This was made abundantly clear by the Henry Tax Review:

“An increase in the superannuation guarantee would … have a net cost to government revenue even over the long term (that is, the loss of income tax revenue would not be replaced fully by an increase in superannuation tax collections or a reduction in Age Pension costs).”

…both the short and long term, superannuation tax breaks cost the budget more than they save in pension payments:

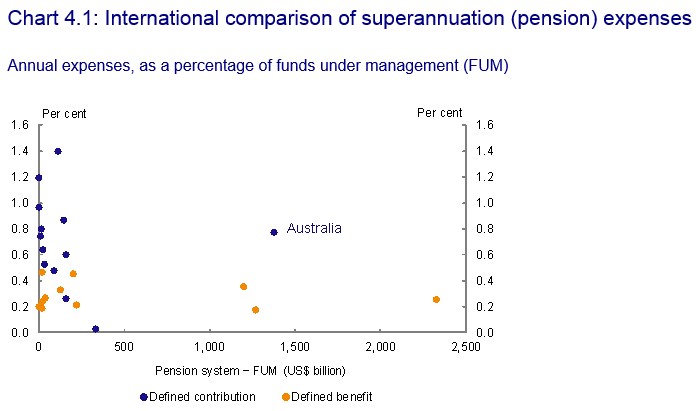

The inefficiency and waste of Australia’s superannuation system is also gleaned from the exorbitant fees charged. These are well above the OECD average despite the enormous funds under management.

Advertisement

The below chart from the Murray Financial System Inquiry tells the tale:

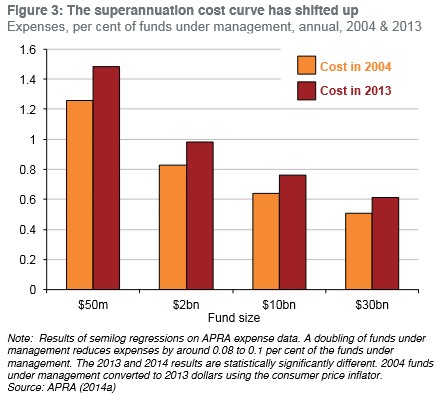

The Grattan Institute has also shown that Australia’s superannuation system has become less efficient as it has ballooned in size:

Advertisement

A larger system of larger funds should have incurred lower costs and charge lower fees, because big funds have lower costs…

Australian funds charge fees that are three times the median OECD rate, on average… Many countries have superannuation pools much smaller than Australia’s, yet their funds charge customers much less.

Indeed, Australians spend twice as much each year managing their superannuation than they do on electricity. But because these fees are hidden from view, few realise it.

Accordingly, Australia’s compulsory superannuation system has spawned a giant industry of rent-seekers feeding off these fees, which now rivals Australia’s Defence Force. And this represents a “massive drain on economic activity”, according to Dr Cameron Murray:

Advertisement

Since 2012 the number of jobs in the super sector has climbed steadily from 48,000 to 55,200 in 2018, while the number of permanent defence force personnel has flatlined around 58,000, according to analysis by Dr Cameron Murray, an economist at the University of Sydney.

“Super fees in 2018 were $34bn, compared to $36bn for the total defence force, but that figure includes a 19,000 strong defence bureaucracy and army reservists,” he said, adding it was “madness to waste vast economic resources on an unnecessary accounting exercise”…

Dr Murray said the super system had reduced Australia’s productivity “by dragging an enormous workforce away from other productive activities, making us less able to support retirees”.

Only 33,000 staff work at the Department of Human Services, which administers the age pension along with all national welfare programs, including Medicare, Dr Murray said.

“This comprehensive welfare system costs just $6bn per year to manage — one-sixth the management cost of superannuation,” he said.

Dr Murray also questioned the effectiveness of superannuation tax breaks of around $40bn a year in forgone revenue. “This is as much as the total age pension system, implying that if we unwound the superannuation system, the age pension could be doubled, or the qualifying age reduced to double the recipients, at no budgetary cost,” he said.

Given the myriad of problems afflicting Australia’s superannuation system, it is unambigously bad policy to raise the superannuation guarantee from 9.5% to 12%. All this would do is heighten the above inefficiencies, rob workers of disposable income, worsen the long-term sustainability of the federal budget, and worsen inequality.

The only winners would be Australia’s already bloated superannuation industry, which would ‘clip the ticket’ on more funds under management and earn even fatter fees.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.