Actuarial firm, Rice Warner, is the latest to acknowledge that Australia’s superannuation system costs the federal budget more than it saves in aged pension costs, and estimates that raising the superannuation guarantee (SG) from 9.5% to 12% would cost the economy 0.22% of GDP “through this century”:

The Australian government gave up A$41bn (€25bn) in tax revenue last year to support its universal superannuation scheme…

The government’s annual revenue loss through tax concessions to super will rise steadily as the pool grows in coming years. The impact of forgone revenue will accelerate as the next round of legislated increase in the super levy – or superannuation guarantee – kicks in from July this year.

It aims to gradually lift the employer contribution by 0.5% each year from the current 9.5% to 12% by 2025…

Actuarial firm Rice Warner said that lifting compulsory super contributions to 12% would not have much impact on the age pension for many years, and would save the budget only about 0.1% in lower age pension spending in the second half of this century.

In contrast, extra super tax breaks from higher compulsory super would cost an average of 0.22% of GDP “through this century”…

Rice Warner’s estimates are supported by The Grattan Institute, which last year estimated that lifting the SG would cost the federal budget an additional $2 billion to $2.5 billion a year:

Lifting compulsory super from 9.5% to 12% as is legislated over the five years from 2021 to 2025 will deprive the Treasury of an extra A$2 billion to A$2.5 billion per year.

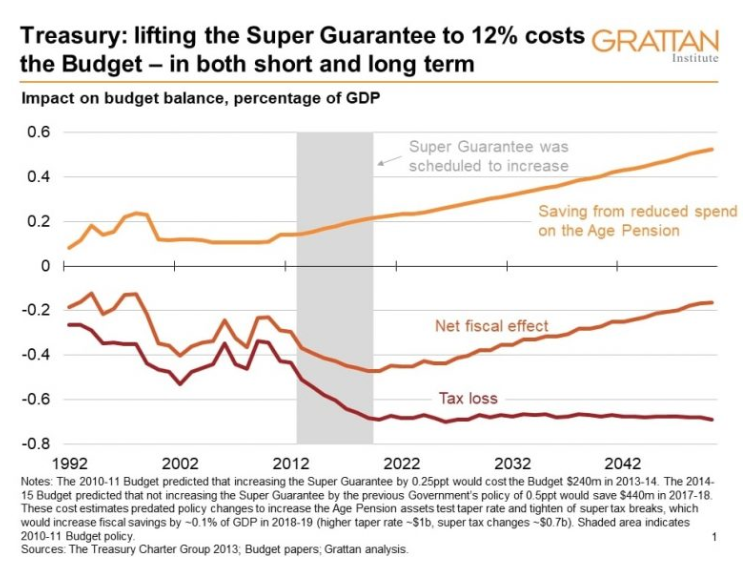

In 2013 the Treasury estimated that the extra revenue foregone from tax breaks after contributions were lifted from 9% to 12% would exceed the budget savings on the pension by 0.4% of GDP a year.

Eventually – by 2050 – the net budgetary cost of super tax breaks would be “only” 0.2% of GDP a year. The extra cost of the tax breaks would continue to exceed the savings on the pension until about 2060, with the resulting debt not paid off in savings on the pension for decades.

Advertisement

Remember, too, that the Henry Tax Review (here and here) explicitly warned that lifting the SG to 12% would harm the federal budget and recommended against doing so:

An increase in the superannuation guarantee would … have a net cost to government revenue even over the long term (that is, the loss of income tax revenue would not be replaced fully by an increase in superannuation tax collections or a reduction in Age Pension costs)…

The retirement income report recommended that the superannuation guarantee rate remain at 9 per cent. In coming to this recommendation the Review took into the account the effect that the superannuation guarantee has on the pre-retirement income of low-income earners.

No wonder the superannuation industry is so strongly in favour of lifting the SG, since it represents a transfer from taxpayers into their coffers.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.