Over the past month, we have witnessed various groups call for explicit government intervention to bridge the discrepancy between male and female superannuation savings.

It started when the ACTU demanded the superannuation guarantee be lifted to 15% for women.

Shortly afterwards, KPMG requested the government make direct contributions into women’s superannuation accounts, which was echoed by the Victorian Government.

The National Foundation for Australian Women (NFAW) has used its submission to the federal government’s Retirement Income Review to argue against progressively increasing the superannuation guarantee from the current 9.5% to 12%. Professor Helen Hodgson from NFAW says increasing the superannuation guarantee would reduce the take-home pay of low-income earners, and women in particular:

…the National Foundation for Women, an independent Canberra-based research body, has argued an increase in the super guarantee rate is likely to hurt low income earners the most, opposing the message funded by the $2.9 trillion super sector.

“NFAW is concerned that increases in the rate of the SG may affect the take-home wages of low income earners, particularly women, who are more likely to be part-time and casual employees,” said Professor Helen Hodgson, the chair of the NFAW social policy committee…

“Even if the burden is not passed to the employee in full, in the current environment of low wage rises any reduction in take-home pay will reduce the standard of living for low income households,” Professor Hodgson said.

“The legislated increase in superannuation guarantee should not proceed if it results in lower levels of take-home income for low income earners,” she said…

NFAW echoes the arguments made by ACOSS in its submission to the Retirement Incomes Review:

ACOSS chief executive Cassandra Goldie said the $3 trillion system of “forced saving” under superannuation “paid too little heed to the needs of people struggling on low incomes during working life” and must better consider people on low wages when they are younger.

“The flawed system of tax concessions for super contributions should be fixed before compulsory contributions are lifted to 12 per cent”…

“For people on lower incomes, who often struggle to meet the basics of life now, the benefits are not so clear.

As I have noted previously, women generally retire with lower superannuation balances because they earn less than men over their working lives due to working in lower paid professions, working part-time, or taking time off from working to raise children.

Therefore, simply lifting the superannuation guarantee to 12% would widen the gender retirement gap even further, in addition to depriving low income earners of disposable income throughout their working lives.

In fact, this was the precise conclusion from the Australian Treasury last year:

Though compulsory SG contributions are paid by employees, wage setting generally takes into account all labour costs. It is widely accepted that employees bear the cost of higher SG in the form of lower take-home pay. This means there will be a trade-off between people’s income during their working lives and their income during their retirement…

The main drivers of women having lower [superannuation] balances than men are women’s lower incomes and longer career breaks. While the increase in rate of SG would increase retirement balances for women, it would likely lead to an even larger increase in male retirement balances due to their higher lifetime earnings…

The first best solution for improving superannuation equity is to make concessions progressive by targeting concessions at those who need it most – i.e. lower and middle income earners. This way, lower income earners would accumulate bigger retirement savings without forgoing take-home pay, irrespective of gender.

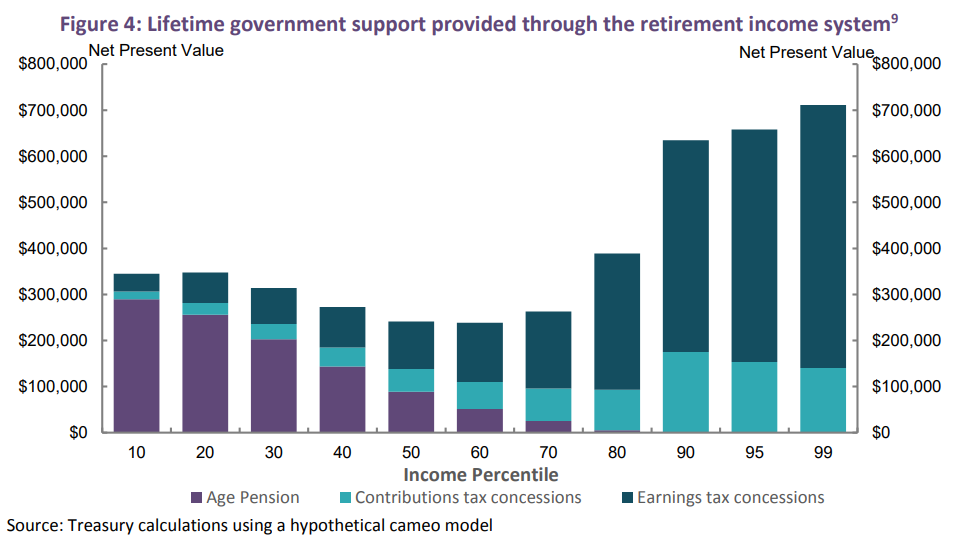

The federal budget would also benefit, given superannuation is currently being used as a tax avoidance scheme by the wealthy (mostly men) who would never have taken the Aged Pension anyway. The below chart from the Australian Treasury illustrates this point clearly:

As you can see, the top 1% of income earners will receive more than $700,000 in taxpayer contributions to their personal superannuation accounts over their working lives, dwarfing the $50,000 received by the bottom 10% of income earners.

Instead of blindly lifting the superannuation guarantee and lowering workers’ take home pay, blowing a bigger hole in the federal budget and worsening inequality, policy makers should focus on ensuring that existing superannuation settings are operating equitably and efficiently.

Abolishing the scheduled increase in the superannuation guarantee and making concessions progressive should be the first step.