DXY was soft Friday night:

The Australian dollar was strong across the board:

Gold was stable:

Oil is still buggered:

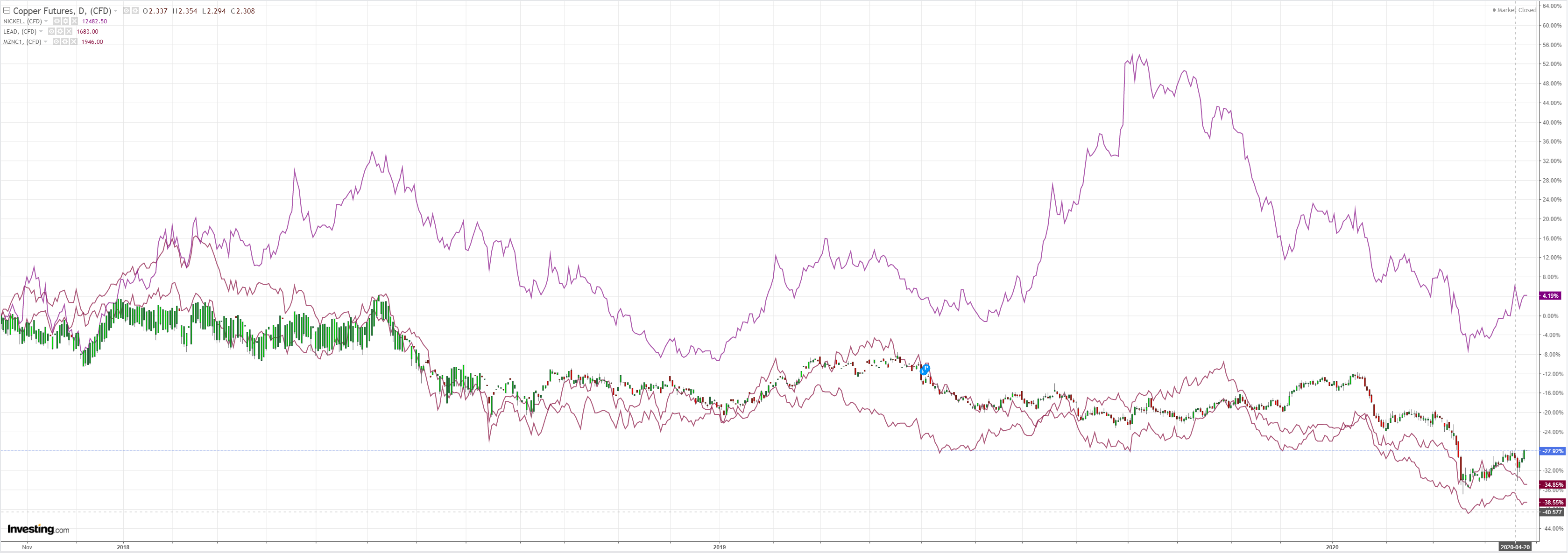

Dirt did better:

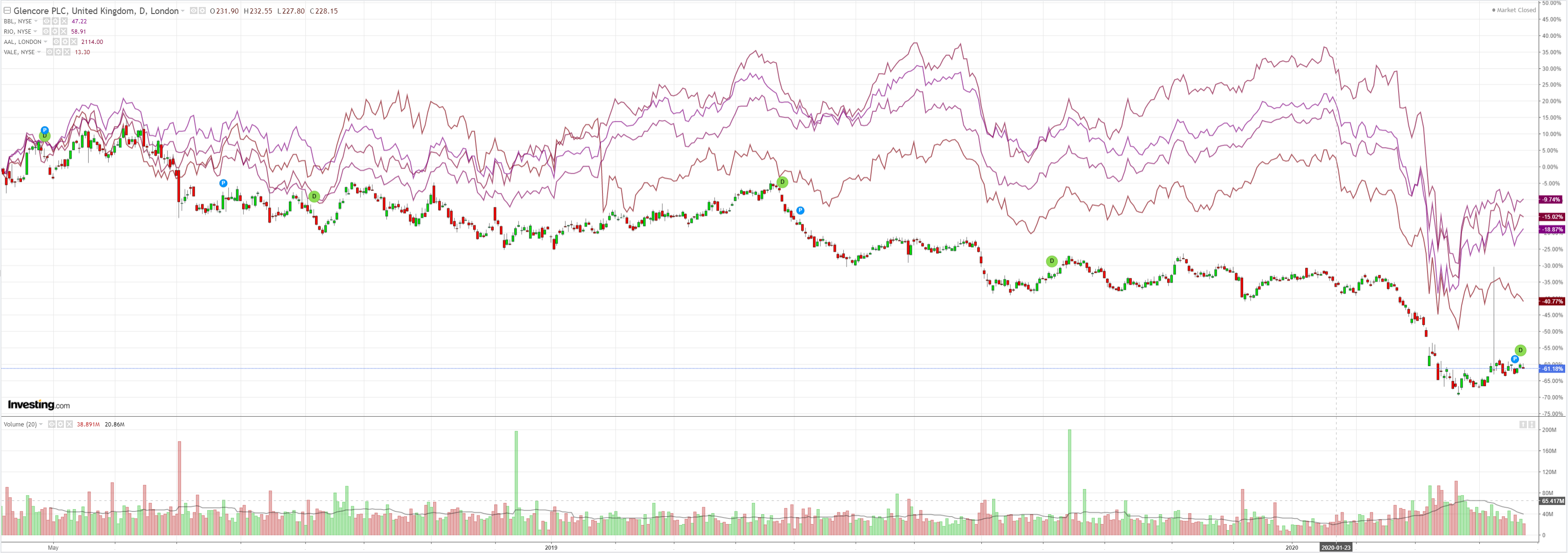

Some miners as well:

Not so EM stocks:

Junk skidded:

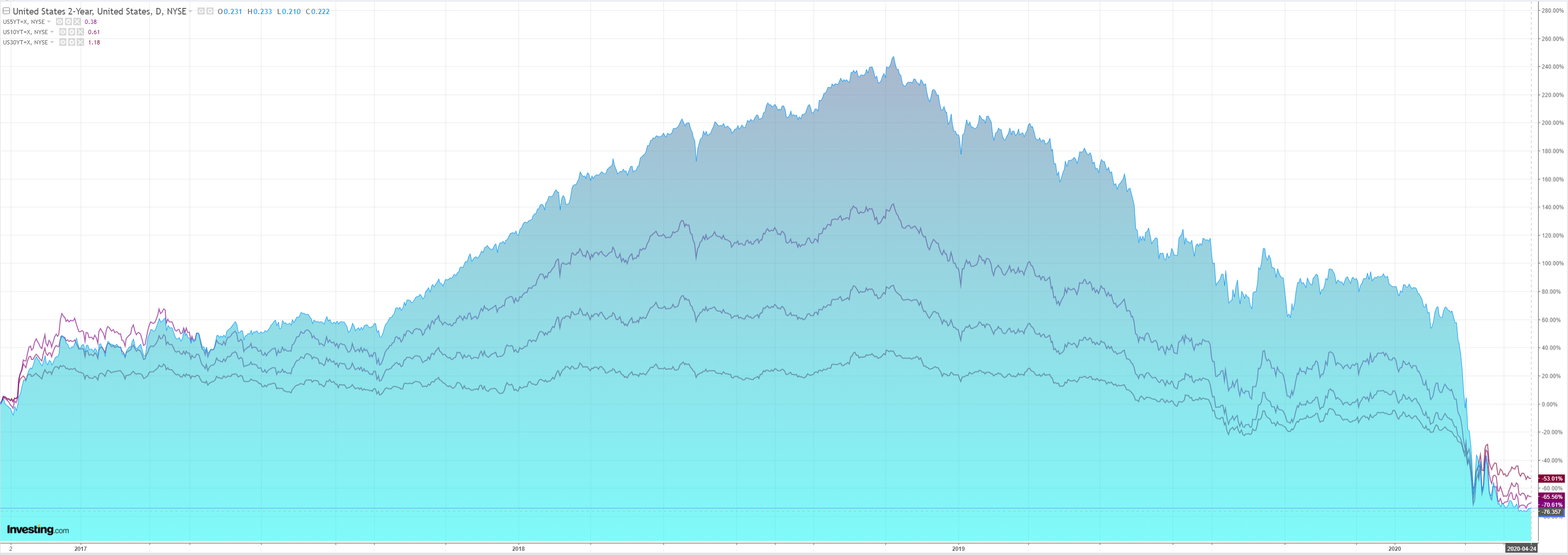

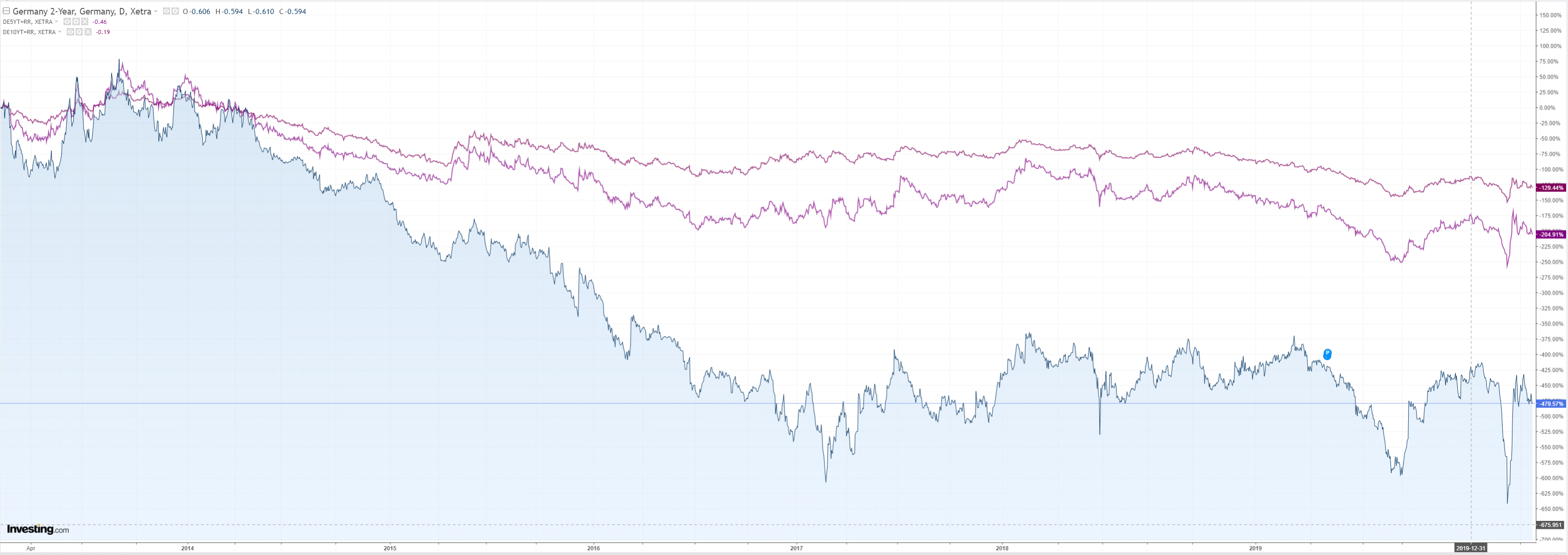

Bonds were bid:

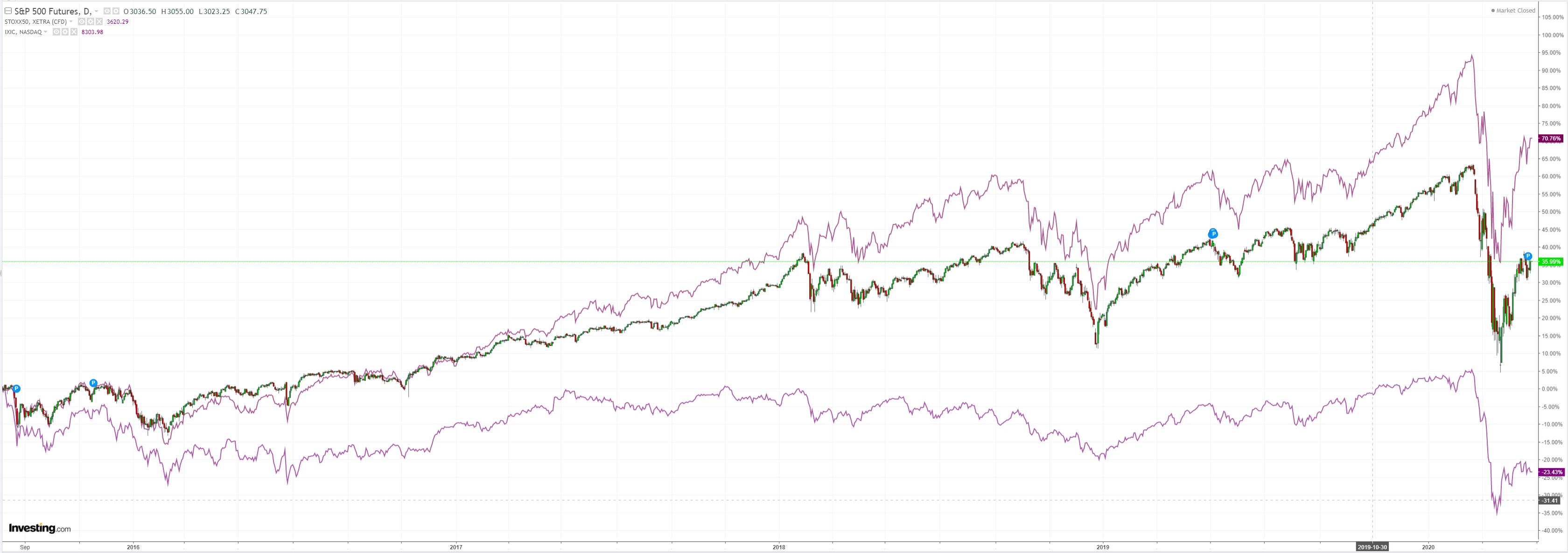

Stocks spiked anew:

Texture from Westpac:

Event Wrap

COVID-19 update: The global case count continues to roll over, with latest data from John Hopkins University indicating 87k new confirmed cases worldwide on 25 April, vs 101k the previous day (the new peak).

US March durable goods fell 14.4%m/m (ave. est. -12.0%m/m). Ex-transport orders fell 0.2%m/m, less than estimated (ave. -6.5%m/m). University of Michigan consumer sentiment held at 71.8, from its preliminary release of 71.0 (and estimates of a fall to 68.0), still showing the largest monthly drop on record. Inflation expectations were unchanged (1yr 2.1%, 5-10yr 2.5%).

German April IFO current assessment fell to 79.5, in line with estimates of 80.5, but the expectations component did not rebound as seen in the ZEW surveys and fell to 69.4 (est.-75.0).

UK March ex-auto fuel retail sales fell 3.7% (est. -4.0%m/m) and fell 5.1%m/m including fuel (est. -5.0%m/m) as the initial stage of lockdown caused the largest monthly fall on record with clothing dropping -35%m/m.

Event Outlook

Japan: The BoJ will hold its monetary policy meeting. However, with limited space for conventional easing, the focus will be on unconventional policy and the asset purchase program.

China: March industrial profits are due. This will provide the first clear read after CLNY, but the virus will stifle earnings.

US: A soft print is expected for the April update of the Dallas Fed survey Index (market f/c -75.0); the index is already at a record low.

More calamitous data everywhere. But the Australian dollar is still flying on the reopening hopes. To me it remains obvious that reopenings across the northern hemisphere are either not coming or if they do, will directly result in the second wave of the virus. It remains rampant just about everywhere.

Clearly it will take time to price the faltering recovery to come.