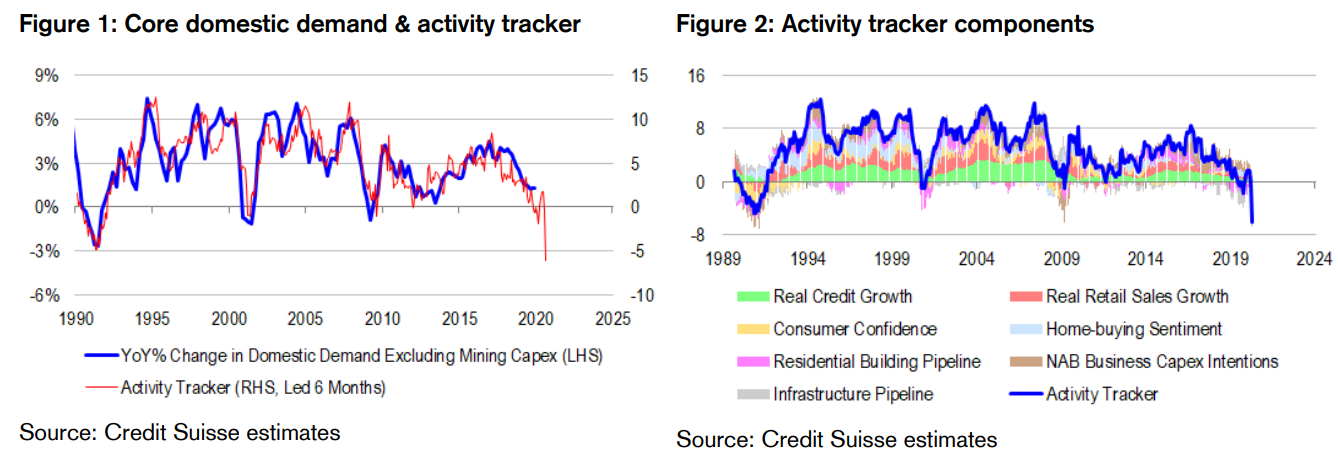

Core domestic demand to fall 3.5%. Our proprietary domestic demand tracker, based on a wide array of timely and leading indicators, is currently pointing to sharp contraction in non-mining domestic demand of around 3.5% annualized in the coming months. Near-term, inventory build and bounce in exports could cushion the blow to GDP. But nonetheless, the economy is on track for its worst performance since the early 1990s recession.

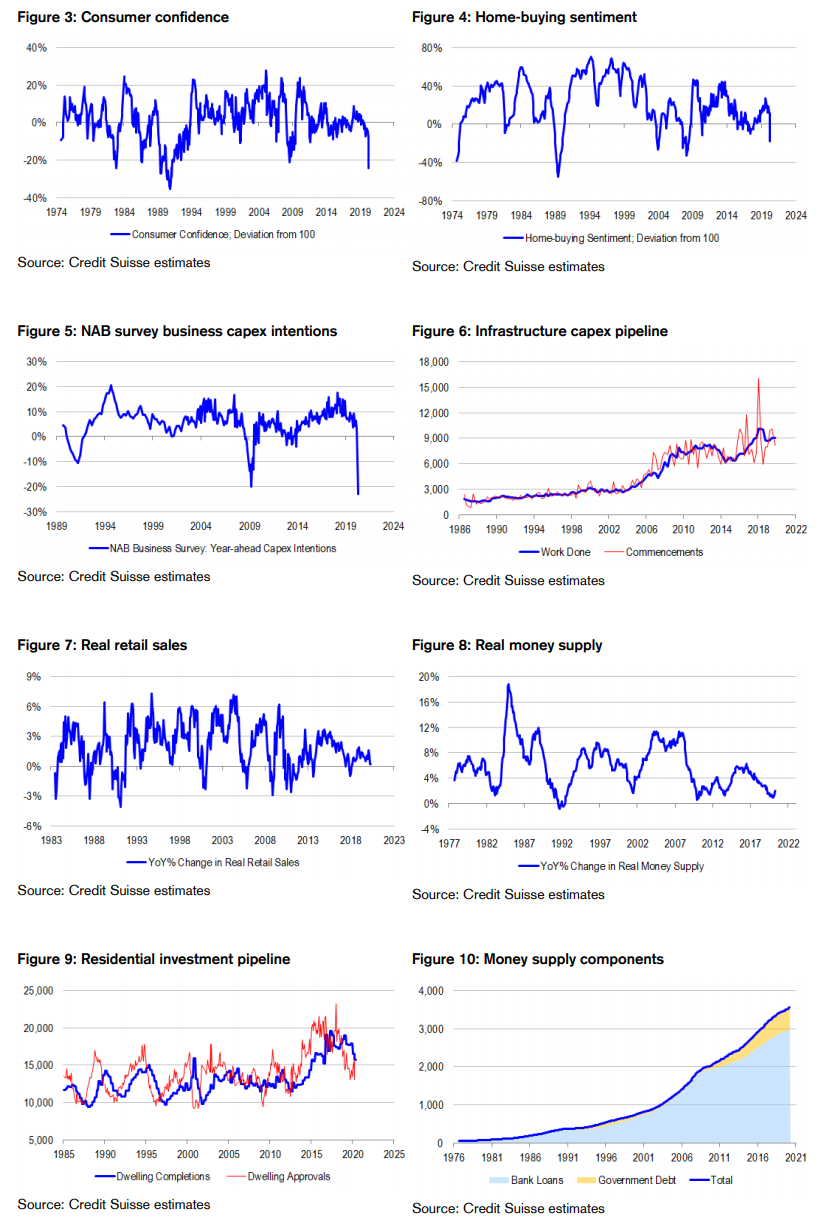

Confidence components of our activity tracker look especially weak. In March and early April, business, consumer and housing sentiment have all plunged, driving our activity tracker into deep contraction territory. COVID-19 shutdowns have weighed heavily on firms’ desire to invest and hire. Consumers have been burdened by job insecurity against the to finance, and public auction bans.

Aggregate hours worked to fall 3.8%. Our proprietary activity tracker is a useful complement to conventional leading indicators of job creation such as the NAB business survey employment index, and growth in ANZ job advertisements. The weighted average of the three indicators is currently pointing to shrinkage in aggregate hours worked of almost 4% annualized in the coming months. Notably, all components of our proprietary labour market leading indicator are pointing sharply lower. All of this said, perhaps in the short-term, increases in the official unemployment rate will be mitigated by the government’s “Job Keeper” program, and associated reductions in average work weeks. Also, it is possible that participation rates will fall – that unemployed secondary income earners will drop out of the workforce to limit the rise in the unemployment rate.

Will the unemployment rate hit 10%? Interestingly, the Treasury is forecasting an increase in the unemployment rate to 10% by 2Q 2020. To achieve this outcome, we would need to see hours worked fall by more than our leading indicators currently suggest and assume that all of the adjustment occurs in jobs rather than average work weeks. We would also need to assume that policy measures and falling participation fail to be mitigating factors. Suffice to say, this is an incredibly bearish scenario indeed. To be sure, we can never say never to undershooting risk, especially given that employment has been remarkably resilient to slowing growth in recent times. But we suspect that the real story is that officials are bringing back memories of the early 1990s recession in their wargaming, with the intentions of managing expectations and building the support case for emergency stimulus measures.

Productivity and potental growth rates are slowing. The really bad news in our view is that potential growth is slowing sharply. Applying a mathematical filter to the data, updated for information in our activity tracker, trend growth in domestic demand has slowed towards zero and may have even turned negative. To be sure, filters can often be wrong in real time, because they lack perfect foresight. But we are not totally in the dark here. Interestingly, the inflation-indexed bond yield is a powerful leading indicator of trend growth in the interest rate-targeting era, with a lead time of roughly 5 years. It provides us with some of the missing foresight we need. And it currently points to negligible potential, or supply side growth. Bond market investors are saying that this recession could easily destroy productive capacity by bankrupting businesses. Moreover, if and when demand stabilizes or recovers, we do not get these bankrupted businesses back. We could easily find ourselves in a situation where too much money is chasing too few goods and services, bringing back inflation ahead of time.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.