DXY was up overnight:

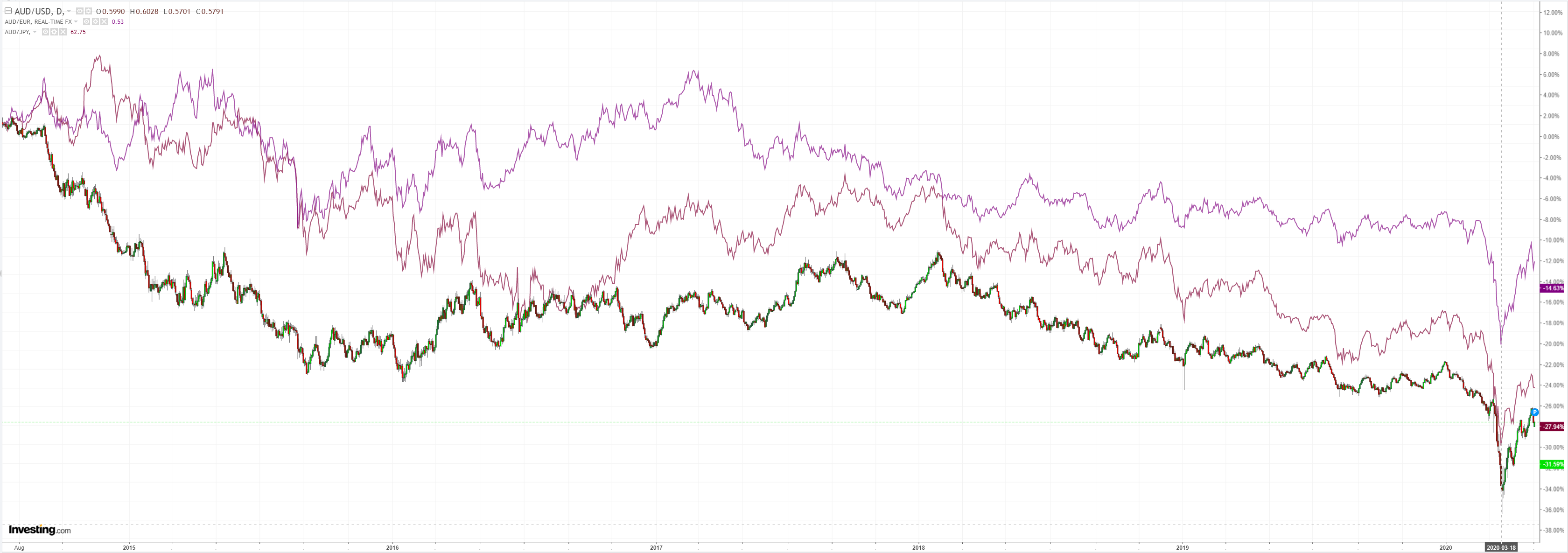

The Australian dollar stabilised:

Gold firmed:

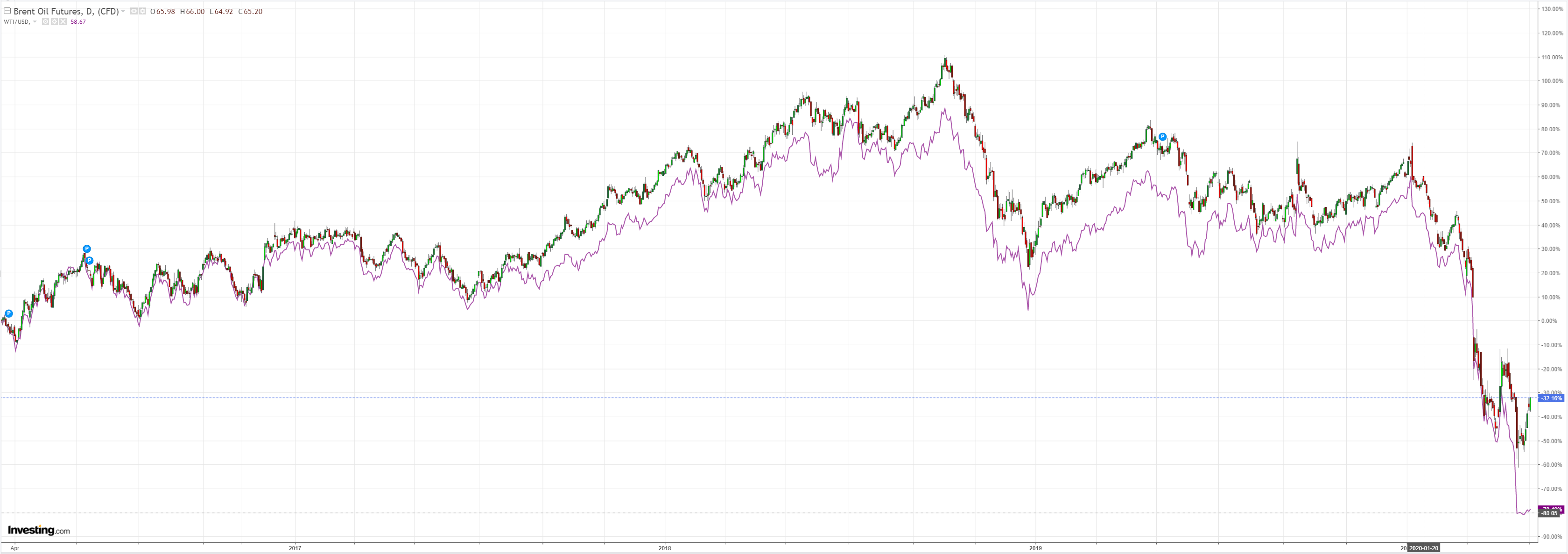

Oil looks like it has bottomed, notwithstanding further volatility:

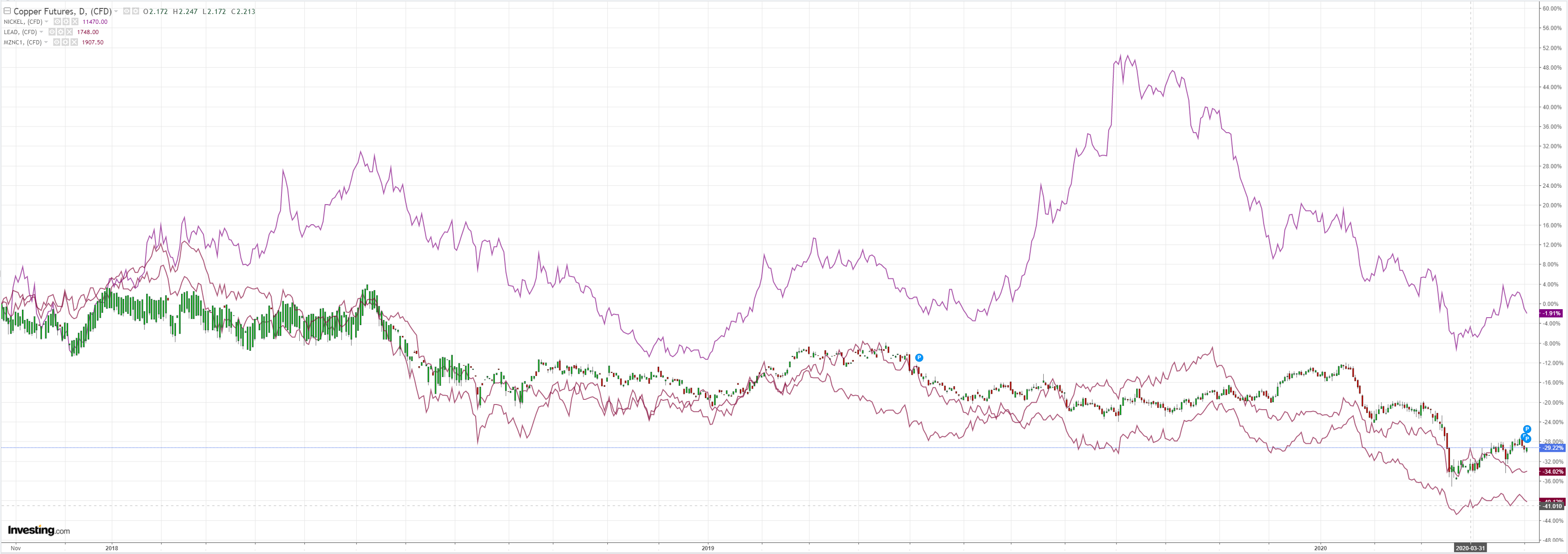

Dirt was weak:

Miners were soft:

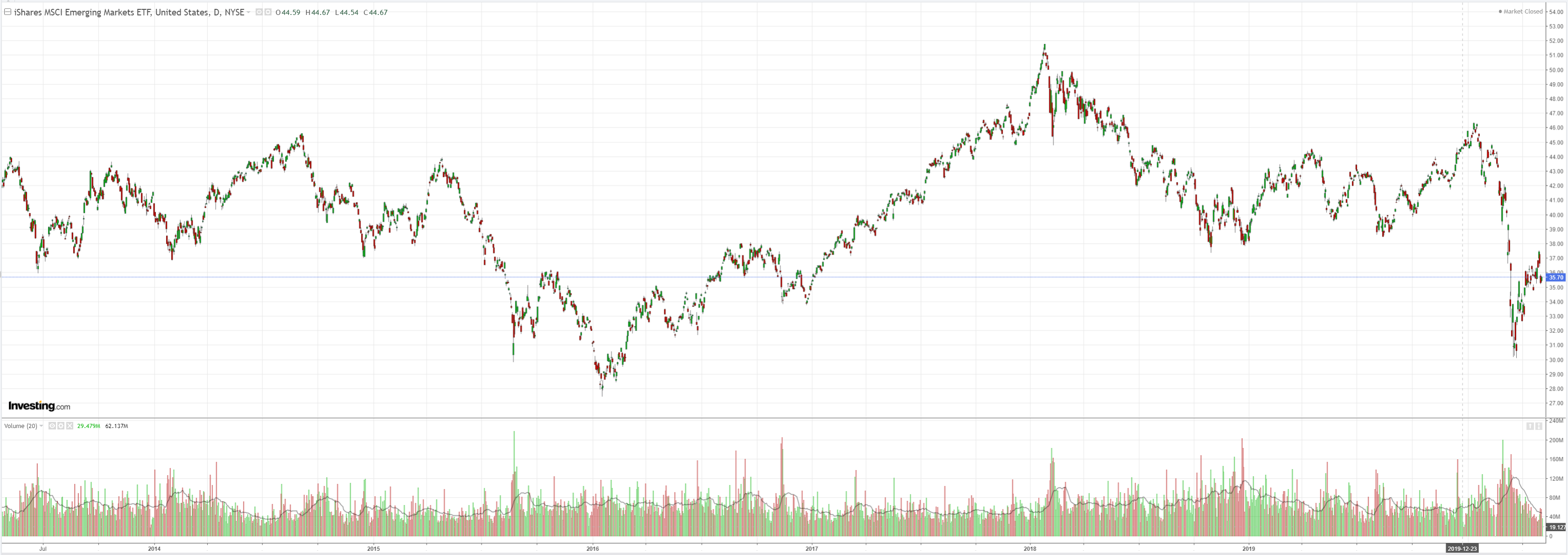

EM stocks too:

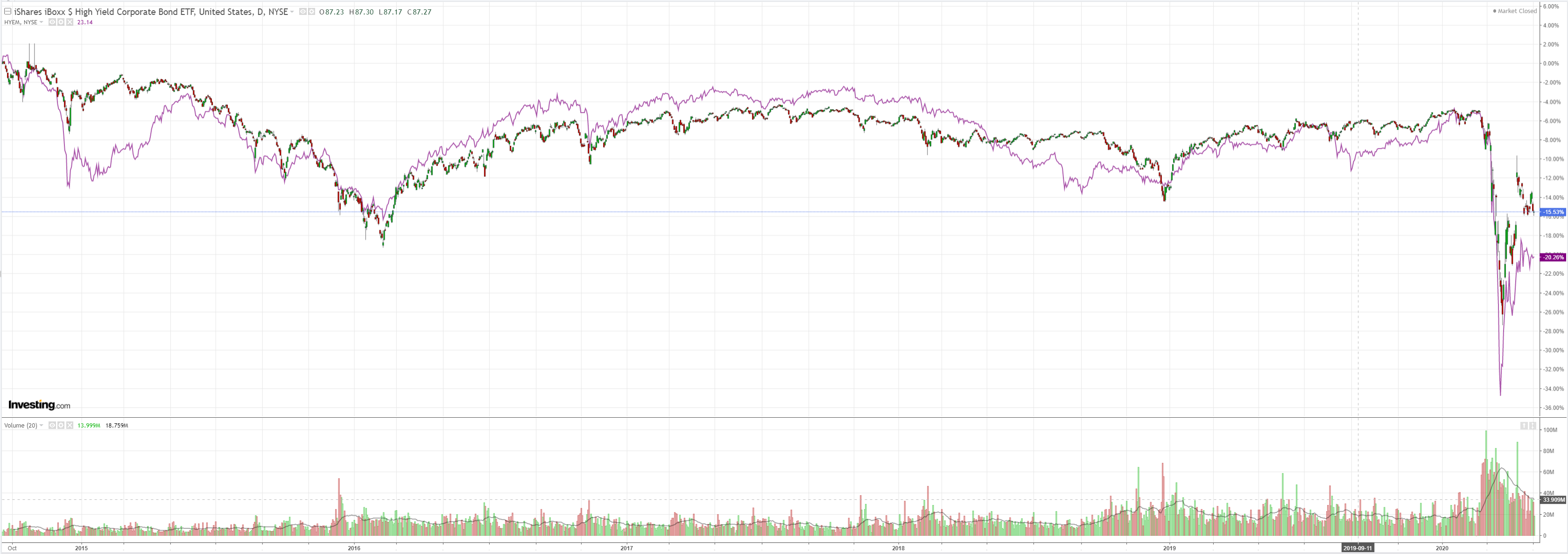

And junk:

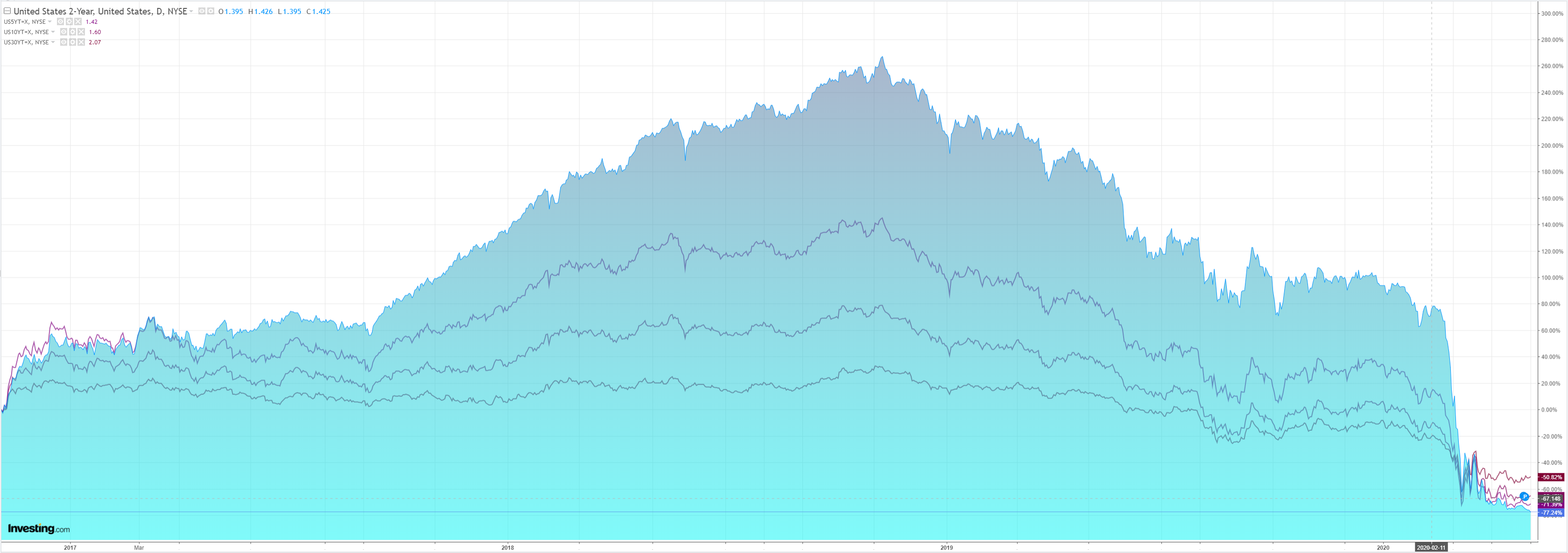

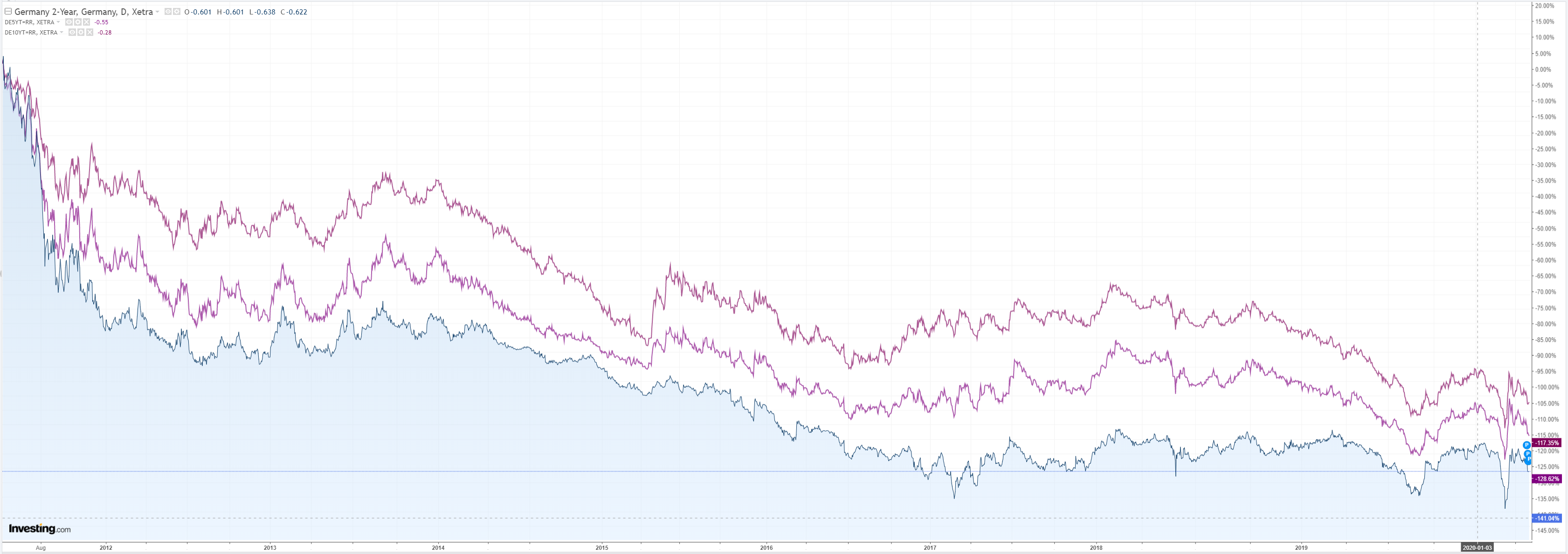

Bonds were bid:

Stocks fell but it’s still “buy the dip”:

Westpac has the wrap:

Event Wrap

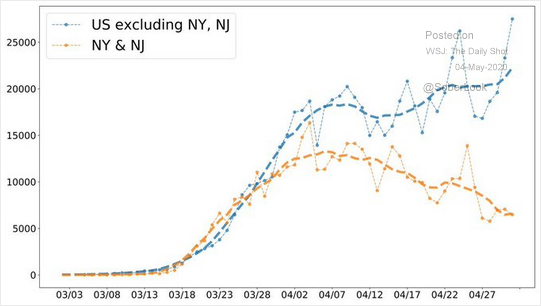

COVID-19 update: The global case count, according to the latest data from John Hopkins University, indicates 74k new confirmed cases worldwide on 3 May, vs 84k the previous day and vs 102k at the peak on 24 April. Whereas in March daily cases accelerated, in April they have trended sideways.

Eurozone final April PMI edged lower to 33.4 (vs flash 33.6), and although the scale of the lockdown disruption remains severe and signals a sharp contraction, there were tentative signs of lifting optimism.

US March factory orders declined 10.3%m/m, close to the -9.7% expected, further underscoring the disruption caused by COVID lockdowns. The revision to durable goods orders was also to the downside, if only mild (ex-transport slipped to -0.4%m/m from initial -0.2%m/m.

Event Outlook

Australia: The April AiG construction PMI will be the first release of the day. In March, new orders were hit particularly hard, and posted a fall of 10.3pts. The ABS’s April 18 “Weekly Payroll Jobs and Wages” survey will follow, and is set to reveal a sharp fall in employment. The major release of the day will be the RBA policy rate announcement. Whilst the cash rate is expected to hold at the effective lower bound of 0.25%, the Board’s assessment of its yield curve control will be of great interest to the market.

New Zealand: March building permits are due, and Westpac is looking for a 25% contraction. This is largely a product of the 5 fewer working days in March that resulted from the lockdown. However, there will be fewer new projects going through the consenting process over the coming months, leading to a slowdown in building through 2021. Following this, April ANZ commodity prices will be published, and will reflect the sharp falls in meat and dairy prices.

US: The March trade balance is expected to show that the deficit widened to $44.2bn. At -$39.9bn, the February release was the narrowest in 3 years. In addition, the market expects that the April ISM non-manufacturing index will fall to a record low of 37.8 as the services sector is hit hard by the virus. Throughout the day, the FOMC’s Evans (00:00 AEST), Bostic (04:00 AEST) and Bullard (04:00 AEST) will speak at various press conferences.

So, if a bearish Oracle of Omaha and a resumption of trade wars can’t knock the bid on stocks (and by extension the AUD) then will anything?

I still see two candidates. The first is weak recovery, terrible profits and the tsunami of household and SME bad debts sweeping into banks.

The second is this:

The virus is still rampant in the US and across many countries. Via Reuters:

Nearly 135,000 Americans were forecast to die from COVID-19 through the beginning of August, almost double the last prediction, due to loosening of lockdowns, according to an updated forecast from the University of Washington on Monday.

It doesn’t look so much like a second wave as it does a ceaseless infection.

As economies now open up, watch it fly.