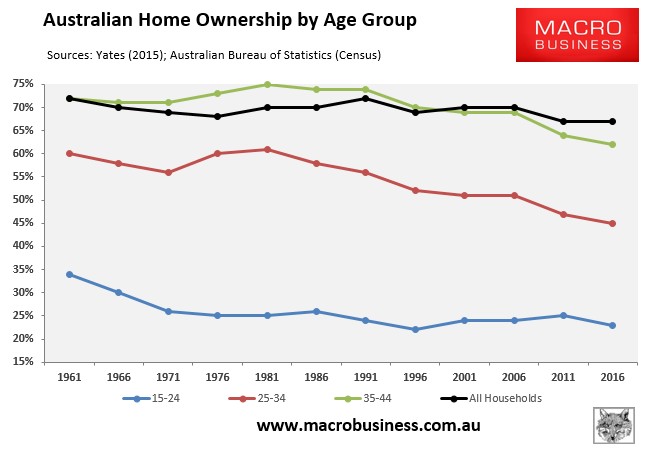

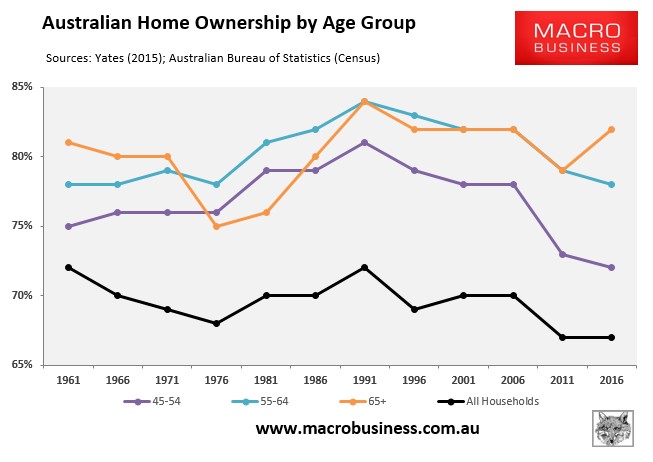

As we already know, Australia’s home ownership rate has been in long-term decline, driven by younger cohorts:

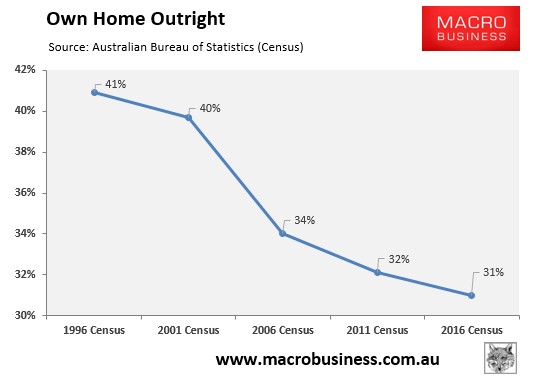

There has also been a bigger collapse in the proportion of households that own their homes outright, from 41% in 1996 to 31% as at the 2016 Census:

Advertisement

New research from the Australian Housing and Urban Research Institute (AHURI) projects that Australia’s home ownership rate will collapse to around 63% by 2040, with younger households again bearing the brunt of the decline:

There appears little chance of Australia sustaining home ownership at current levels. The rate is projected to decline by 2040 to around 63 per cent for all households, and to not much more than 50 per cent—down from 60 per cent in 1981—for households in the 25–55 age bracket.

Declines in ownership seem likely by virtue of attributes of the Australian labour market; continued issues of affordability (despite the 2018–19 price downturn); the proliferation of building forms (apartments) more suited for rental than ownership; and the growth of the private rental sector, underpinned by favourable tax provisions and a housing industry now increasingly path dependent on the private rental sector…

In the domestic context, the projected declines mean Australia will no longer be a near universal ownership society, but must become a dual tenure society of ownership and rental (both private and social). This will require a substantial rethink and redirection of housing and related policy, with a particular focus on how to achieve greater security, affordability and liveability of private rental…

Population growth is a key determinant of housing demand… Relatively inelastic housing supply means that demand shocks—from household income and population growth –tend to be capitalised in property prices and rents, rather than additional dwelling supply…

There is also a secondary effect: properties developed to meet the high land costs were, and still are, typically small one- and two-bedroom apartments; many, as various incidents have revealed in recent years, of poor quality or with structural problems. These by and large are not suitable for purchasing families and most are built for, marketed to and bought by rental investors, many from overseas. Australian cities, most keenly Sydney, Melbourne and Brisbane, have since the 1990s therefore supplied more and more dwellings of a form not designed for or meant for purchasers: purchase choices in the more inner city areas (most notably for families) have therefore been more constrained than in earlier decades…

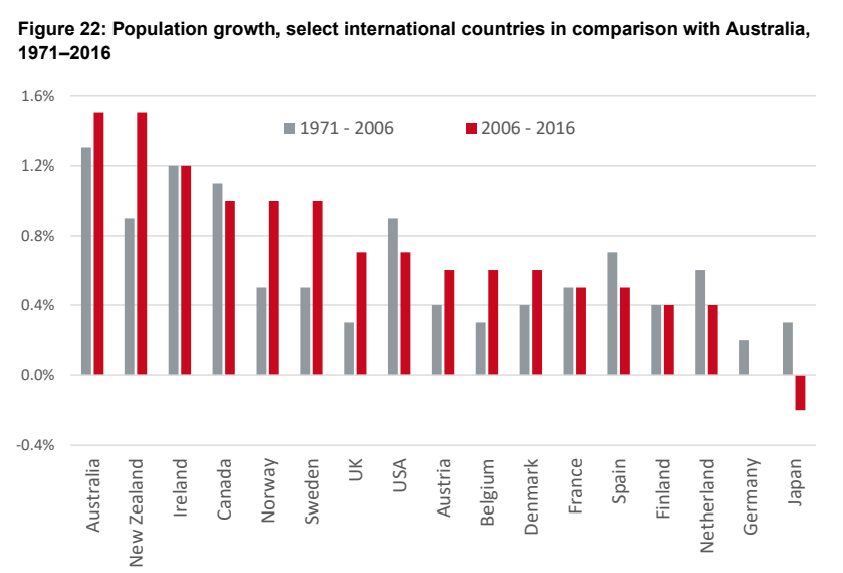

Although there may be hiccups in the inflationary pressures, as in 2018–19, the underlying demographic pressures of Australia, Canada and New Zealand suggest sustained challenges in matching dwelling supply with demand and the associated price pressures. As Figure 22 shows, Australia and New Zealand’s population growth rates are much greater than any of the other countries. Some of these (e.g. Germany and Japan) have effectively zero population growth and it is probably no coincidence that these countries have had very little house price inflation in recent decades…

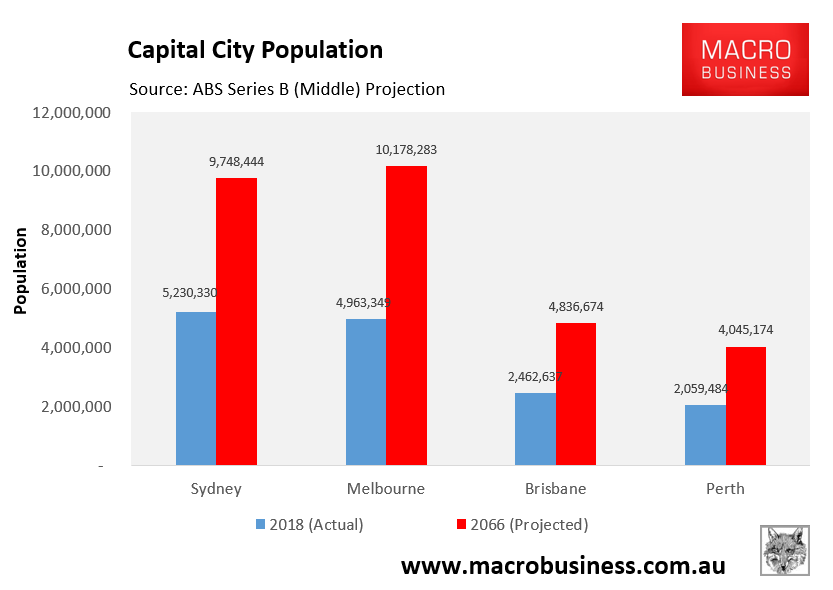

None of this is surprising. With Australia’s major cities projected to roughly double in size over the next 46 years on the back of endless mass immigration:

It is inevitable that home ownership rates will collapse.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.