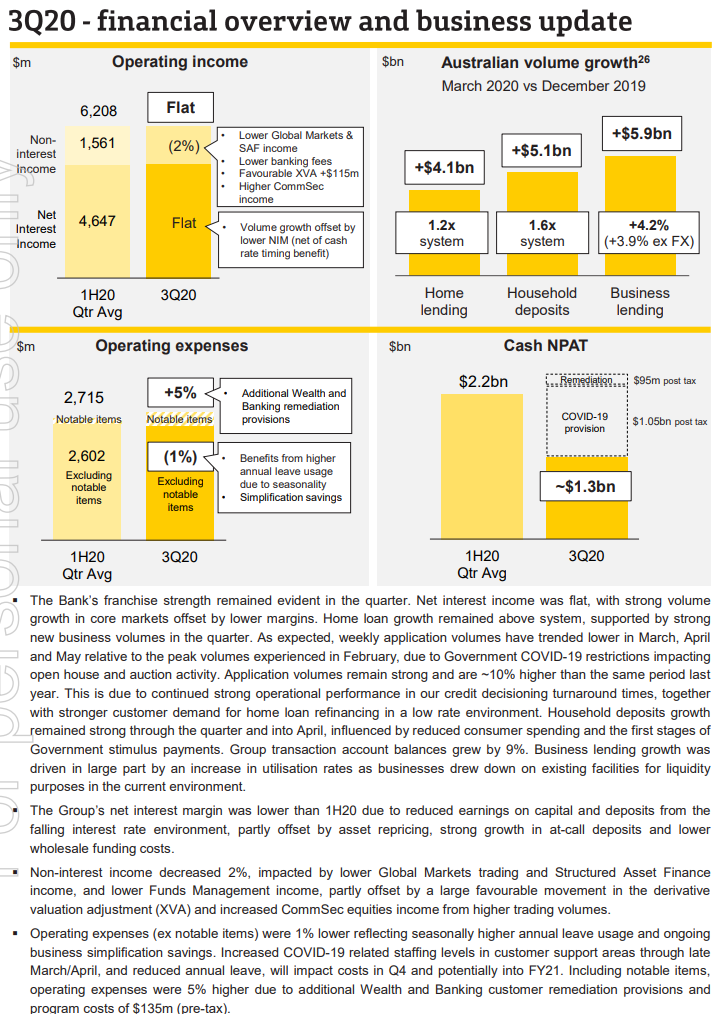

CBA out with its update:

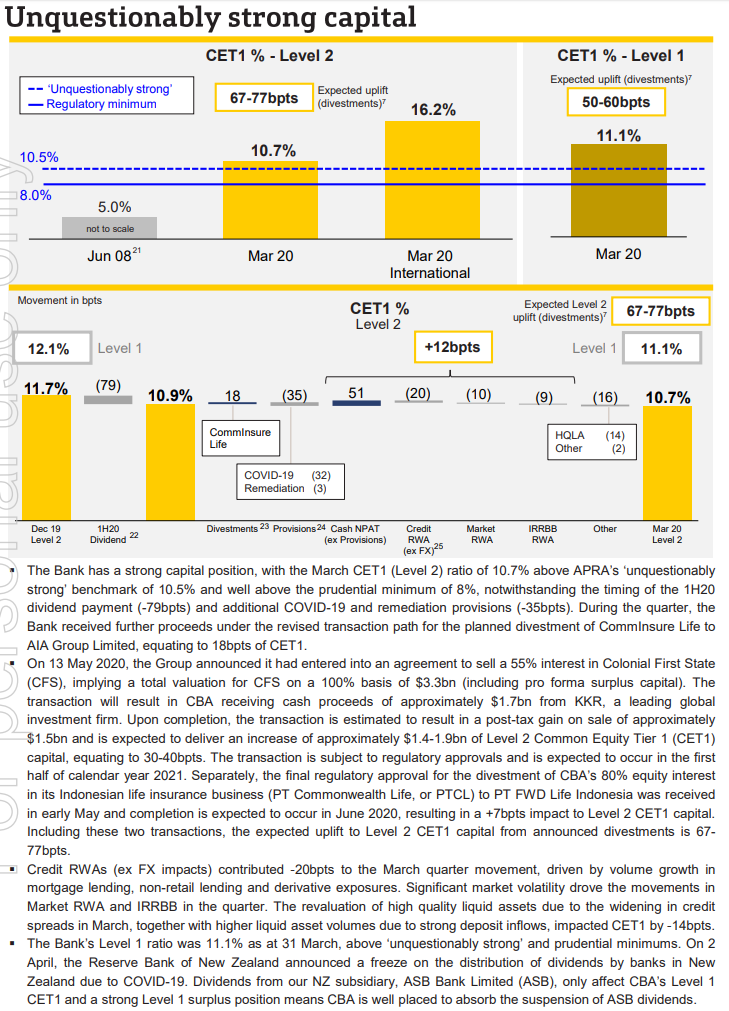

So, profits down 23%. It’s sold Colonial First State to KKR. NIM down despite big deposit flows. Provisions up solidly but not enough. Capital not strong at 10.7% but it’s in line with the other banks so I guess that’s why it has been allowed to continue the dividend. That said, $13bn in forbearance loans is manageable in a portfolio of $1tr of assets.

The bank is clearly outperforming its peers but it simply can’t answer the question being posed by the COVID-19 economy.