As we know, industry superannuation funds have regularly attacked research suggesting that increasing the superannuation guarantee (SG) would cost wage rises and has incessantly lobbied to raise the SG to 12%.

Earlier this week, it was revealed that a “not for citation” paper prepared by Industry Super Australia (ISA), which analysed two decades’ worth of enterprise agreements, found that increases in the SG came at the expense of both wages and jobs:

“In addition to lower wages, costs can also be borne by employers through a reduction in profits, by consumers through increases in prices, or via lower equilibrium employment,” read slides prepared for the presentation to the Centre of Excellence in Population Ageing Research in December…

Industry Super has continually attacked research that has found increasing the super guarantee from 9.5 to 12 per cent will cost workers wage rises, cost the budget billions in tax concessions, and mainly benefit wealthy people and the funds management sector…

Now the AFR View has called out “BigSuper’s” dishonesty, claiming its lies have now been exposed:

Advertisement

Imagine the uproar if a big bank was found out for saying one thing in public to influence a policy debate material to its corporate interests while suppressing incriminating evidence that contradicted its position.

Big Super has now been found out for doing just this after trying to deny that the scheduled increase in workers’ compulsory superannuation payments – from 9.5 per cent to 12 per cent of wages over the next five years – will have to be paid for by some combination of reduced take-home pay, jobs or profits…

This finally moves the debate on to more solid ground already occupied by the Henry tax review a decade ago, the Reserve Bank of Australia, the Grattan Institute and the Australian Council of Social Service.

The political advocacy of Big Super has been reluctant to cede the point because it might strengthen the push by Liberal MPs to dump the scheduled super contributions increase.

Raising the SG would increase inequality, given superannuation concessions overwhelmingly favour high income earners.

Raising the SG would reduce workers’ take-home pay, thereby punishing lower-income earners living paycheck to paycheck, as well as sucking demand out of the economy while it is still trying to recover from COVID-19.

Raising the SG would cost the federal budget more than it saves in Aged Pension costs.

Advertisement

On the specific issue of the SG lowering wages, the evidence is overwhelming.

Even slower wage growth will be the result of increasing compulsory superannuation contributions from 9.5 per cent to 12 per cent…

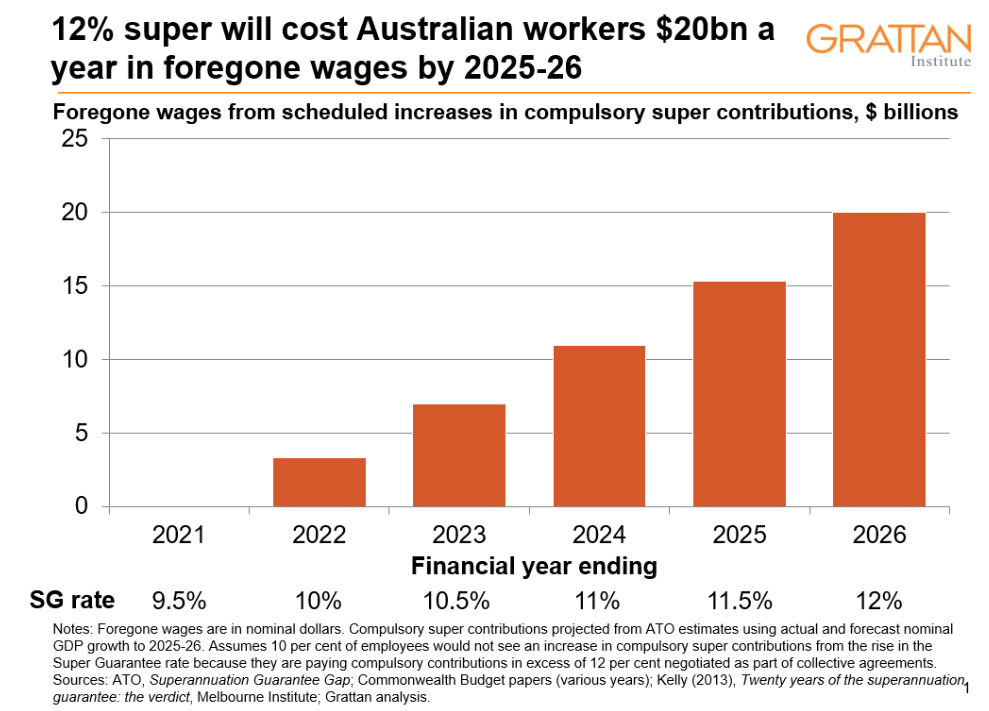

If compulsory super contributions go up, wages will be lower than they otherwise. And the cut to wages from raising compulsory super is big. Really big. By the time it’s fully implemented in 2025-26, a 12 per cent Super Guarantee will strip up to $20 billion from workers’ wages each year, or nearly 1 per cent of GDP…

RBA assistant governor Luci Ellis said it had “shaved” its worker pay forecasts to reflect that higher compulsory super will dampen future wage growth for private sector workers…

“Historically about 80 percent of the increase in the non-cash benefit tends to show up as somewhat slower wages growth than what you would have otherwise seen.”

Although employers are required to make superannuation guarantee contributions, employees bear the cost of these contributions through lower wage growth. This means the increase in the employee’s retirement income is achieved by reducing their standard of living before retirement…

The retirement income report recommended that the superannuation guarantee rate remain at 9 per cent. In coming to this recommendation the Review took into the account the effect that the superannuation guarantee has on the pre-retirement income of low-income earners.

Because it’s wages, not profits, that will fund super increases in the next few years. Wages are the seedbed of the whole operation. An increase in super is not, absolutely not, a tax on business. Essentially, both employers and employees would consider the Superannuation Guarantee increases to be a different way of receiving a wage increase.

Advertisement

And here’s former Labor Prime Minister and Treasurer, Paul Keating:

The cost of superannuation was never borne by employers. It was absorbed into the overall wage cost… In other words, had employers not paid nine percentage points of wages as superannuation contributions to employee superannuation accounts, they would have paid it in cash as wages.

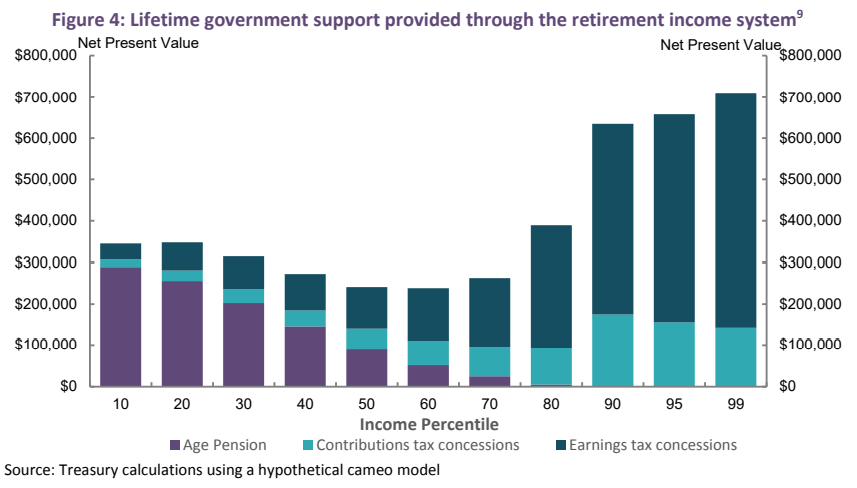

Perhaps even worse, 12% superannuation will also worsen inequality, since the lion’s share of concessions flow to high income earners, according to the Australian Treasury:

Advertisement

Moreover, because it gives higher income earners the lion’s share of concessions, compulsory superannuation costs the federal budget more than it saves in Aged Pension costs. The Grattan Institute, the Henry Tax Review, and actuarial firm Rice Warner are explicit on this point.

Indeed, the Grattan Institute estimates that lifting the SG to 12% would cost the federal budget an additional $2 billion a year in lost income:

Advertisement

In both the short and long term, though, superannuation costs the budget more than it saves, because the tax breaks cost the government more than the pension savings…

The only real winners from lifting the SG to 12% are the industry, which would get to ‘clip the ticket’ on bigger funds under management. This is why they continually obfuscate the evidence to talk their own book.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.