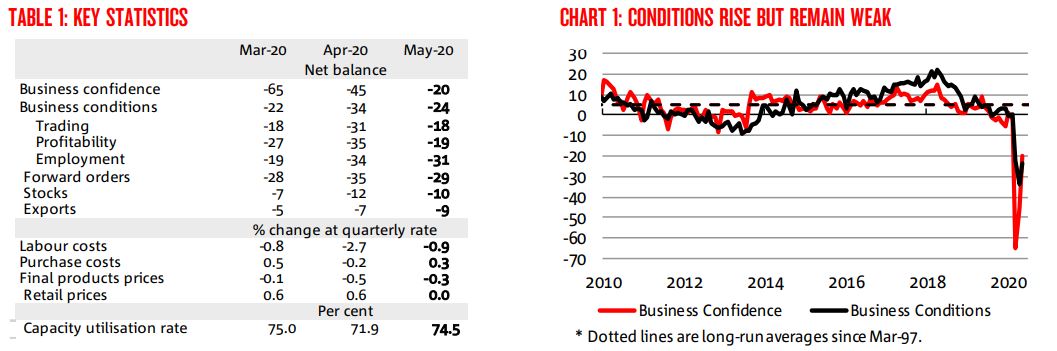

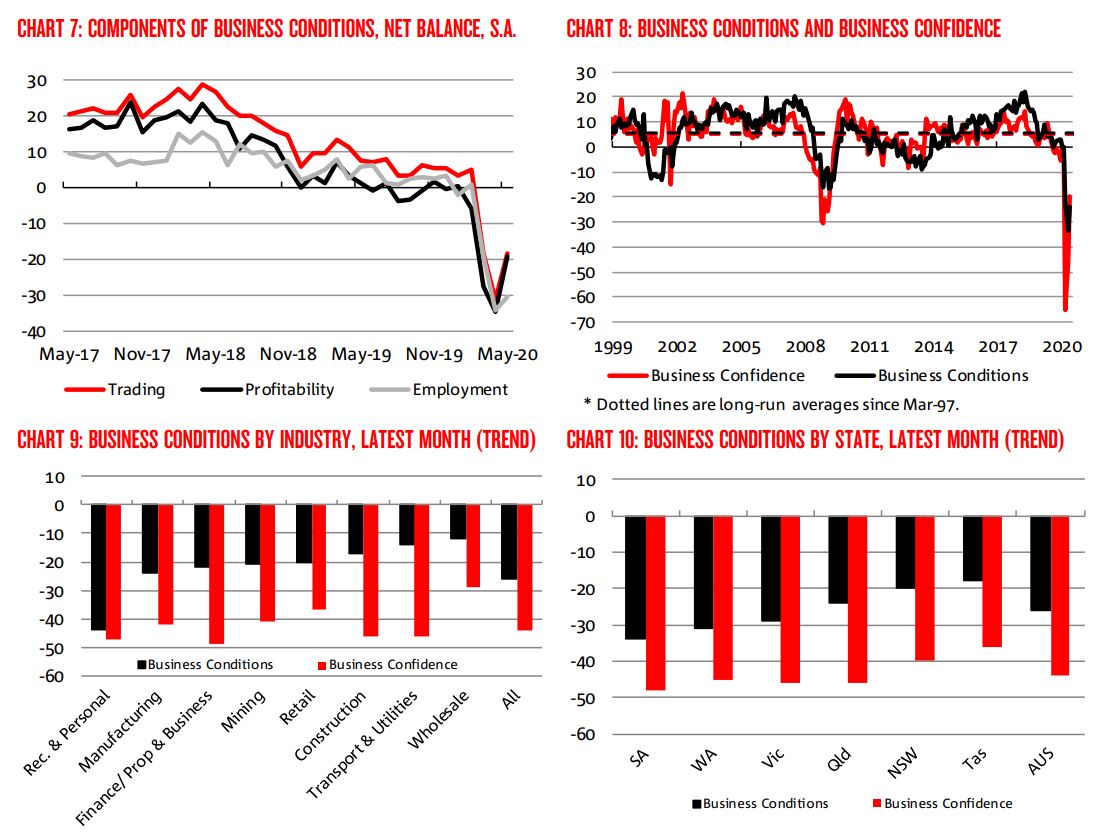

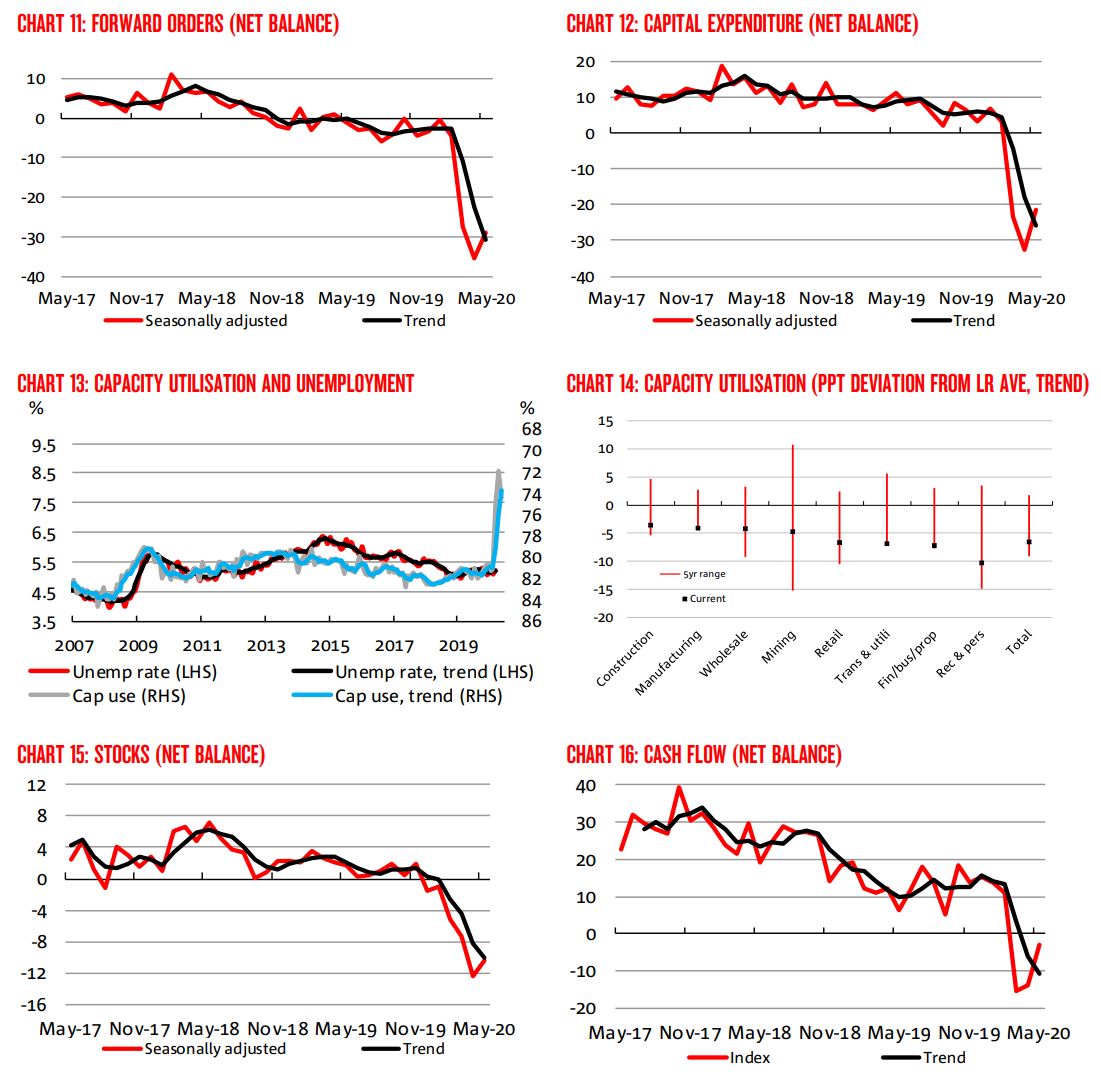

Business conditions saw a broad-based improvement in the month but remain deeply negative – at a level last seen coming out of the GFC. The services sectors remain weakest, but all sectors continue to see negative conditions. Business confidence increased further from its low point in March, but remains weak with a current reading last seen around the trough in the 1990s recession. The increase in confidence was also broad-based across the economy but all industries continue to expect a deterioration in conditions. Overall, this month’s results accord with what we have seen elsewhere, with restrictions having generally been eased – though to varying degrees across the states – there has seen some pickup in activity. However, uncertainty remains high both globally and domestically and businesses likely remain concerned about how quickly they will return to full capacity. Unsurprisingly the employment index – which appears to have stabilised – and capex remain very weak. Both indicators point to ongoing restraint in the business sector with respect to hiring and expansion plans. Indeed, while capacity utilisation saw some improvement, it remains historically low, and well below pre-COVID-19 levels. Forward orders, also near record lows, suggest activity will remain weak in the near term.

Disastrous:

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.