Monetising deficits has started. Expect it to stay.

The helicopters have arrived. Central banks are printing money to fund expanding government deficits. I expect them to stay: fiscal will remain the lead instrument for cycle management through the coming expansion, and it will be backstopped by central banks. Deployed with sufficient vigour – which will be a matter of political will, not ability – this will end the era of secular stagnation.

The Fed is now fully monetising the expansion of the US Federal budget deficit. The Fed isn’t directly crediting money to the Government – the Treasury bonds are being laundered by a fleeting period of private sector ownership – but this is in every way that matters pure monetisation.

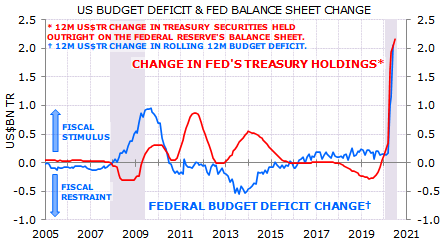

Exhibit 1 shows the 12 month change in the budget deficit – the deficit over the year to June was $2.1tr larger than the deficit over the year to June 2019 – and the 12 month change in the Fed’s Treasury holdings. At the end of June the Fed owned $2.2tr more Treasuries than it did in June 2019. Bingo.

Exhibit 1 also shows how this cycle differs from the prior cycle. Budget deficits widened amidst the GFC, but there was no synchronisation with Fed balance sheet changes. More to the point, the waves of quantitative easing through the subsequent expansion (the periodic increases in the red line in Exhibit 1) coincided with fiscal contraction. QE proved to be an ineffectual macro stimulant, while fiscal tightening was a significant headwind for growth. Policy will be much more effective boosting growth now than it was in the prior cycle because it is being led by fiscal.

A few follow-on points:

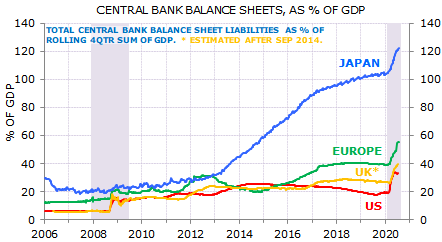

First, the Federal Reserve continues to have a ‘small’ central bank balance sheet, at least when balance sheets are measured relative to the size of the economy (Exhibit 2). (Note that Exhibit 2 shows the size of the overall balance sheet, while Exhibit 1 showed the change only in the Fed’s outright holdings of Treasuries, not all Fed assets.)

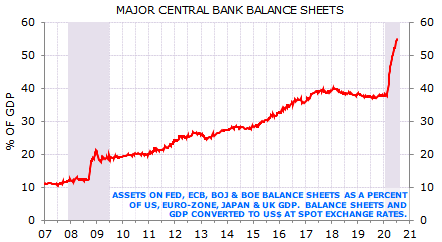

Second, de facto monetisation is occurring throughout the developed economies. The IMF estimates that the fiscal measures in response to the Covid-19 crisis now amount to just under 10% of GDP in the developed economies. The aggregate balance sheet of the major economy central banks has already increased by 15% of GDP (Exhibit 3).

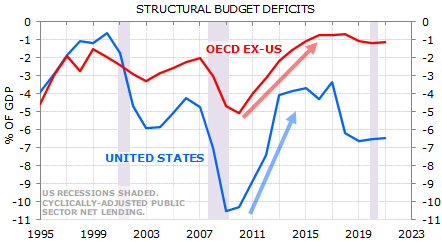

Third, as with the US, there are already signs outside the US that policy will be different in the post-Covid-19 expansion compared to the post-GFC expansion. Fiscal policy was tightened throughout the developed economies in the aftermath of the GFC (Exhibit 4, which includes clearly overtaken-by-events OECD forecasts for fiscal policy this year and next). Fiscal tightening led to secondary recessions in Japan, UK and Europe. The idea of ‘expansionary austerity’ proved to be as daft as it sounded. It is clear that there will be no repeat of post-crisis fiscal tightening in this cycle. It also seems clear that central banks outside the US will stand ready to backstop ongoing fiscal expansion.

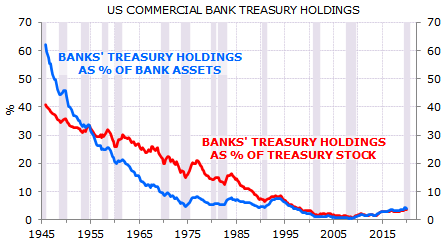

Fourth, the fact that central banks are backstopping the expansion in public sector debt loads reduces a major risk for private banks. The deleveraging of government balance sheets in the aftermath of World War 2 was facilitated by a rigged financial system. Effectively governments forced the private sector to hold government bonds, artificially supressing yields. The banks were the biggest loser: Treasuries were a major component of bank balance sheets (Exhibit 5). This sort of financial oppression is much less likely if central banks become the largest buyer of government debt.

Secular stagnation is first and foremost a problem of excess saving: the private sector’s planned saving exceeds planned investment. The public sector running sufficiently large deficits can be an effective antidote to secular stagnation. It seems likely that the Covid-19 crisis will make acceptable the use of sustained, aggressive fiscal stimulus backstopped by central bank balance sheet expansion. The test of whether this change has occurred is not what is happening now amidst the crisis. The real test will be whether policy makers continue to use fiscal stimulus through the recovery phase. I think they will. And if that’s the case then it will reverse many of the investment trends of the past 30 years.

And that’s how far behind the times that the RBA and Scummo are.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.