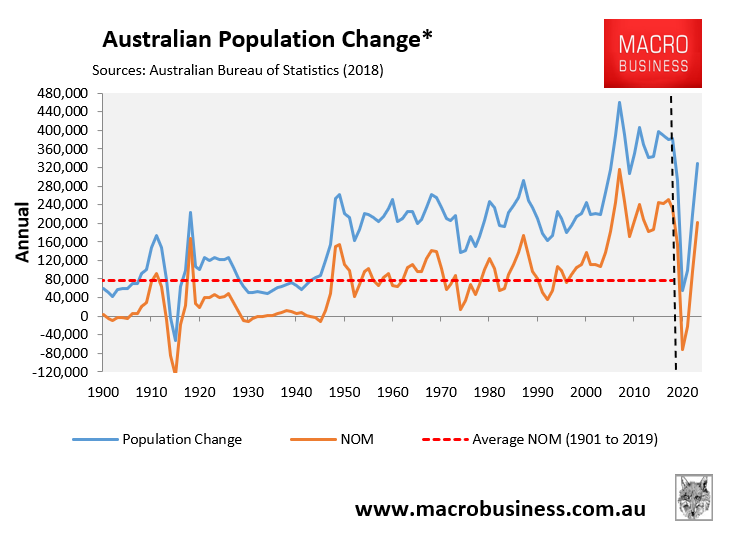

As reported earlier, the federal government has forecast Australia’s first outward movement of net overseas migration (NOM) since the Second World War, which will drive Australia’s population growth to its lowest level since 1942:

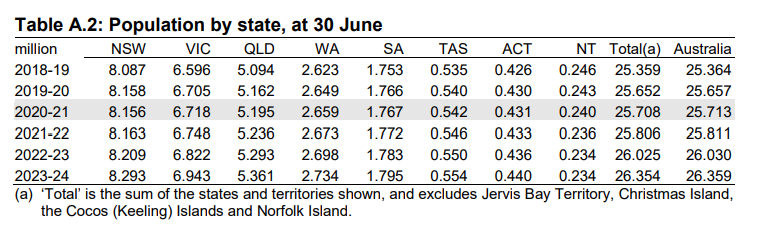

Population growth across Australia’s jurisdictions is also forecast to slow dramatically, with NSW’s population even forecast to fall slightly in 2020-21:

One of the key areas that will be impacted most heavily from the collapse in immigration is Australia’s property market, with the migrant epicentres of NSW (Sydney) and Victoria (Melbourne) most impacted.

Indeed, with dwelling construction still running at elevated levels, key housing markets across Australia are facing unprecedented gluts as new supply is added at a far quicker pace than population growth.

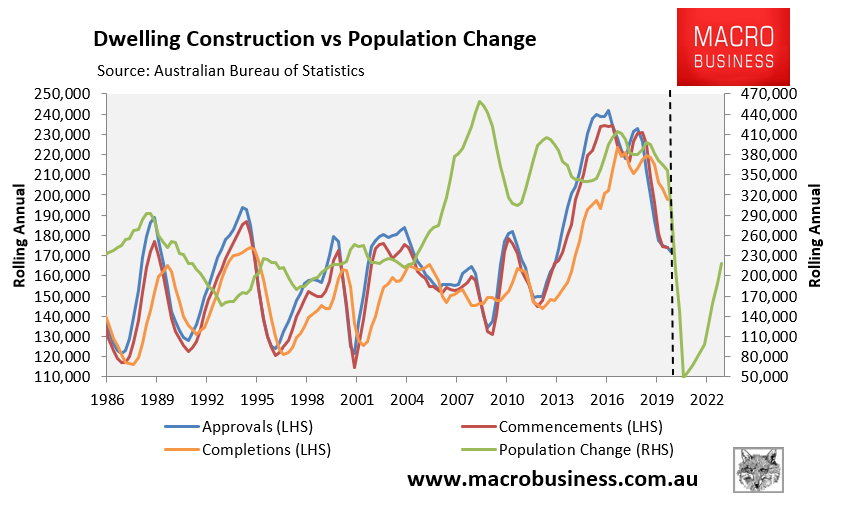

Presented below are charts tracking historical and projected population growth against dwelling approvals, commencements and completions, which illustrate the supply gluts coming down the pipe.

First, below is the national picture, with annual population growth forecast to crater to just 50,000 in March quarter 2021 versus dwelling construction of around 180,000 dwellings:

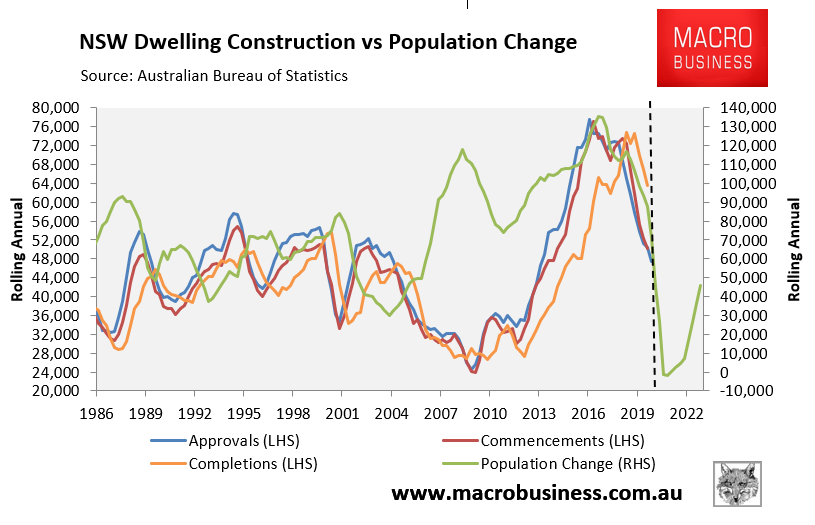

Next we have NSW where population is forecast to decline by 2,000 in the year to June 2021 versus dwelling construction of around 45,000:

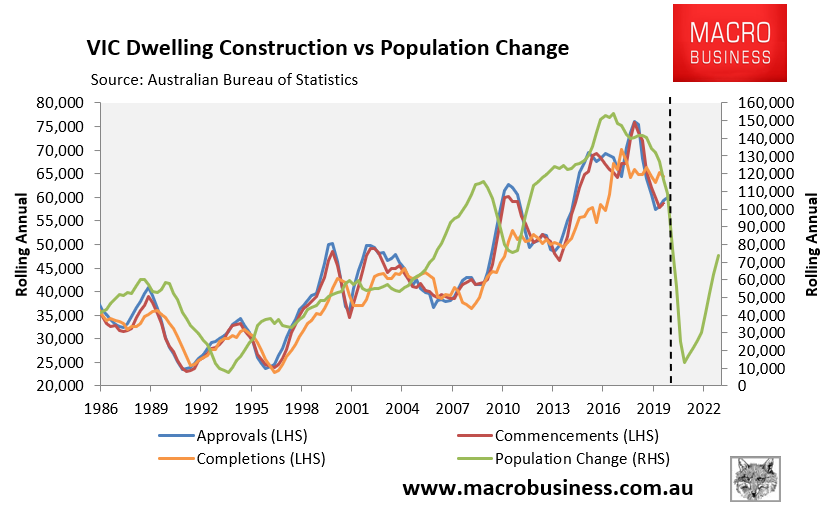

Next is Victoria where annual population growth is forecast to bottom at 13,000 in June 2021 versus dwelling construction of around 60,000:

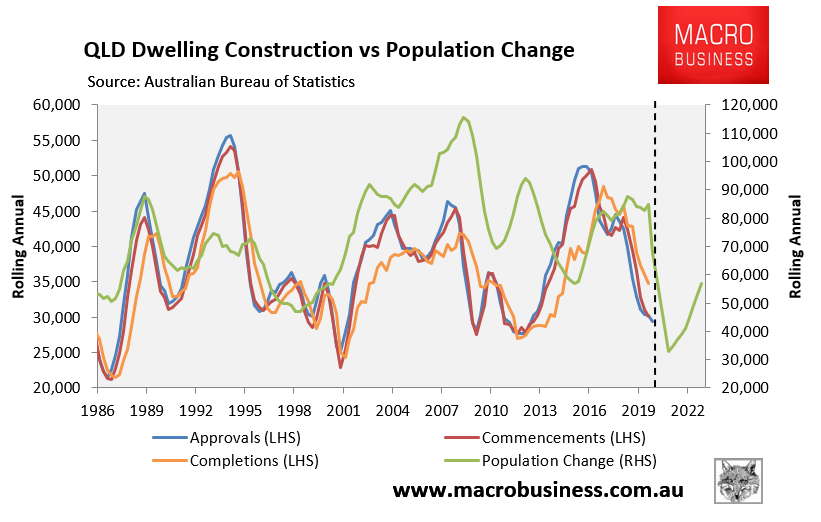

Next is QLD where annual population growth will crater to 33,000 in June 2021 versus dwelling construction of around 30,000:

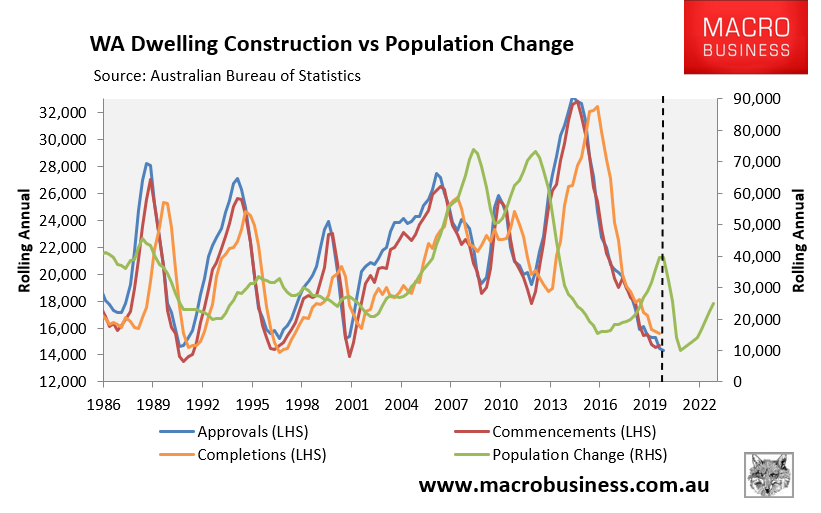

Next is WA where annual population growth is forecast to bottom at 10,000 in June 2021 versus dwelling construction of around 14,000:

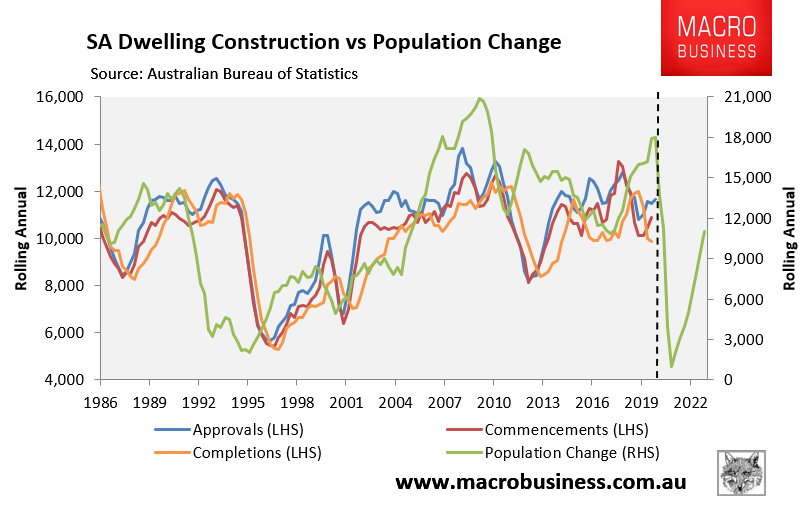

Finally, SA’s annual population growth is projected to crater to 1000 in June 2021 versus dwelling construction of around 10,000:

There’s no sugar coating this data: Australia’s property market is facing an unprecedented housing oversupply with the migrant epicentres of Victoria (Melbourne) and NSW (Sydney) facing the biggest gluts.

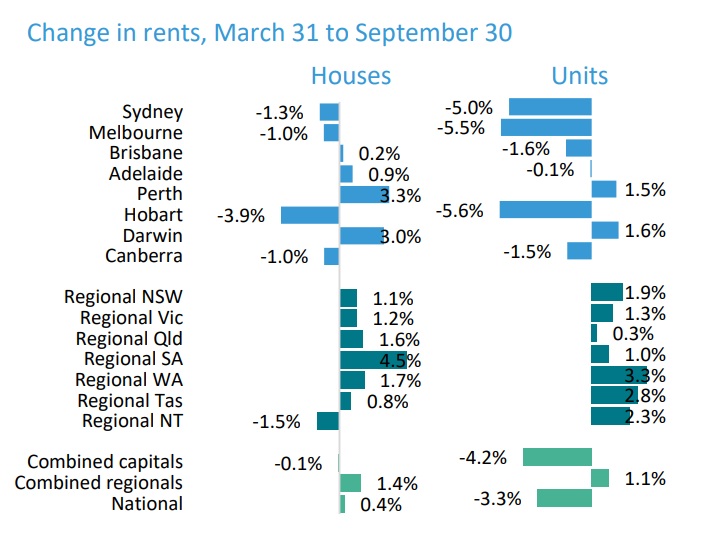

This ensures that rental vacancies will continue to balloon and rents will continue to fall, with apartments most impacted:

It is therefore shaping up to be a disastrous period ahead for financially stressed and highly leveraged landlords.