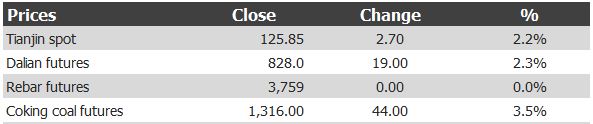

Daily iron ore price update for October 10, 2020:

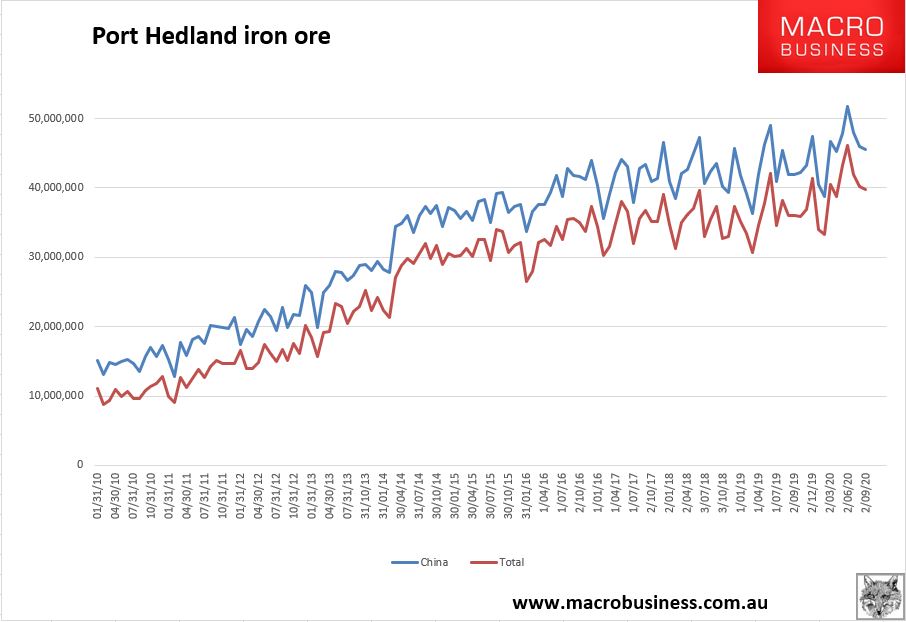

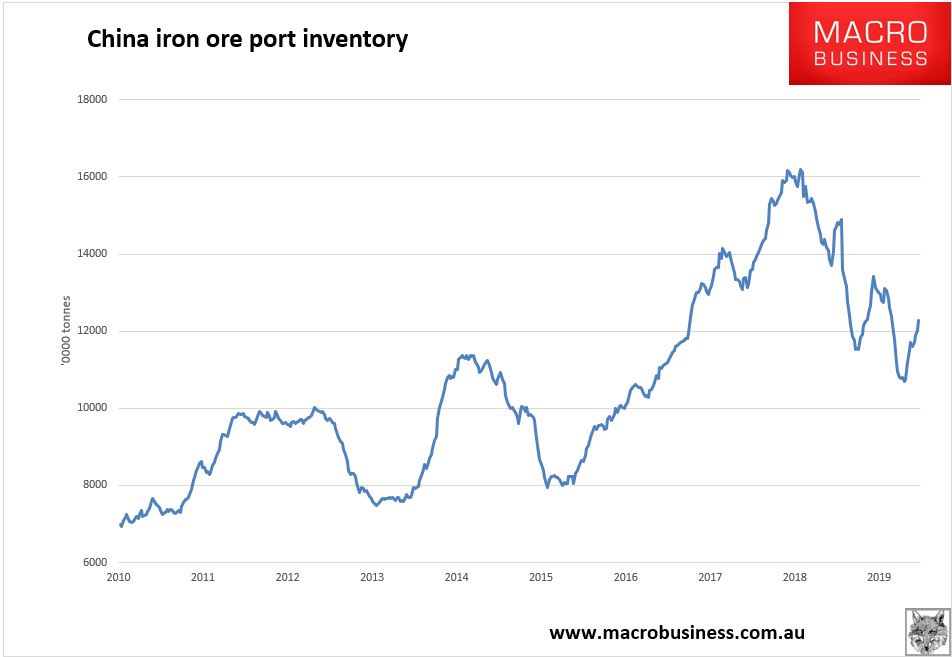

Spot jumped after Golden Week. Paper too. Port Hedland output has eased as Brazil ramps up. Chinese port stocks are climbing at a goodly pace, now at 122.7mt. I expect them to keep on going all way the to 160mt and possibly higher if Beijing has given the order for a strategic reserve. That is going to push this restocking right through to mid-2021. This adds an annualised 100mt plus to apparent demand. That is strong price support while that lasts, especially amid Brazil’s problems, despite a few better months recently.

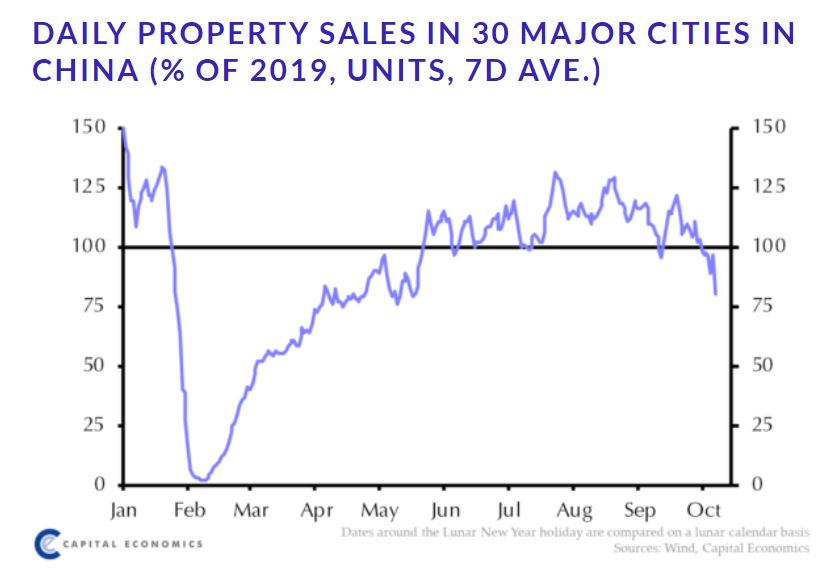

On the other hand, underlying demand is not great. Golden Week empty apartment sales were poor:

That’s a bit of shock. One wonders if Evergrande’s problems, and extreme discounting, have led to falling inflation expectations among Chinese buyers.

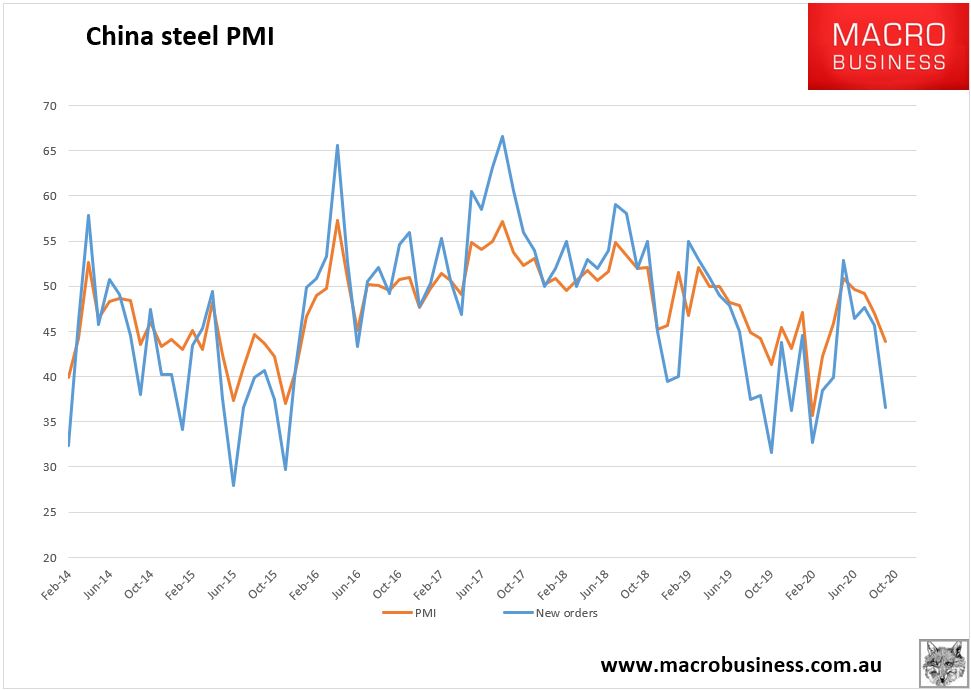

In truth, new orders in the steel PMI are very weak as well:

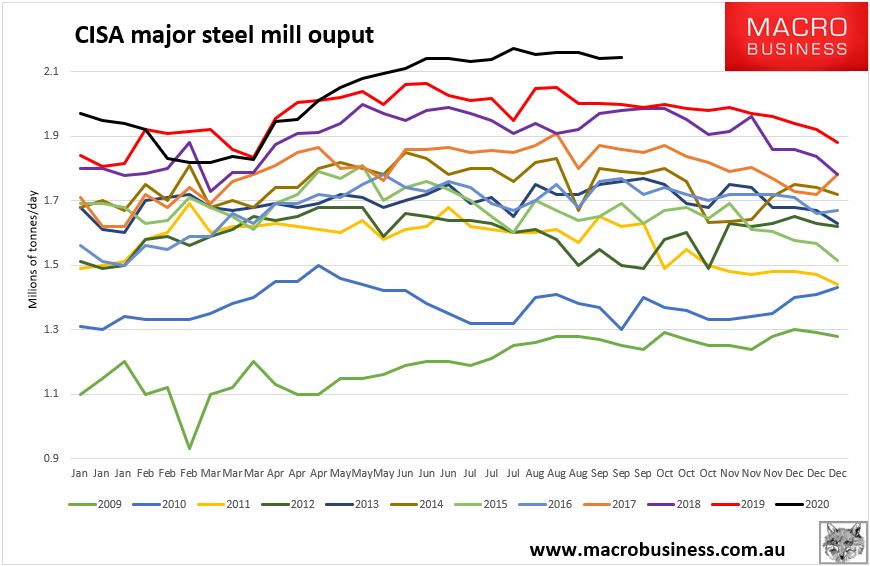

But production is still extreme:

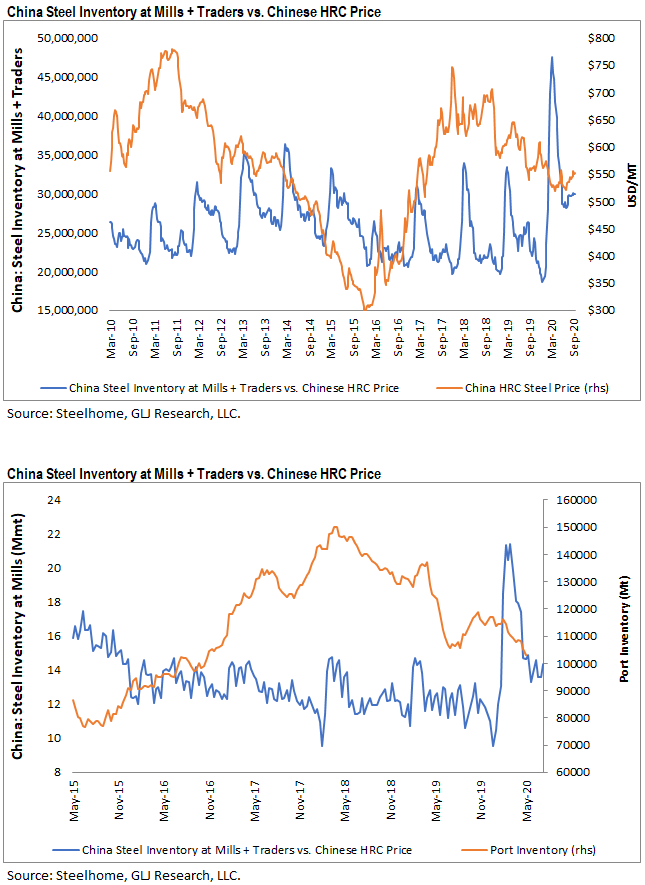

Which is also playing out in staggering steel inventories, the highest by far seasonally adjusted in history:

Iron ore is less predictable than the old days given it now dances to the beat of wider risk sentiment in commodity markets. So, if the current rally persists, which seems pretty stupid to me given no more US stimulus, election and thrid wave virus risk, then so might iron ore. If not, I still think there’s scope here for further seasonal weakness.

That said, we’re fast running into the new year restock so if it does come then it had better be quick!