DXY was soft last night as EUR flew:

The Australian dollar is still flying free:

Gold and oil eased:

Metals were mixed:

Miners rolled:

EM stocks too:

Junk is fine:

Treasuries bid:

Stocks held:

Westpac has the wrap:

Event Wrap

Europe announced further Covid-related restrictions. Following record daily cases and deaths on Friday, Germany is urging, but not requiring, employers to close workplaces as it starts a hard lockdown on Wednesday. Italy and the Netherlands are among the countries expected to tighten restrictions as well. The UK announced London and SE England will start Tier 3 restrictions on Wednesday.

Comments from EU officials suggesting that there were few positive developments in UK/EU trade negotiations quashed earlier reports (including from EU Chief negotiator Barnier) that there had been some progress.

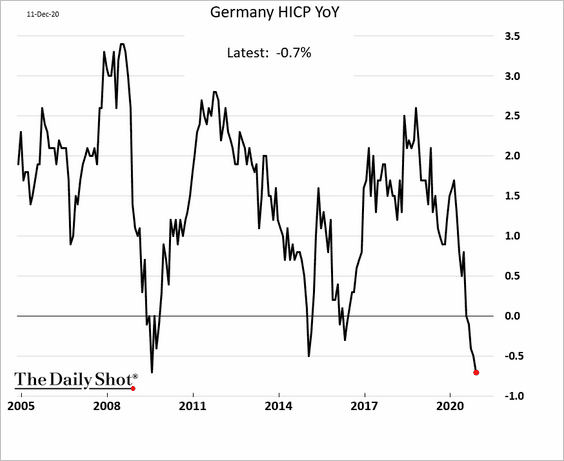

Eurozone October Industrial production rose +2.1%m/m (est. +2% m/m), although production is expected to be more severely hit by the Covid-related restrictions imposed across Europe through November. The September reading was revised from -0.4%m/m to +0.1%m/m, taking the annualised reading in October to -3.8%y/y (est. -42%y/y).

Event Outlook

Australia: The RBA will publish the Minutes of the December Monetary Policy Meeting – the Bank will remain in “watch–and–wait” mode after delivering November’s stimulus. Following this, the RBA’s Kearns (Head of Financial Stability) will speak at the Australasian Finance and Banking Conference. The Q4 AusChamber–Westpac business survey will provide an update on business conditions as the economy reopens. ABS Weekly Payrolls for the week-ended 25th November will be released; the recent collapse in small business payrolls has been key to soft prints.

New Zealand: The Q4 Westpac-McDermott Miller Consumer Confidence Survey will capture several significant developments, including the easing of restrictions, the strengthening of activity, a rapid rise in house prices, and positive news around the development of a vaccine.

China: Key November releases will provide further insight into China’s recovery, including industrial production (market f/c: 2.3%yr YTD), retail sales (market f/c: -4.9%yr YTD), and fixed asset investment (market f/c: 2.6%yr YTD).

UK: The ILO unemployment rate is expected to tick up to 5.1% in October, but the furlough scheme will continue to provide support until March 2021.

US: The December Fed Empire State Index (market f/c: 6.9) and November industrial production (market f/c: 0.3%) will reveal the impact of surging cases and reimposed restrictions.

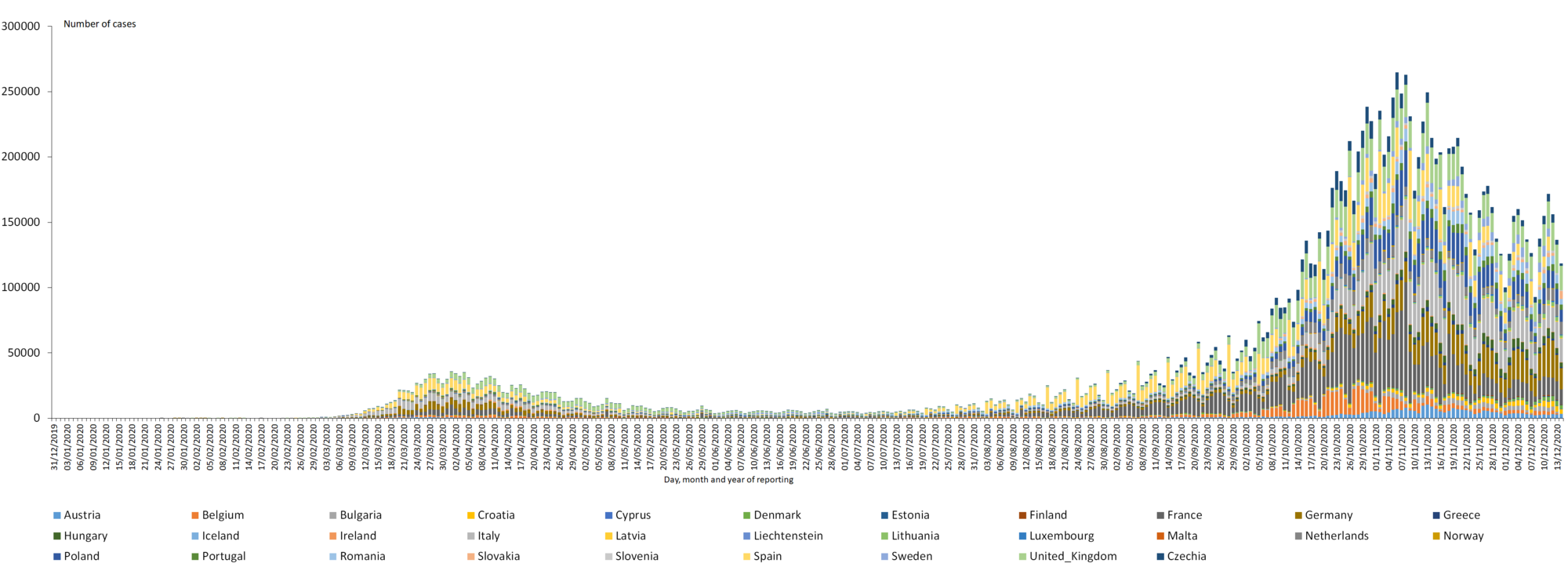

Nothing much new here. The US and European pandemics are slowly improving:

On lockdowns:

But the market is still more focussed on the big bang of vaccines, that began to roll out last night:

So long as the vaccine catch-up growth story holds then DXY will fall and AUD rise.