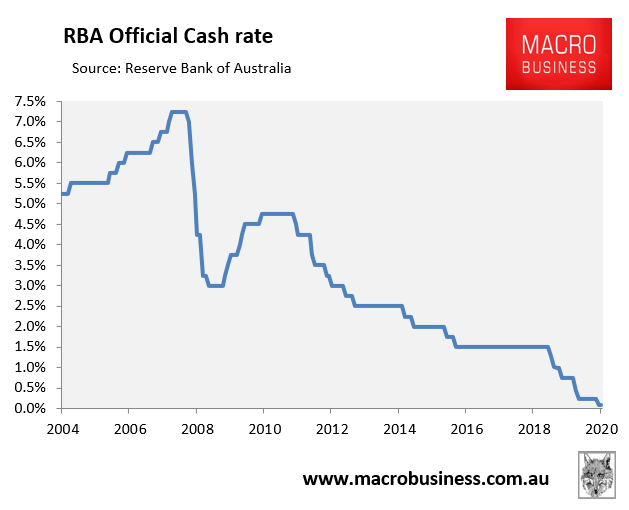

We had previously operated under the wrong assumption that the 30-year decline in mortgage rates had run its course given the RBA official cash rate (OCR) had little further room to fall:

That is, with the OCR hitting its lower bound, we wrongly believed that banks would have minimal ability to cut deposit and wholesale borrowing rates without compressing their net interest margins. Accordingly, we believed mortgage rates could not fall any lower.

Our assumptions were thrown out the window with the RBA’s Term Funding Facility (TFF), which has successfully driven mortgage (and other borrowing) rates lower.

The TFF was announced in March 2020 as part of a monetary policy package to reduce funding costs across the economy and to support lending. However, we were slow to register its significance.

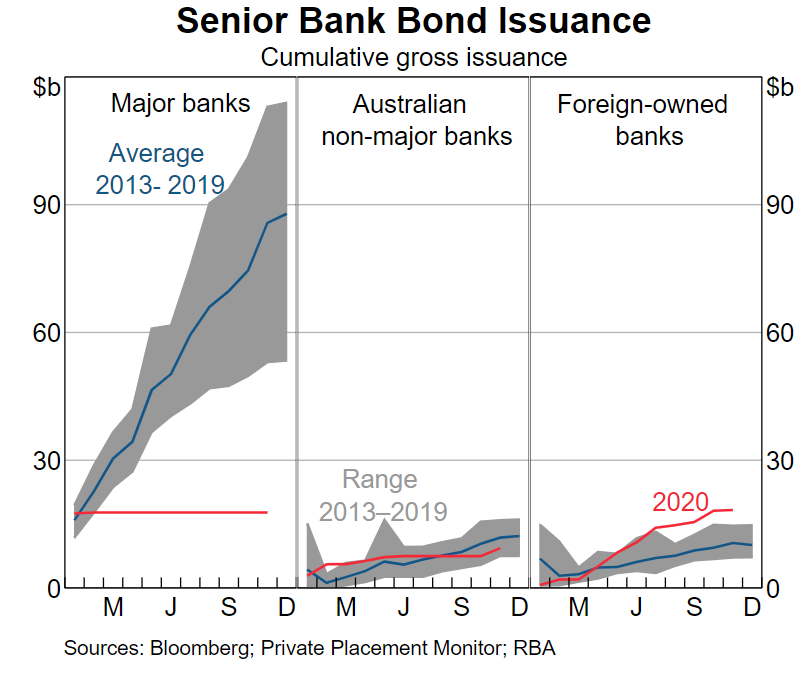

The TFF provides low cost three-year funding for authorised deposit-taking institutions (ADIs) to support the supply of credit. And it has been highly successful in replacing relatively expensive wholesale funding with cheap funding from the RBA:

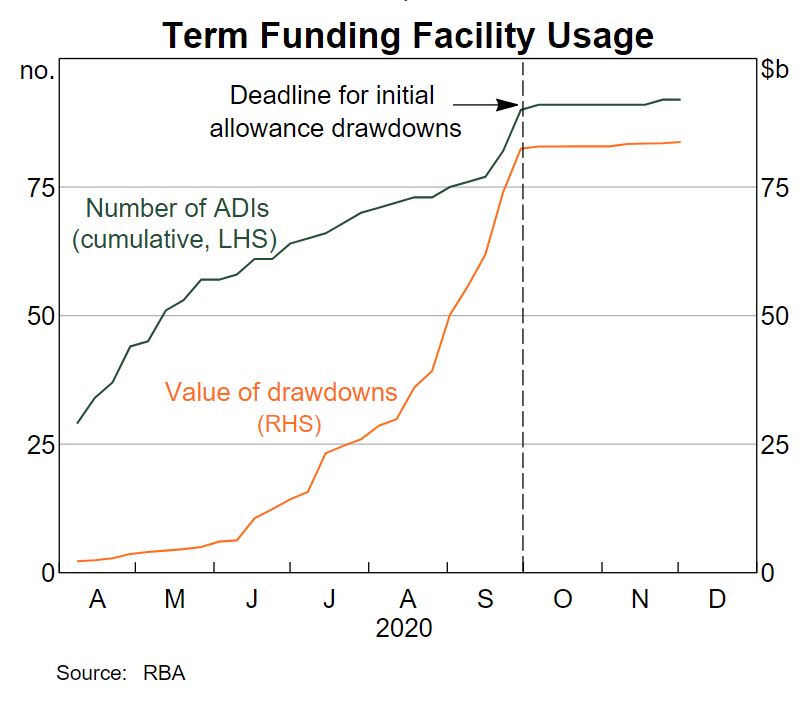

Most of the initial allocations of the TFF were drawn upon by the time the first phase of the facility closed in September. Then the RBA Board adjusted the TFF in response to economic conditions, expanding and extending the facility, and in November it lowered the interest rate on new drawings to only 0.10% (from 0.25%).

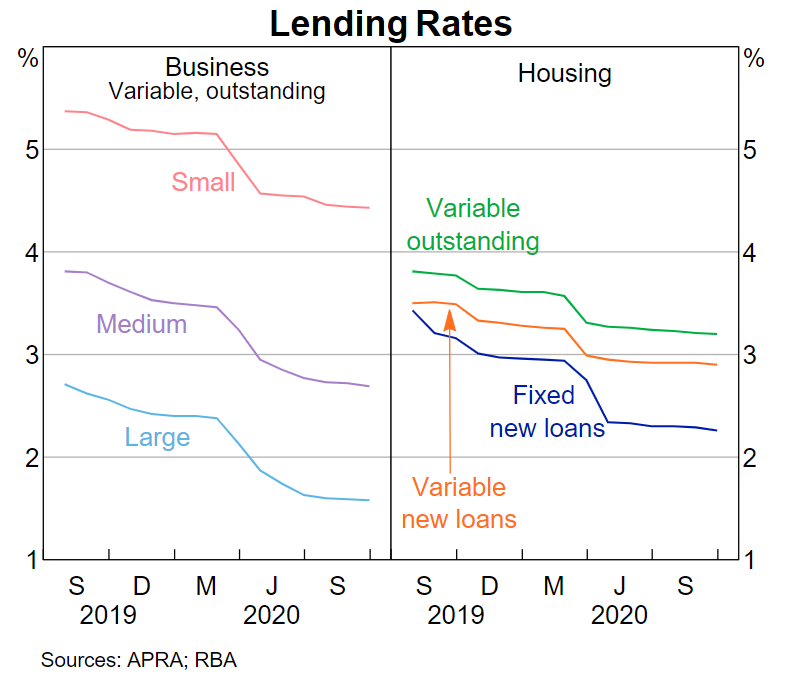

The TFF has successfully lowered mortgage borrowing rates, especially fixed mortgages:

There is also a high likelihood that Australian mortgage rates could fall lower still judging by what’s happened in Europe.

The European Central Bank started with 0.1% funding for banks in 2014. By 2016 the rate was -0.4%. And now it’s -1.0%. Yes, the central bank will pay commercial banks up to 1% if they can just find someone (anyone!!!) who will just borrow the money.

Indeed, the nation with the the longest history of negative central bank rates – Denmark – has begun offering homeowners 20-year loans at a fixed interest rate of zero:

Customers at the Danish home-finance unit of Nordea Bank Abp can, as of Tuesday, get the mortgages, which will carry a lower coupon than benchmark US 10-year Treasuries. At least two other banks have since said they’ll do the same…

Back in 2012, policy makers drove their main rate below zero to defend the krone’s peg to the euro. Since then, Danish homeowners have enjoyed continuous slides in borrowing costs.

The once unthinkable notion of borrowing for two decades without paying interest comes as central bankers across the globe shy away from rate hikes.

This is an amazing development that could be a harbinger of what lies ahead for Australia.

If the RBA follows Europe’s path, we could soon see the TFF providing negative interest rates and plunging fixed mortgage rates well below 2%.

The RBA put remains in play.