Since COVID-19 struck and Australia’s nanny state kicked into gear, office occupancy has cratered. Whether this is a long-term phenomenon as work from home takes hold is a crucial question. Commercial construction is a decent driver of economic activity.

Via the Property Council:

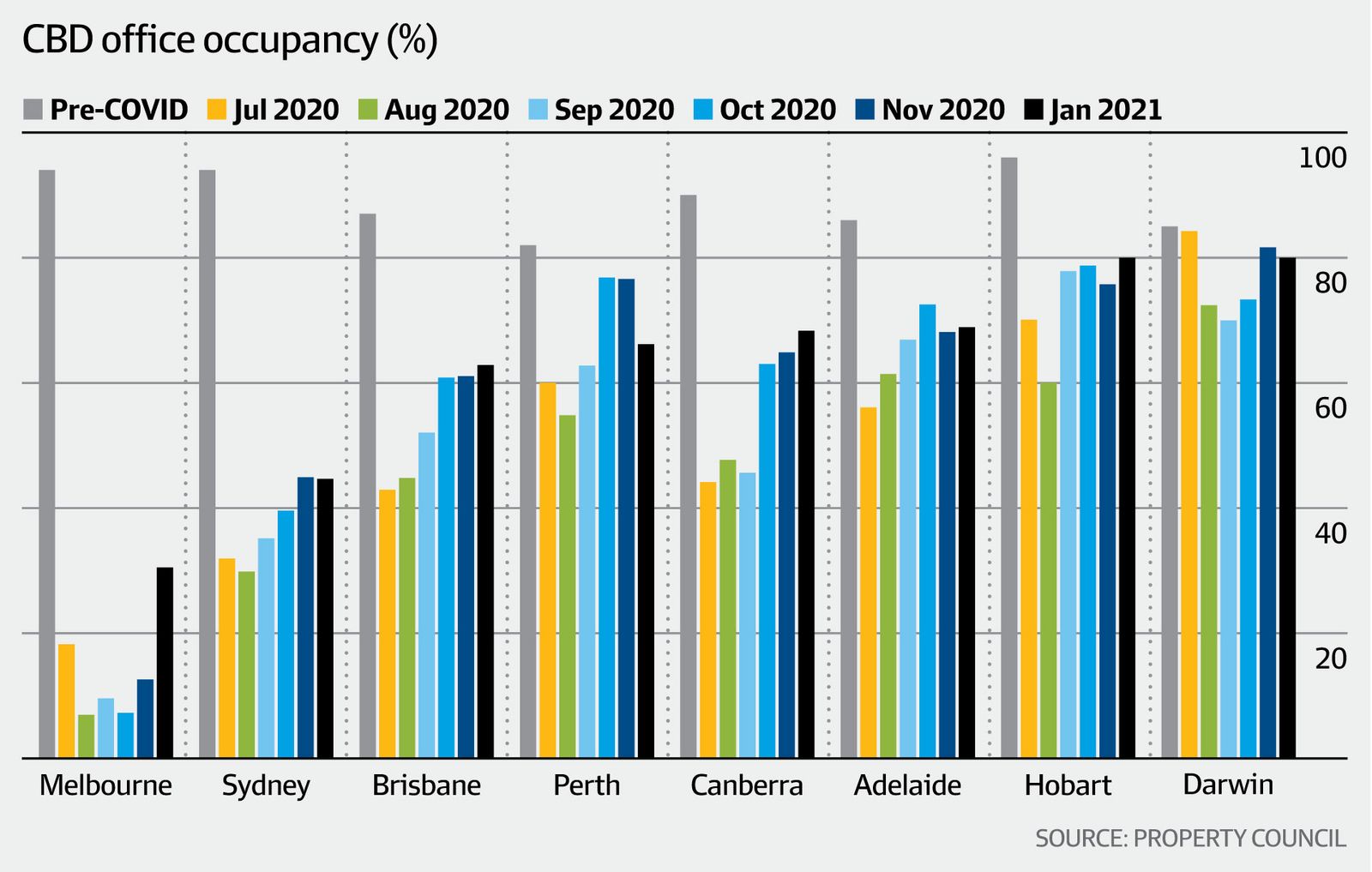

Melbourne’s office occupancy rate increased to 31 per cent in January but still lags the nation following Victoria’s extended lockdown and prolonged work from home orders throughout 2020.

The Property Council of Australia’s periodic Office Occupancy Survey shows an increase from 13 per cent in December, after reaching a low of 7 per cent in October, and reflects a renewed confidence and the Victorian Government’s safe and progressive roadmap to the reopening of offices.

Melbourne’s office occupancy levels fall behind Sydney’s, which sits at 45 per cent. All other capital cities currently enjoy occupancy levels greater than 60 per cent.

Only a small percentage of survey respondents consider that workplace safety concerns are contributing to lower occupancy levels, whereas over 20 per cent consider public transport safety and capacity concerns to be influencing occupancy and nearly 40 per cent cite changed workplace preferences.

Over 50 per cent of survey respondents think that it will take more than 3 months to see a material increase in occupancy levels.

Office occupancies are calculated on whether a tenant’s employees are occupying the space or working from home, not whether a lease is in place. The Property Council has been surveying our members who specialise in the office sector to track progress in the return to office.

This week’s Occupancy Survey release follows last week’s important Property Council of Australia Office Market Report, which showed that Melbourne’s office vacancy had reached 8.2 per cent, reflecting an influx of new office supply and an increase in subleasing activity.

In addition to the bi-annual Office Market Report, the Property Council of Australia is actively tracking office occupancy data through our periodical Office Occupancy Survey. All data collected across Australia’s capital cities, has been aggregated to provide a market-by-market consensus overview. The next edition of this survey is due to be released at the start of March.

The Property Council of Australia’s Office Market Report and Office Occupancy Survey are nation-leading, in depth analysis of Australia’s office vacancy and occupancy levels. The Property Council of Australia is actively using these data sources to advise and inform the Victorian Government’s return to office roadmap.

With respect, this is an office apocalypse, chart from the AFR:

A few points:

- we can expect office investment to collapse along with rents:

- prices are also going to fall:

Where are these losses going to end up? First of all: AREITS. Avoid!

Australian banks are notoriously parsimonious with commercial development since the 1990s bust so any losses there should be manageable. The last cycle saw a lot of foreign capital drive office development so that’s where loan losses will hit.

When might it turn? Vaccines will help. But WFH is a structural shift so the rebound will be muted and rents and capital values will remain under pressure for some time to come.