The Australian dollar soared on Icarus wings last night. The driver was a renewed swoon in the US dollar as consolidation of the recent move higher in yields took over. I do not think that the trend has changed. To the charts!

DXY was down, down as EUR jumped on ECB waffling:

US dollar swoons

The Australian dollar soared:

Advertisement

On wings of wax

The oil bid returned:

More inflation panic cometh

Base metals finally dead catted:

That screcching sound

Big miners likewise:

Advertisement

Sell the rally?

EM stocks and junk gapped to heaven:

Emerging from the gloom

The Treasury curve steepened but nobody cared:

Infaltion schminflation

Stocks to the moon, led by the bargain basement Nasdaq!

Advertisement

The bear market rally roars on

I remain of the view that we have slipped into a phase change market in which inflation worries will continue to lift US yields, inflation and growth and those three advantages will drive an ongoing rise in DXY.

That said, nothing happens all at once and the evening’s events drove consolidation in that trend. The ECB followed the RBA’s lead, via Westpac:

Advertisement

The ECB left its key policy rates unchanged, as was widely expected. However, in a clear signal to markets that the ECB will address undue increases in yields and widening of spreads, it said that it would purchase bonds “at a significantly higher pace” in the next quarter. At the same time, the ECB repeated that the PEPP programme may not be used in full.

But that was a sell-the-fact event. More importantly, the market also ignored this, at Barron’s:

Senators are already working on President Joe Biden’s next legislative priority, a major transportation package at the heart of Biden’s “Build Back Better” plan, with the aim of getting the entire bill passed with Republican support by the end of September.

Sen. Tom Carper (D., Del.), who heads the Environment and Public Works panel, told reporters Wednesday that he is confident Democrats can get at least 10 Republicans to sign on to the proposal, which would enable them to pass it without resorting to budget reconciliation.

The bill, which is expected to cost at least $2 trillion, would modernize the nation’s infrastructure while creating millions of manufacturing and clean energy jobs to “rebuild our roads, our bridges, our ports, and to make them more climate resilient,” Biden said shortly after taking office in January.

Although infrastructure reform has bipartisan support, the specifics are up for debate. Take clean energy, which Sen. Shelley Moore Capito (R. W.Va.) said Wednesday “isn’t just wind and solar power,” adding that it includes everything from low-carbon natural gas to “electricity generated conventionally from fuels like coal with innovative technologies.”

Advertisement

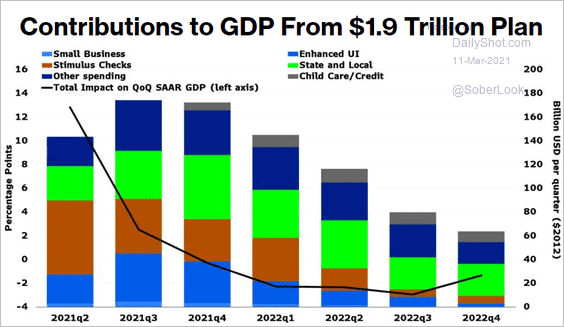

The Dems are aiming for money to flow from Q3. With good reason:

Fiscal cliff dead ahead!

Whether it gets passed by bipartisanship of budget reconciliation who cares. It’s going to get passed and add 2%+ per annum to US GDP from 2022-26.

Advertisement

That is a lot of potatoes to lift average US growth to 4%+ for the next four years, a real reason for the market to worry about inflation:

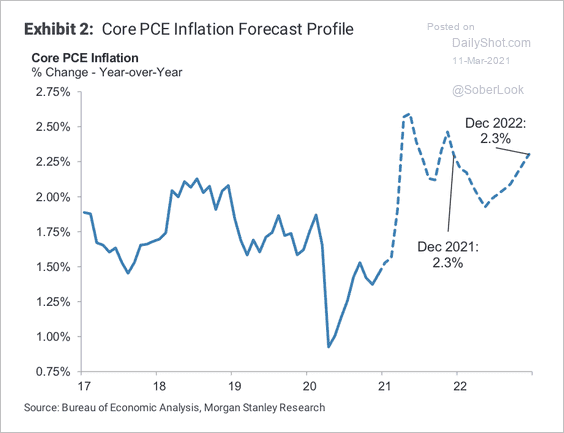

US inflation mwahahha

I expect another round of inflation panic to set as the real numbers arrive and the Biden agenda gathers momentum. The US ten year at 2-2.5% is where I’m looking next. That means another leg down in tech, EMs and the AUD once we get through this consolidation.

Advertisement

For me, it’s still probably NOT enough to generate an inflationary wage push cycle to really alarm. The more that the US leads global growth, the more tightening China will do. Europe is a paralysed mess as usual. So, after the initial commodity price excitement, I still expect dirt will fall as US growth, inflation and yield advantages lead DXY higher.

For Australia, it shapes as a decent few years as commodity prices remain at OK levels with the Australian dollar materially below where it might normally be. Materially lower than today. This will boost national income.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.