Last week, Liberal MP Tim Wilson came under fire after it was revealed that he and his partner owned five residential properties and stand to gain financially from Wilson’s proposal to allow first home buyers (FHBs) to use their superannuation savings to purchase a home.

Wilson hit back at his critics over the weekend:

“They are deluded in thinking their intimidatory tactics will stop us shining bright lights in dark places, or that we will back down from fighting for home ownership by getting life’s financial priorities right: home first, super second.”

Regular readers will know that I am an outspoken critic of Australia’s compulsory superannuation system, despite this site offering the MB Super Fund and, hence, benefitting financially from policies that force Australians to put money into super.

My skepticism is centered around three main concerns:

- Compulsory superannuation reduces take-home wages;

- Superannuation concessions are poorly targeted toward higher income earners. Therefore, superannuation’s cost to the federal budget is greater than future savings from lower Aged Pension outlays; and

- The inequitable distribution of superannuation concessions increases inequality.

That said, I also do not support allowing FHBs to raid their superannuation savings to purchase a home. While this policy may benefit some individual FHBs, it would push up demand and be inflationary to property prices overall, thereby eroding affordability.

Thus, Tim Wilson’s policy would quickly be capitalised into higher home prices, with the end result being no affordability gain and lower retirement savings. This explains why Tim Wilson and his partner, who own five properties, stand to gain large wealth increases if his policy goes ahead.

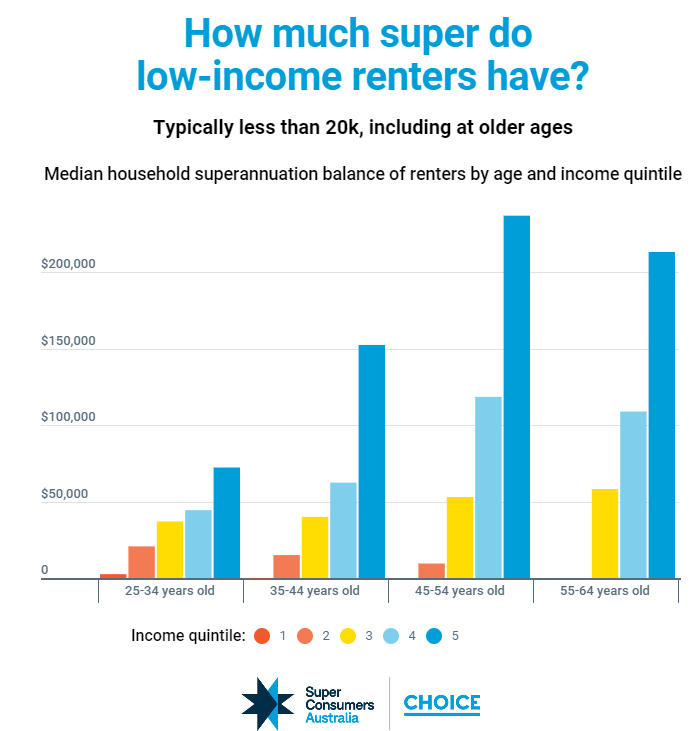

New research from Choice further highlights why Tim Wilson’s policy would not help would-be FHBs.

Young low-income renters have minimal superannuation savings.

As shown in the above chart, young lower income renters have negligible superannuation savings. Thus, Tim Wilson’s policy could actually impede this cohort’s ability to buy a home, according to Kate Colvin, spokesperson for national housing campaign Everybody’s Home:

“Paradoxically, allowing people to use their super for housing would increase the purchasing power of people who have a high income, and so have a relatively high super balance, exactly the group who are already most able to buy.

“Giving this group access to faster capital will push up prices across the board, making it harder for the people who were already struggling to get a foothold in the market.”

The last thing this country needs is to pour superannuation fuel on the housing bonfire, in the process making affordability worse and reducing retirement outcomes.

Let’s instead target the three fundamental flaws in superannuation listed above by: 1) abandoning the scheduled rise in the superannuation guarantee to 12%; and 2) reforming the concession system to make it far more progressive.