Stock markets remain in hesitation and consolidation mode as we head into the all important US inflation report with overnight sentiment still mixed. Bond yields pulled back while the USD found some lost ground with gold still unable to clear the $1900USD per ounce level. European data was a little softer than expected, particularly German industrial production which kept European bourses steady for the most post. Commodity prices were truly mixed with oil spiking again alongside iron ore.

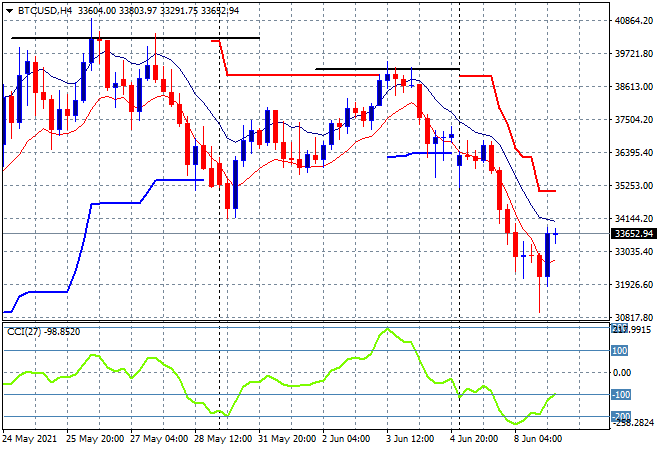

Bitcoin fell out of bed all day yesterday and almost cracked through the $30K level before a “everything is fine” 10% rally overnight taking it back to the $34K level level this morning. Price is poised for a breakout here above the high moving average for a classic swing play but its a low probability move:

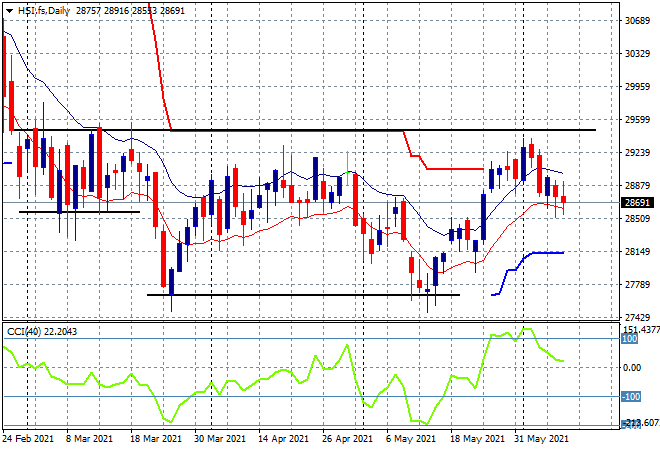

Looking at share markets in Asia from yesterday’s session, where the Shanghai Composite fell over 0.5% to close at 3580 points, still unable to climb back above the 3600 point level while the Hang Seng Index was steady after its previous selloff, down a handful of points to 28781. Price action is again failing to re-engage to the upside after the recent breakout with the inability to decisively clear resistance at the 29000 point level keeping this market contained and possibly in decline:

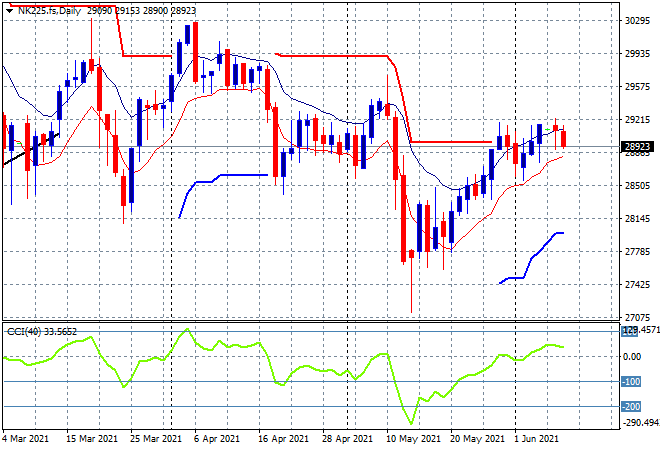

Japanese stocks continued to struggle with a stronger Yen with the Nikkei 225 taking back the previous meagre gains to close 0.1% lower at 28963 points. Daily futures are pointing to more downside on the open today as recent sessions show a bunch up around the 29100 point level but not through it even as the moving average band moves higher, momentum is not yet in proper overbought mode to indicate a sustainable trend:

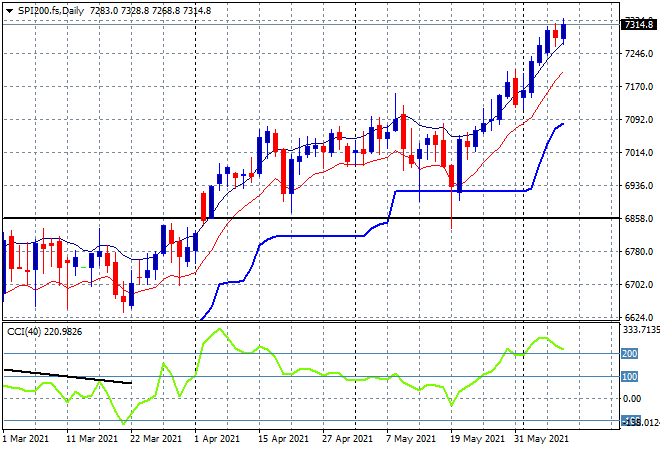

The ASX200 was the only market to make headway, but only just, closing just 10 points higher at 7291 points. SPI futures are again up another 10 points so although we should see more upside here, momentum remains extremely overbought with the potential for a mild pullback here. Watch the high moving average for any signs of an inversion:

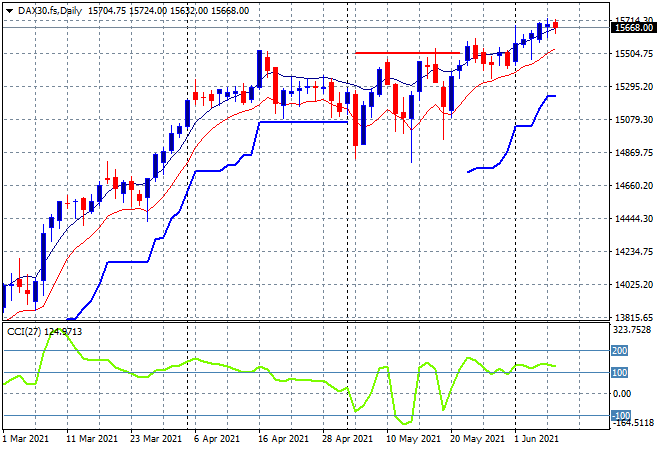

European markets continue to flit around with more regional divergences as the FTSE lifted 0.25% while the German DAX pulled back once more, this time down 0.2% to finish at 15640 points. This daily chart is still looking promising with momentum nicely overbought and price action continuing to track higher, but its not yet like the May run up so I’m keeping an uncle point clearly at the low moving average level:

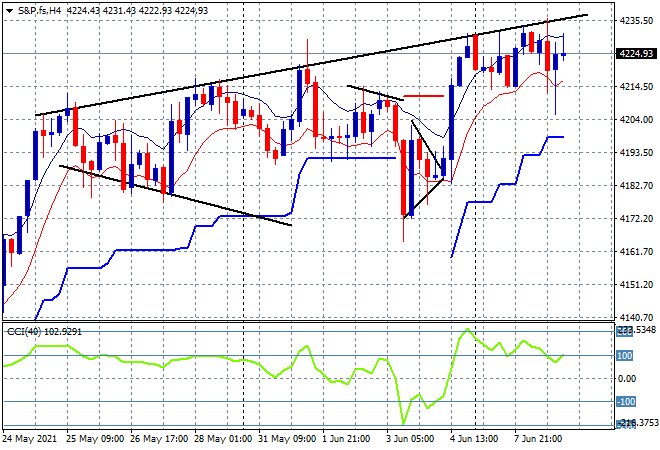

Wall Street was unsettled with headline DOW putting in a scratch session with a minor loss, the tech heavy NASDAQ actually gaining 0.3% while S&P500 again tread water, staying bang on 4227 points, still shy of its recent record high. Price action on the daily and four hourly charts is trying to clear to the upside here but the lack of a proper positive close and another record high is keeping risk spirits at bay:

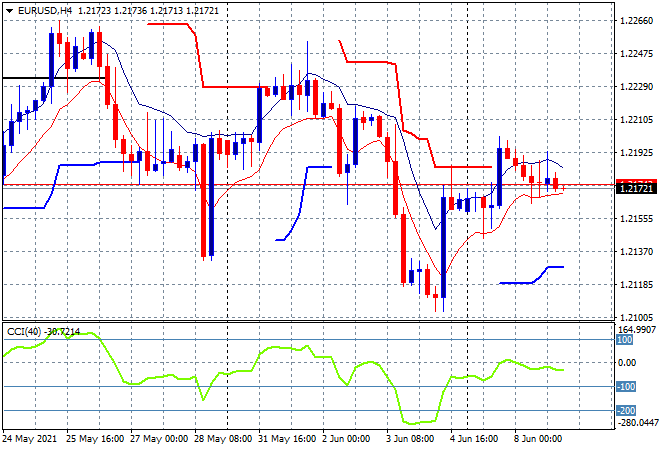

Currency markets are also in consolidation zone following the NFP print from Friday with Euro settling in to just below the 1.22 handle last night, basically unchanged from the ZEW survey and EZ GDP estimates. As I said yesterday while the bounce on Friday night was relatively large, it still only takes back to last week’s starting point and still doesn’t put it out of danger with some considerable resistance overhead at the 1.22 level and at the previous weekly highs at the 1.2270 to overcome:

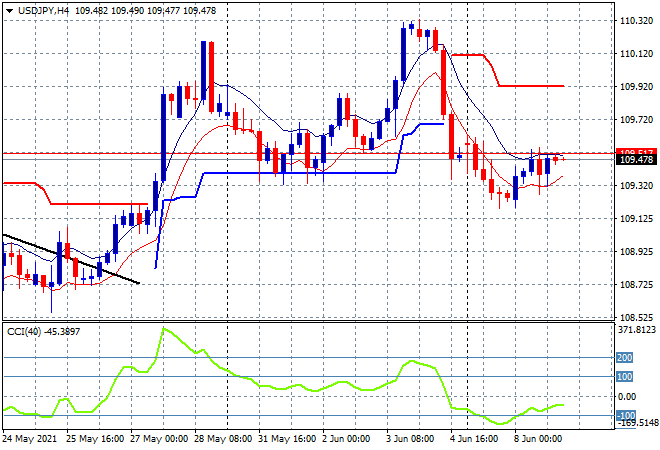

The USDJPY pair remains composed as well with some tight trading around the moving average band and not much else last night, settling at the mid 109 level this morning. This price action created a new weekly low below last week’s support at the 109.40 level and although price is slowly building back up above it again, I’m still watching for any flip below the recent very tight four hourly sessions:

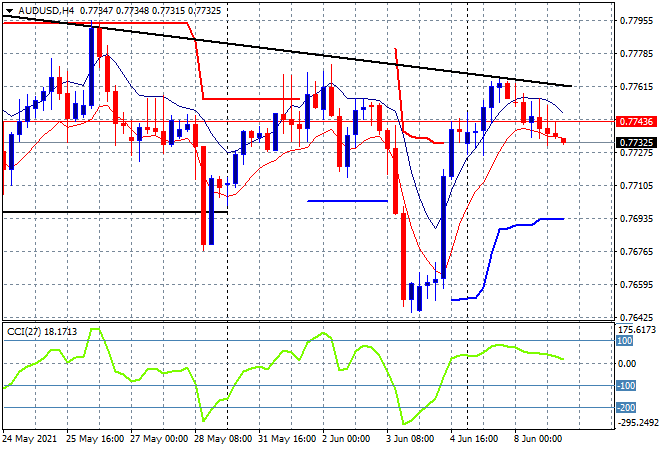

The Australian dollar is on deflation ride yet again, pushing back towards the 77 handle as it was unable to clear the 77.70 level or threaten the dominant downtrend in play (upper sloping black line). Momentum is not yet overbought on the four hourly chart, and combined with the clear deceleration and waning intrasession momentum, we could see a reversion here in the short term back to the 77 handle proper:

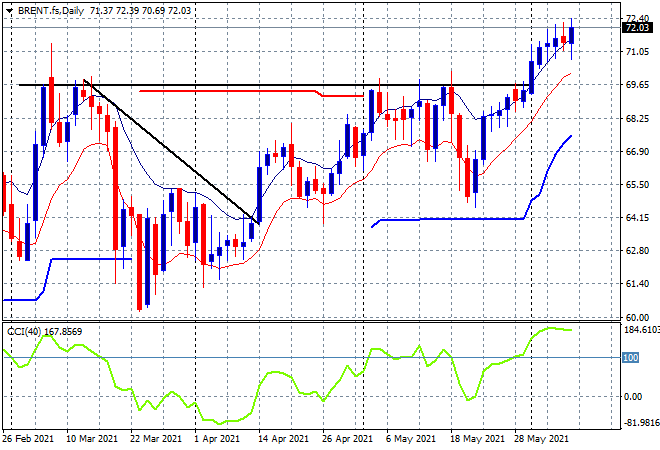

Oil prices got out of their temporary funk overnight with the Brent crude marker pushed up 2% to be just above the $72USD per barrel level. There is still the potential run up to the 2018 high at $83 or so but I’m cautious here despite some good momentum:

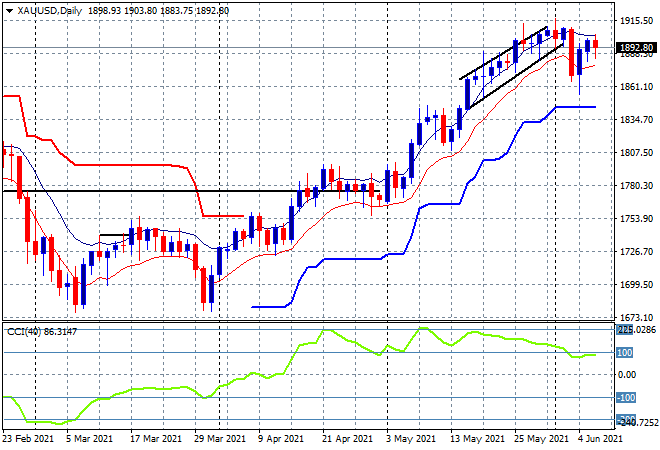

Gold is still fighting back following the NFP print but despite a try mid session failed to get back above $1900 level. As I mentioned yesterday, price didn’t go near trailing daily ATR support at the $1850 level but it still requires another solid session in the short term of the anticipated run up to the former highs may prove too elusive before the Fed actually does Taper:

Glossary of Acronyms and Technical Analysis Terms:

ATR: Average True Range – measures the degree of price volatility averaged over a time period

ATR Support/Resistance: a ratcheting mechanism that follows price below/above a trend, that if breached shows above average volatility

CCI: Commodity Channel Index: a momentum reading that calculates current price away from the statistical mean or “typical” price to indicate overbought (far above the mean) or oversold (far below the mean)

Low/High Moving Average: rolling mean of prices in this case, the low and high for the day/hour which creates a band around the actual price movement

FOMC: Federal Open Market Committee, monthly meeting of Federal Reserve regarding monetary policy (setting interest rates)

DOE: US Department of Energy

Uncle Point: or stop loss point, a level at which you’ve clearly been wrong on your position, so cry uncle and get out!