Numera captures the prevailing view on Wall Street about the future of bond yields:

• Recovery on track: Strong employment and retail sales figures, alongside falling public health risks, reinforce the view that the US recovery remains on track. Equity investments should yield positive returns in 2022, but high valuations and a likely increase in longterm yields (see below) cap the magnitude of future gains.

• Inflation and yields: High inflation readings are raising fears over Fed tightening. We expect consumer inflation to exceed 4% next year, increasing the likelihood of higher longterm yields. Our modeling work now points to a 50+ bps increase in 10Y Treasuries over the next 12M, reducing the relative appeal of growth stocks.

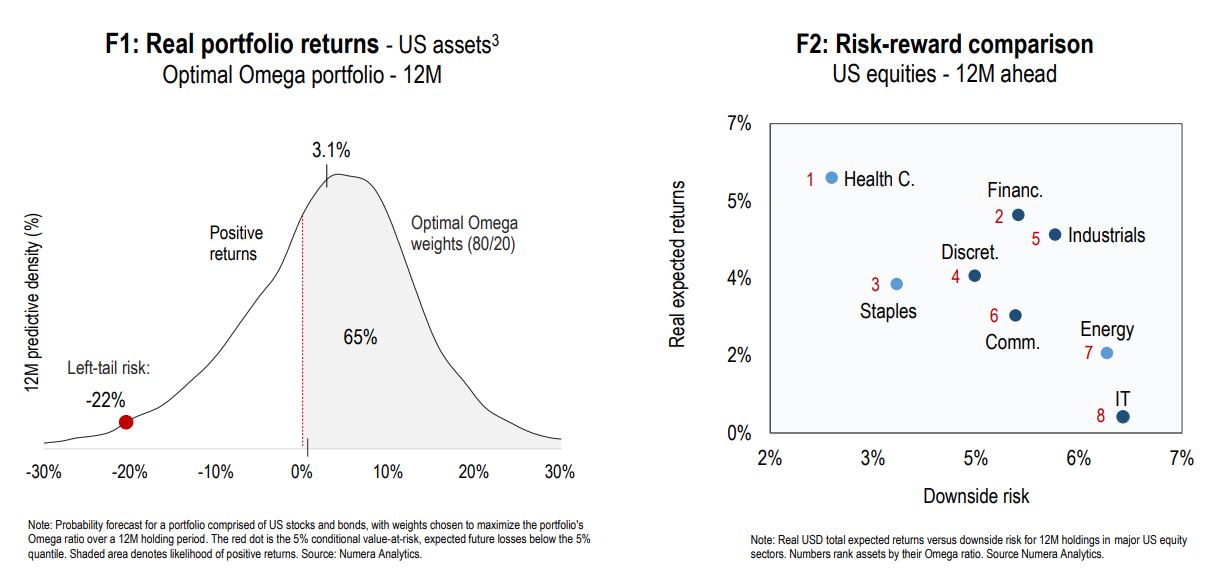

• Asset allocation: A likely transition from ‘reflation’ to ‘overheating’ continues to support the relative appeal of equity over FICC investments (F1). In managing equity risk, in turn, we suggest favouring corporate bonds and TIPS over sovereign nominal bonds, the

macro hedge that is most exposed to elevated inflation risk.

It appears that the inflation panic has gotten the better of the Fed now, as it did the RBA a few weeks ago. Increasingly, the taper is likely to accelerate and rate hikes begin mid-2022.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.