CoreLogic’s head of research, Eliza Owen, has published interesting research comparing the growth of Australian property prices against wages:

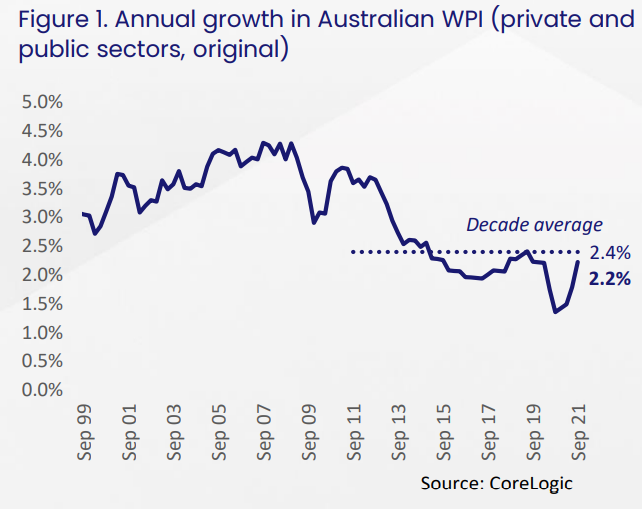

This month, the ABS posted a 2.2% annual increase in the Australian wage price index (WPI)… The 2.2% uplift represents wages growth getting back to pre-pandemic levels, and is just shy of the decade average growth of 2.4%…

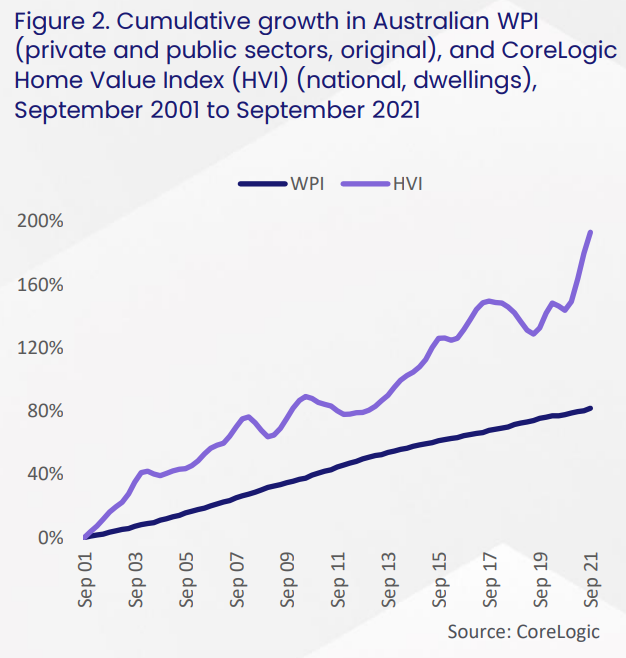

While wages increased 81.7% in the past 20 years, Australian home values have grown 193.1% (figure 2)…

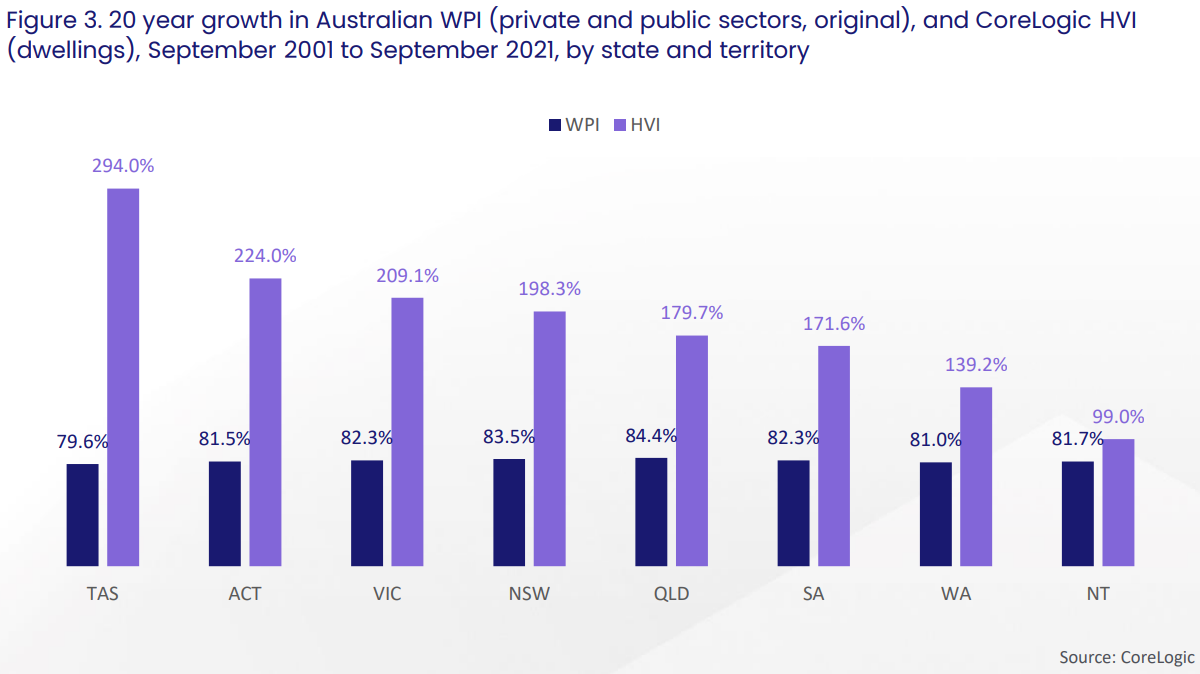

The difference in growth across wages and house prices is presented by state in figure 3…

Eliza Owen went on to explain several channels through which wage growth impacts the property market:

Wage growth impacts one’s ability to save up a housing deposit;

Wage growth impacts mortgage serviceability; and

Wage growth impacts inflation and mortgage rates.

Advertisement

It may sound controversial and somewhat counter-intuitive, but higher wage growth could be the harbinger of the next major housing downturn.

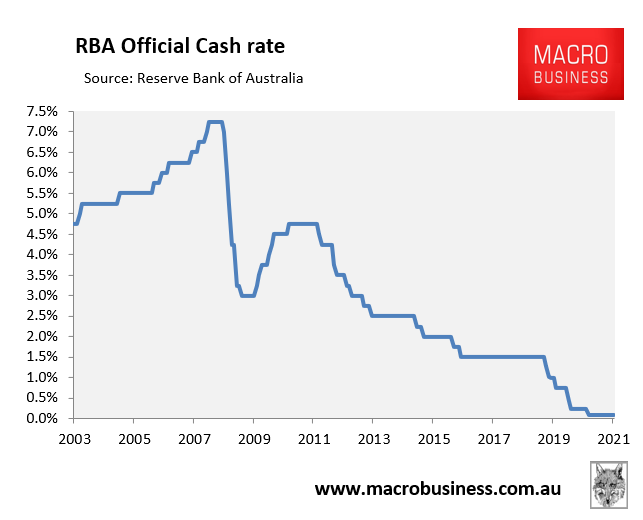

The record low wage growth experienced over the prior decade was the primary cause of persistent low inflation and the sharp fall in the RBA cash rate:

Advertisement

This low wage growth, in turn, was driven by persistent ‘slack’ in the Australian labour market caused primarily by the strong immigration program, which added 180,000-plus workers to the Australian economy every year.

Thus, if wage growth was to accelerate from here on the back of lower immigration and a tightening labour market, then this would be met with higher interest rates, which would cause property prices to fall.

Indeed, the RBA has stated repeatedly that it needs to see wage growth with a ‘3’ in front of it for inflation to hit its target.

Wage growth is now central to RBA policy. The Bank says it will not tighten until actual inflation is sustainably within its 2-3% target range, and that will require materially higher wage growth than current levels…

The key to the RBA is domestic wage growth. The tricky point is that wage growth is likely to be a function of how reopening the international border affects labour supply. The longer supply is crimped, the more likely it is the wage growth may increase to the point where the RBA will need to tighten before 2024. But if migration flows revert to pre-pandemic levels, then it’s likely that wage growth reverts to pre-pandemic levels. If that happens the RBA may be able to go another 11 years without tightening.

The Australian economy has been exceptionally good at growing at a reasonable pace without generating excessive wage costs. This is partly a function of our ability to continuously import human capital through an ambitious skilled migration program…

A wave of students and skilled migrants would alleviate upward pressure on wage costs and inflation, and possibly allow the RBA to defer increases to its target cash rate into 2023. A great deal therefore hinges on labour supply, and the current lack thereof…

If this offshore labour supply returns, the skills shortages that many firms have been complaining about should dissipate.

Both echo RBA Governor Phil Lowe, who recently acknowledged that high immigration pre-COVID was used to hold down wages.

The upshot is that maintaining the Australian property ‘bubble’ hinges on keeping interest rates low, which ergo hinges on suppressing wages through high immigration.

Advertisement

Perverse isn’t it? Crush wage growth via immigration to ensure lower interest rates and higher house prices: win-win for the elites.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.