The US dollar was weak on Friday night as EUR bounced:

But Australian dollar was weak anyway:

Oil is firming as OMICRON hints at the end of COVID19:

Advertisement

Base metals were firm over Xmas but not copper:

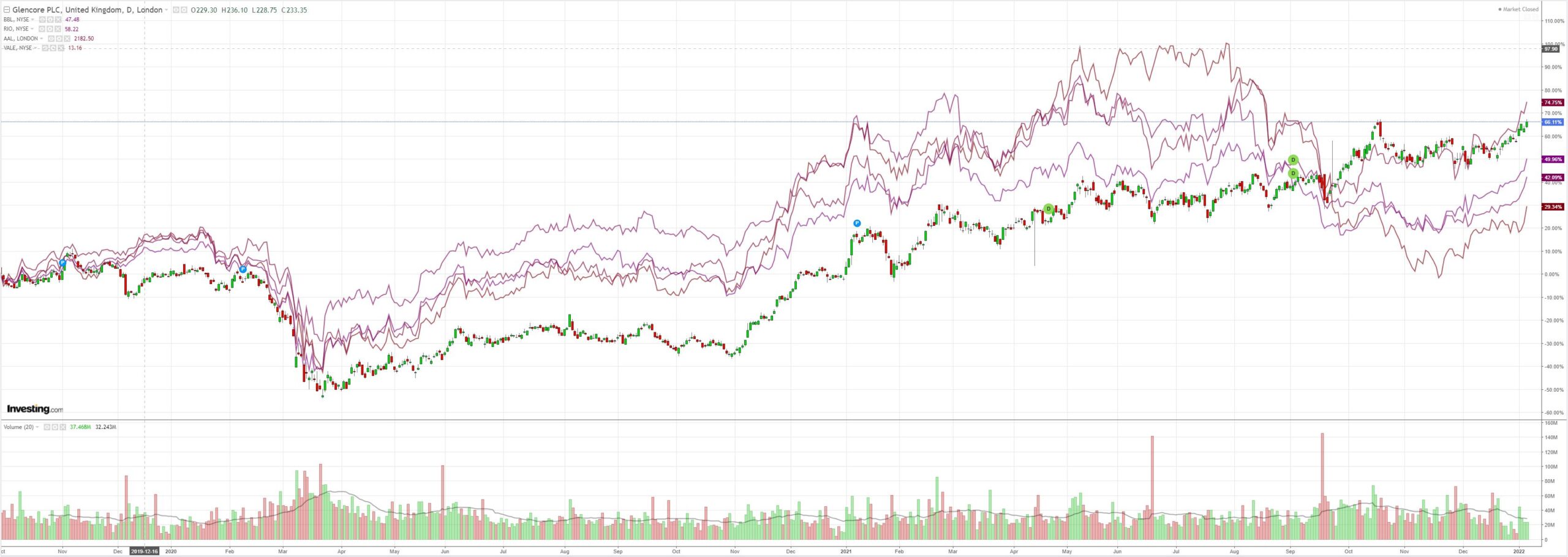

Big miners are getting very excited for no reason:

Advertisement

As EM stocks go the other way:

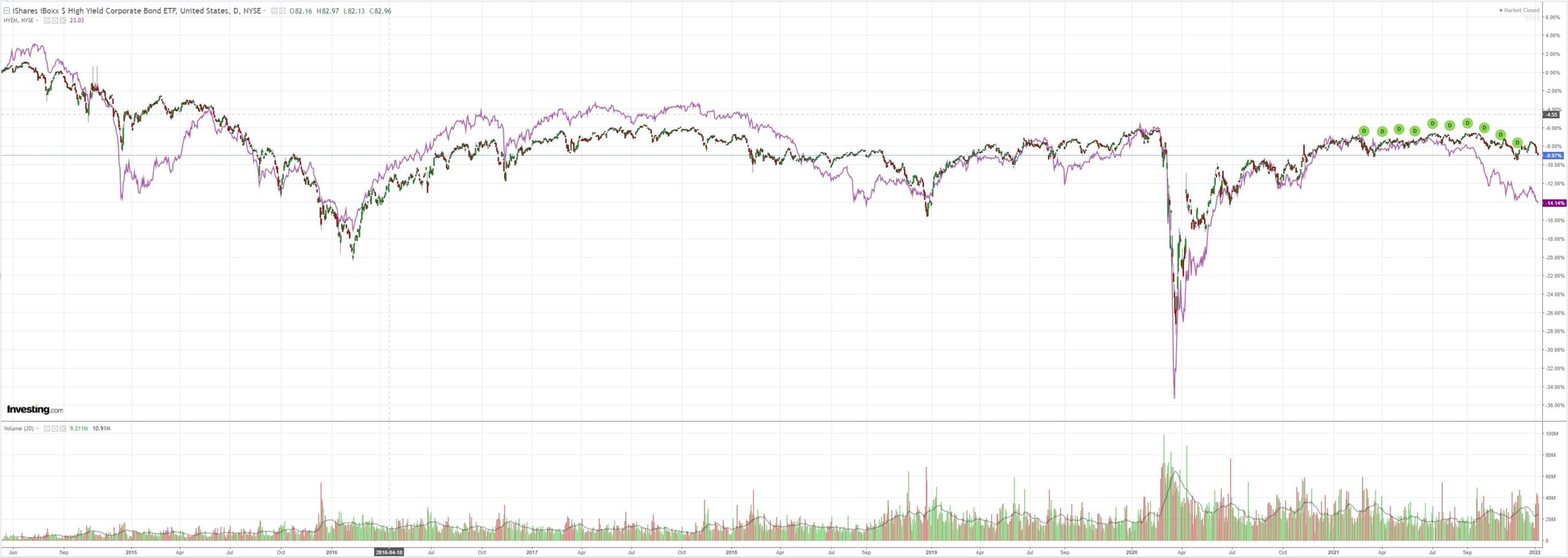

Trailing EM junk which is pretty bearish for all assets:

Advertisement

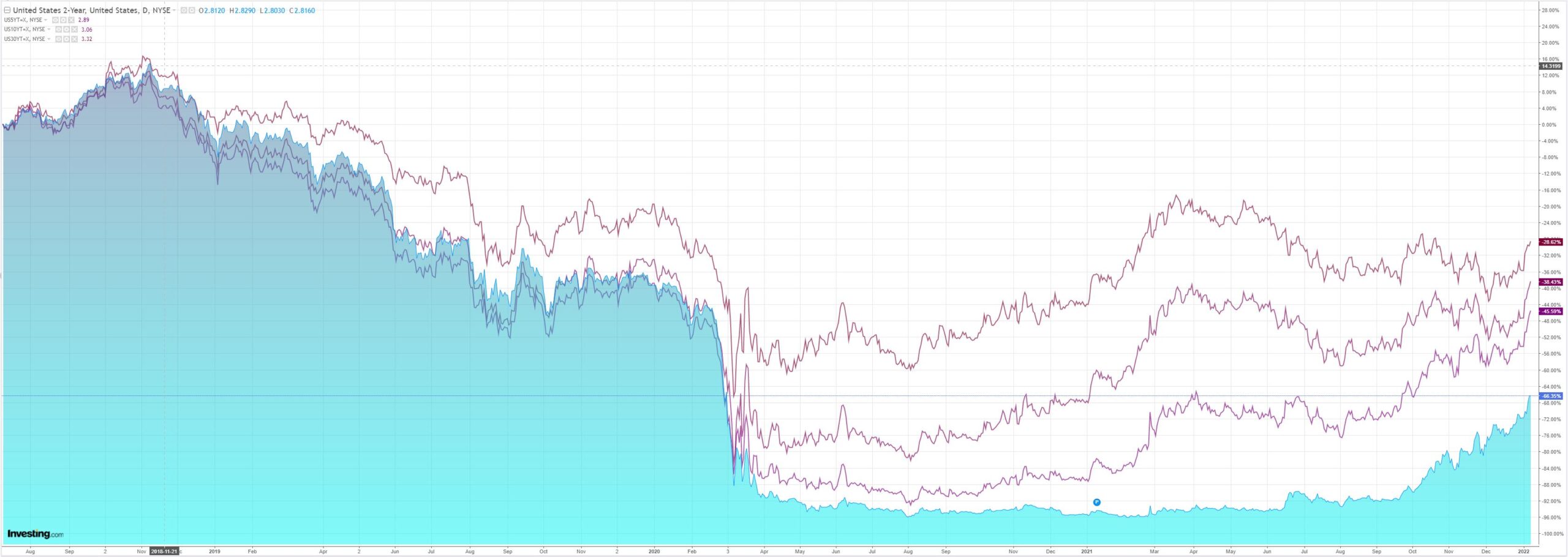

Yields jumped over Xmas as OMICRON delivers a little more inflation. The curve steepened less:

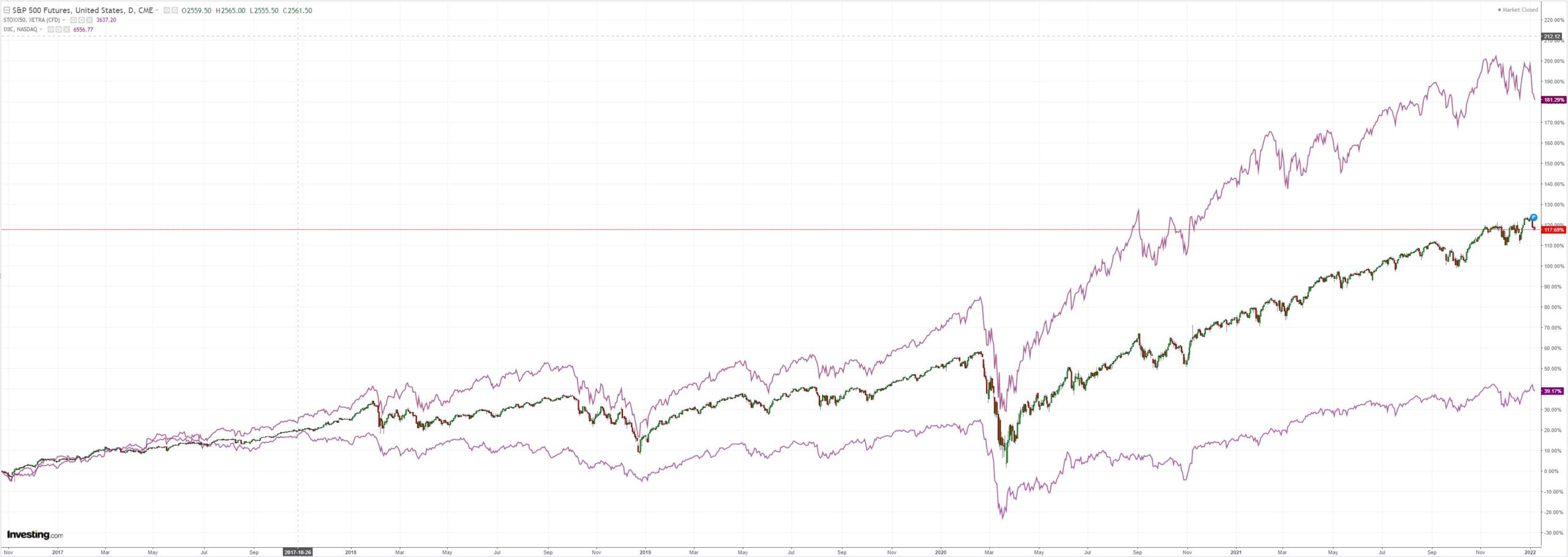

Which hit Growth stocks:

Advertisement

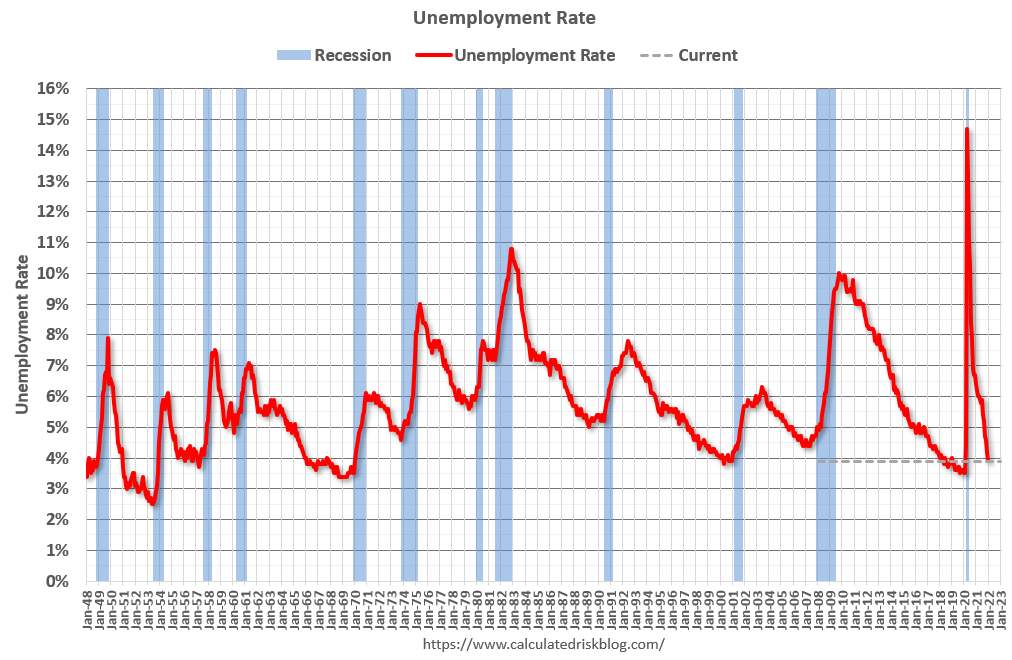

US jobs were softer than expected but still decent:

Total nonfarm payroll employment rose by 199,000 in December, and the unemployment rate declined to 3.9 percent, the U.S. Bureau of Labor Statistics reported today. Employment continued to trend up in leisure and hospitality, in professional and business services, in manufacturing, in construction, and in transportation and warehousing.

…The change in total nonfarm payroll employment for October was revised up by 102,000, from +546,000 to +648,000, and the change for November was revised up by 39,000, from +210,000 to +249,000. With these revisions, employment in October and November combined is 141,000 higher than previously reported.

Over Xmas, markets have rightly moved to price a little more inflation and therefore a little more Fed tightening thanks to OMICRON disruptions. However, I still think that it won’t be long before the US curve starts to flatten again.

The main reason is that over Xmas the US dalliance with MMT also died. The end of Build Back Better shifts the growth projection dial back towards secular stagnation pretty quickly as the Fed tightens through H1.

Advertisement

This is a great disappointment for America. Virus inflation panic has aborted what was an excellent fiscal reform package that would have guaranteed the US a productivity and growth advantage for much of the cycle ahead.

Now, as the coming post-COVID global deflation transpires, Fed tightening will be short-circuited before very long in some kind of equities correction and we’ll be back to QE with a bullet, with all of its problems.

How does FX fit this picture? I remain bullish DXY for now and into the Fed tightening but that is the end of it. Afterward, the loss of BBB throws open the distinct possibility that looming Chinese stimulus (there is none of consequence yet) will once more drag it into the growth leadership position as we enter H2’22 or 2023.

Advertisement

Goldman sums it pretty well:

USD: Favor exposure to US/Europe growth and higher bond yields; turn cautious Asia and tech-sensitive FX. It’s been a choppy start to the year for the broad Dollar—with FX markets instead dominated by sizable moves in a number of non-USD crosses—due to a complex set of macroeconomic drivers. We see three key macro trends currently affecting the FX outlook: (i) major micron outbreaks in Western economies, which will damage near-term growth but also accelerate progress toward the endemic phase of the medical crisis; (ii) likely outbreaks in Asia in the coming weeks, which could have larger effects on growth due to comparatively low immunity rates in the region and, in China specifically, the government’s zero-tolerance covid policy; and (iii) increasingly hawkish signals from developed market central banks, which is putting upward pressure on bond yields and seemingly causing a growth-to-value rotation within equities. Broadly speaking, we think markets should take a “glass half full” view of the medical backdrop. While ongoing outbreaks will inflict economic and human cost, omicron’s lower severity and the rise in effective immunity from additional infections should improve the distribution of possible growth outcomes beyond the near-term. As a result, we favor longs in currencies positively exposed to North American and Western European growth, as well as those with relatively hawkish central banks (e.g. CAD). At the same time, we would avoid currencies that could be harmed by higher global bond yields, downgrades to Asia growth expectations, and/or a continuation of growth/tech underperformance in stocks (e.g. JPY, AUD, MYR, KRW, and TWD). We therefore issue a new recommendation to go long CAD vs JPY and AUD (in equal weights) to express these views (more details below).

I am still bearish AUD as well. But it is a less secular view than it was before Xmas. By H2, the still crashed Chinese property market is going to need stimulus proper or Beijing will miss its growth targets badly as the world slows. If this happens just as US growth fades into its mid-cycle slump then the chances of a bottom and strong cyclical rebound for AUD are obvious.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.