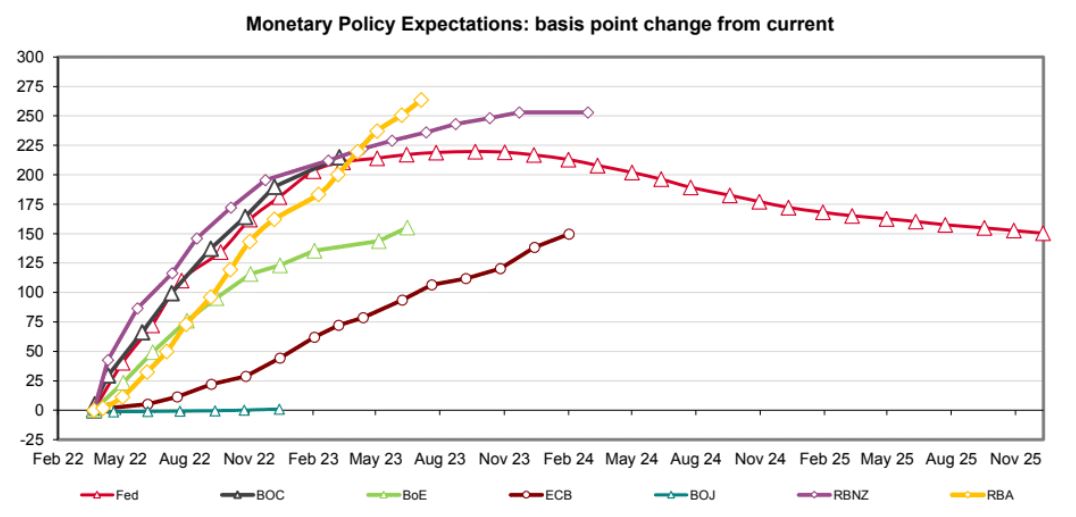

With each passing week, it gets more outlandish. Markets are now pricing nearly eleven straight rate hikes by July 2023. Assuming the tightening begins in June, that’ll be a hike every meeting for 13 months or a whole swag of 50bps hikes. Via Westpac:

Here is what this will do to Aussie households:

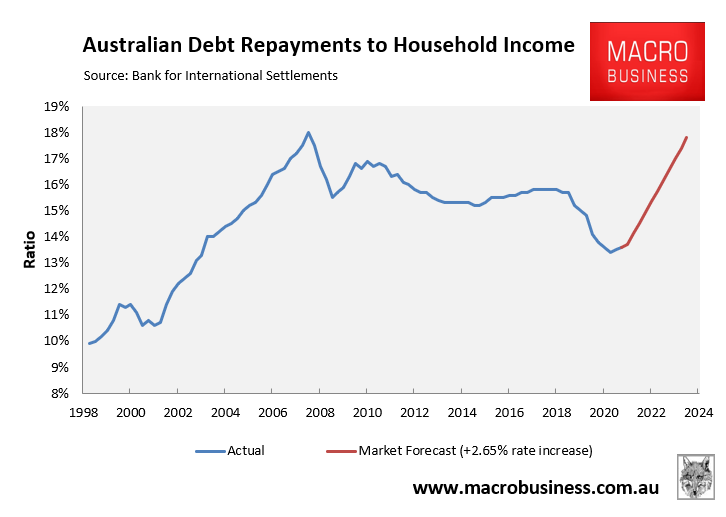

- If OCR rose by 2.65%, average monthly mortgage repayments would rise by 36%.

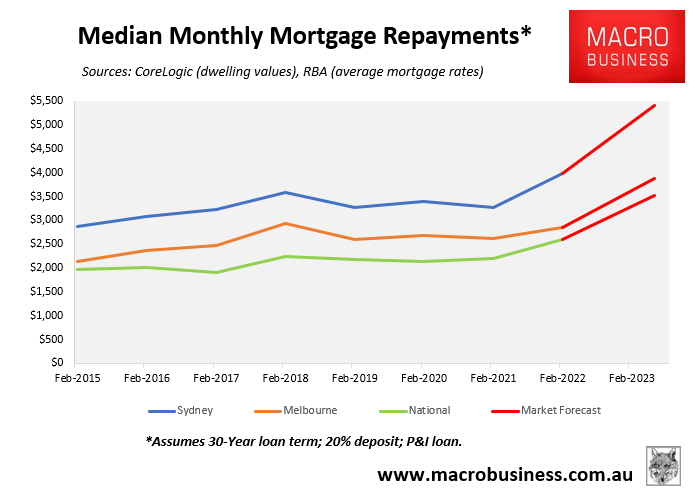

- $930 monthly increase in mortgage repayments nationally (assuming median priced home, 30-year P&I mortgage and 20% deposit). $1,426 increase for Sydney and $1,022 for Melbourne.

This is a far more powerful imminent tightening cycle than Australia experienced after the GFC when the RBA explicitly set about “making room” for an expansion of Australian mining as the terms of trade hit record highs.

Commodity prices are even higher now so on the surface markets are re-running the same playbook.

The problem is that the booming commodity prices this time are not going to be followed by an investment surge to drive growth. The major commodities are all inhibited:

- iron ore is in a structural glut;

- the two coals are buggered by ESG;

- LNG is largely tapped out given the Australian market share is already so high.

As well, high LNG prices add nothing to the economy, the budget is in deep deficit limiting any fiscal boost and share markets are falling.

In short, if the RBA were to follow market directions this time, all it will be doing is making room for a depression as house prices halve around the country.

But, as JM Keynes once said, markets stay irrational longer than you can stay solvent.