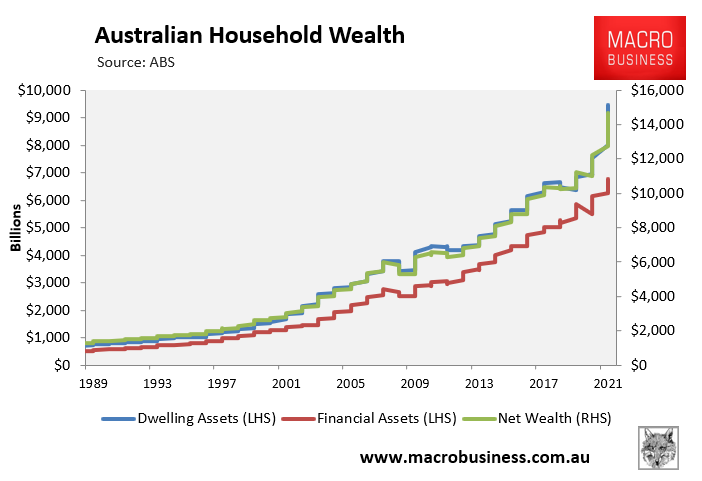

The Australian Bureau of Statistics (ABS) yesterday released household wealth data for the December quarter of 2021, which revealed that total household wealth increased by 4.5% ($628 billion) over the December quarter 2021 reaching a record $14.7 trillion:

Record household wealth

Total dwelling assets surged by 5.5% ($490 billion) over the quarter to a record high $9.5 trillion, whereas total financial assets rose 2.7% to a record high $6.8 trillion.

As explained by Head of Finance and Wealth at the ABS, Katherine Keenan:

“Residential property prices continued to drive increases in household wealth, contributing 3.5 percentage points to the quarterly growth in household wealth. Prices increased 4.7 per cent during the quarter, reflecting record low interest rates, labour market recovery, and strong demand for housing.”

Ms Keenan said increases in superannuation balances, and currency and deposits, contributed a further 0.7 and 0.3 percentage points respectively. Offsetting these was an increase in household loans which detracted 0.4 percentage points from growth.

“The contribution of superannuation to household wealth reflected the recovery in the labour market, as well as the increase of the superannuation guarantee from 9.5 to 10 per cent from 1 July 2021. Household deposits continued to grow, although at a slower rate compared to September quarter, as household spending increased as states emerged from COVID-19 lockdowns.“

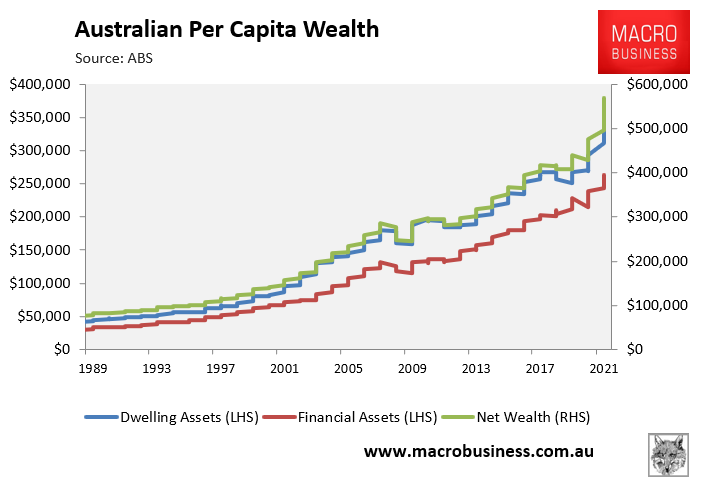

Per capita household wealth also surged by 4.4% over the quarter to a record high $569,100, with per capita dwelling assets rising 5.4% to $366,800 and per capita financial assets rising 2.6% to $263,200:

The average Australian is worth $569,100.

My long held view is that having so much of our wealth locked up in housing is useless. Every Australian needs somewhere to live and higher home values serve little purpose to the vast majority of owner-occupiers, who typically must sell and buy into the same market.

Expensive housing also punishes those who have recently entered, or are yet to enter, the housing market. These people are required to either take-out mega-mortgages and have a life of debt slavery, or miss-out altogether.

Would Australians really be worse-off if the median dwelling price was $370,000 instead of $740,000, mortgage debt was 70% of disposable incomes instead of 140%, and the banking sector was smaller and less profitable?

The answer is clearly no. Lower debt loads would make Australian households better-off, whereas the broader economy would benefit from the productivity-boosting effects of lower land prices, increased business lending (investment), and a more balanced economy.