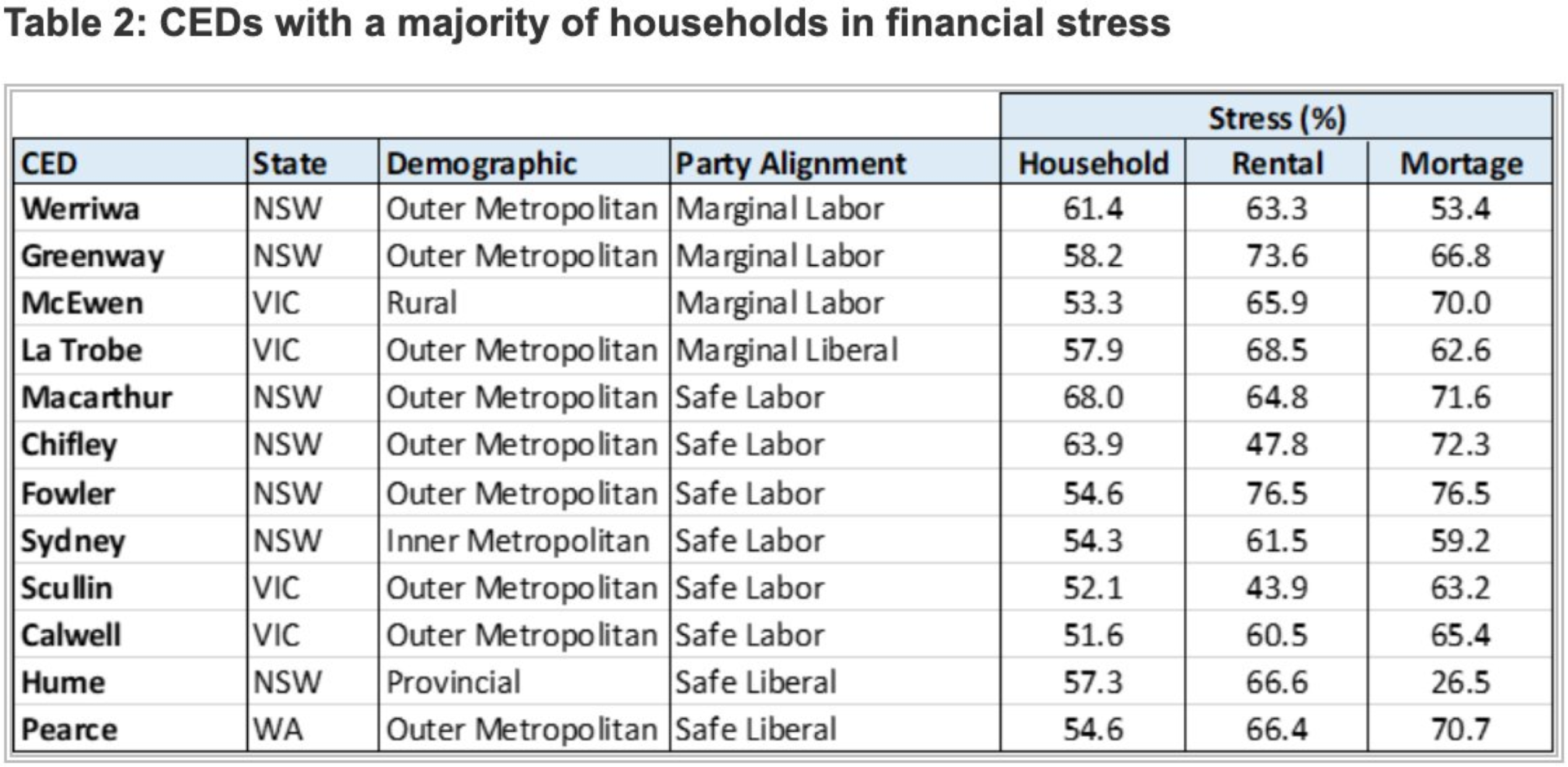

New data from researchers at the University of New South Wales (UNSW) shows that out of the 12 electorates where the majority of residents are experiencing severe financial stress, nine were in the outer suburbs of Sydney and Melbourne:

Severe mortgage stress in Sydney’s and Melbourne’s outer suburbs.

According to Professor Hal Pawson from UNSW, “It’s not strictly speaking mortgage stress. It’s people who are in financial stress who also have a mortgage”.

Many of these households would have purchased near the top of the market during the pandemic at mortgage rates below 2.5%. Accordingly, they are facing a “huge cliff'” in coming years as their fixed-rate loans expire and they are hit with higher interest rates:

“There’s going to potentially be a huge cliff in two or three years’ time when their fixed-rate loan runs out because they’ll have to refinance,” Pawson said.

For those on an average mortgage of $600,000, adding three percentage points to the borrowing costs could swell repayments by $1,500 a month or more. “That’s going to be a lot for any household to swallow.”

Rate City’s Sally Tindall agrees:

There’s going to be some households that really have to take a long hard look at their budgets, and potentially make hefty cuts in numerous places to just keep their heads above water and their mortgage repayments up.

Anyone who bought recently and potentially overstretched themselves to get into an overheated property market, they will feel the heat of these rate hikes, that’s for certain.

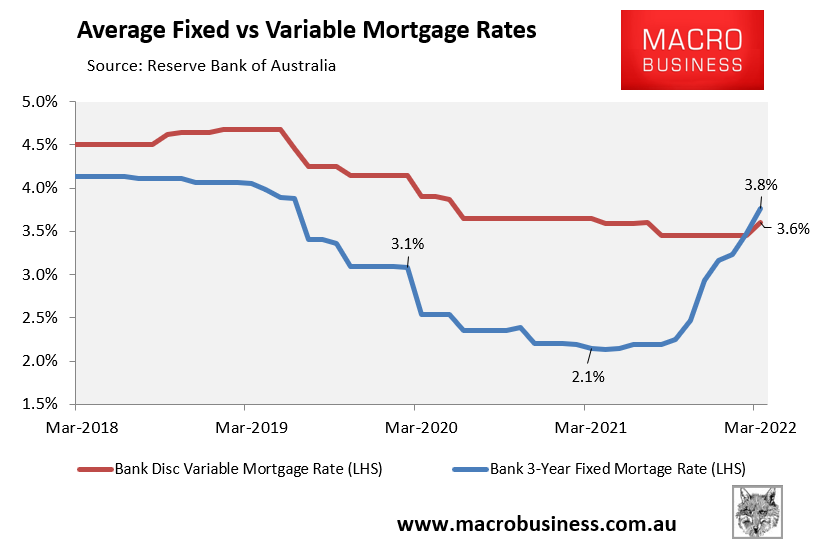

Already, fixed mortgage rates have risen sharply from their pandemic lows, whereas variable rates have also ticked higher:

Australian mortgage rates are already rising.

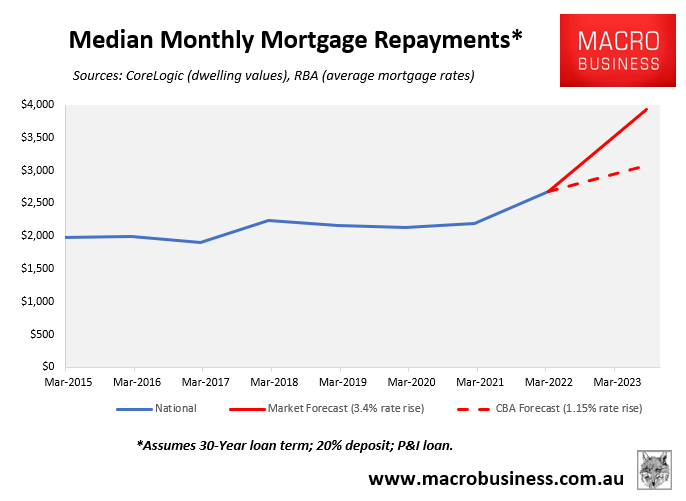

Australia’s bank economists expect the RBA to lift the Official Cash Rate by between 1.15 per cent (CBA) and 3.0 per cent (ANZ), whereas the futures market is tipping a jumbo rise in the OCR of 3.4% by August 2023.

The next chart shows how monthly mortgage repayments on the median priced Australian home would be impacted if rates rose by the low-end (CBA’s) and high-end (futures market’s) forecasts, assuming a 30-year principal and interest mortgage and a 20 per cent deposit:

Median monthly mortgage repayments are set to soar.

If the discount variable mortgage rate was to rise by 1.15% to 4.75%, as predicted by the CBA, then mortgage repayments would lift by 15% from their current level, adding $400 a month in repayments on the median priced Australian home.

However, if the discount variable mortgage rate was to rise in line with the futures market’s projection (i.e. 3.4% by August 2023), then average mortgage repayments would soar by 46%, adding a whopping $1,250 to monthly mortgage repayments on the median priced Australian home.

Either way, recent home buyers already suffering financial distress could easily be tipped of the edge at the same time as they are plunged into negative equity.