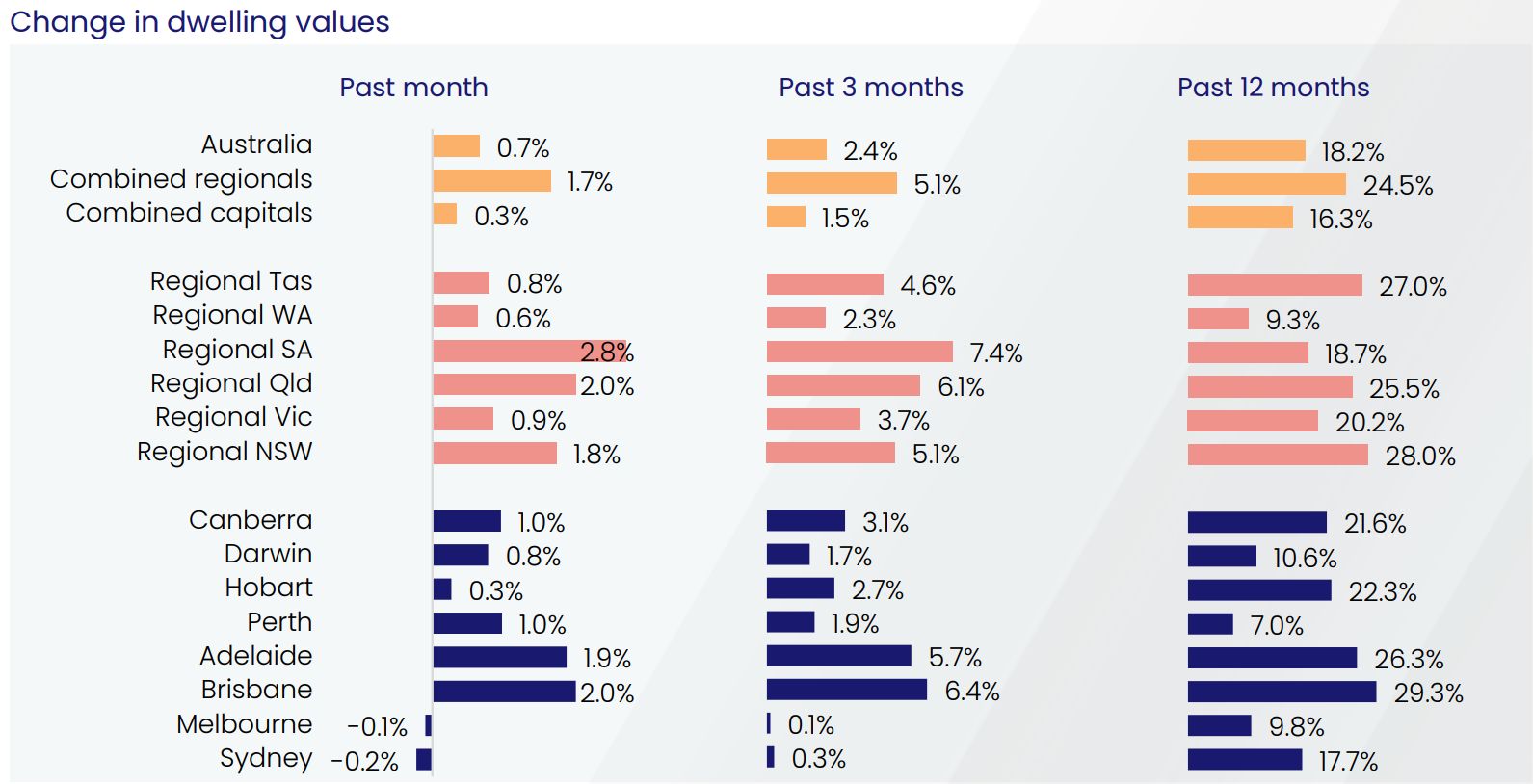

The latest CoreLogic dwelling value results for March showed that price growth has well and truly turned two-speed, with wild variation apparent between the capital cities, as well as between the capitals and the regions:

Two-speed housing market.

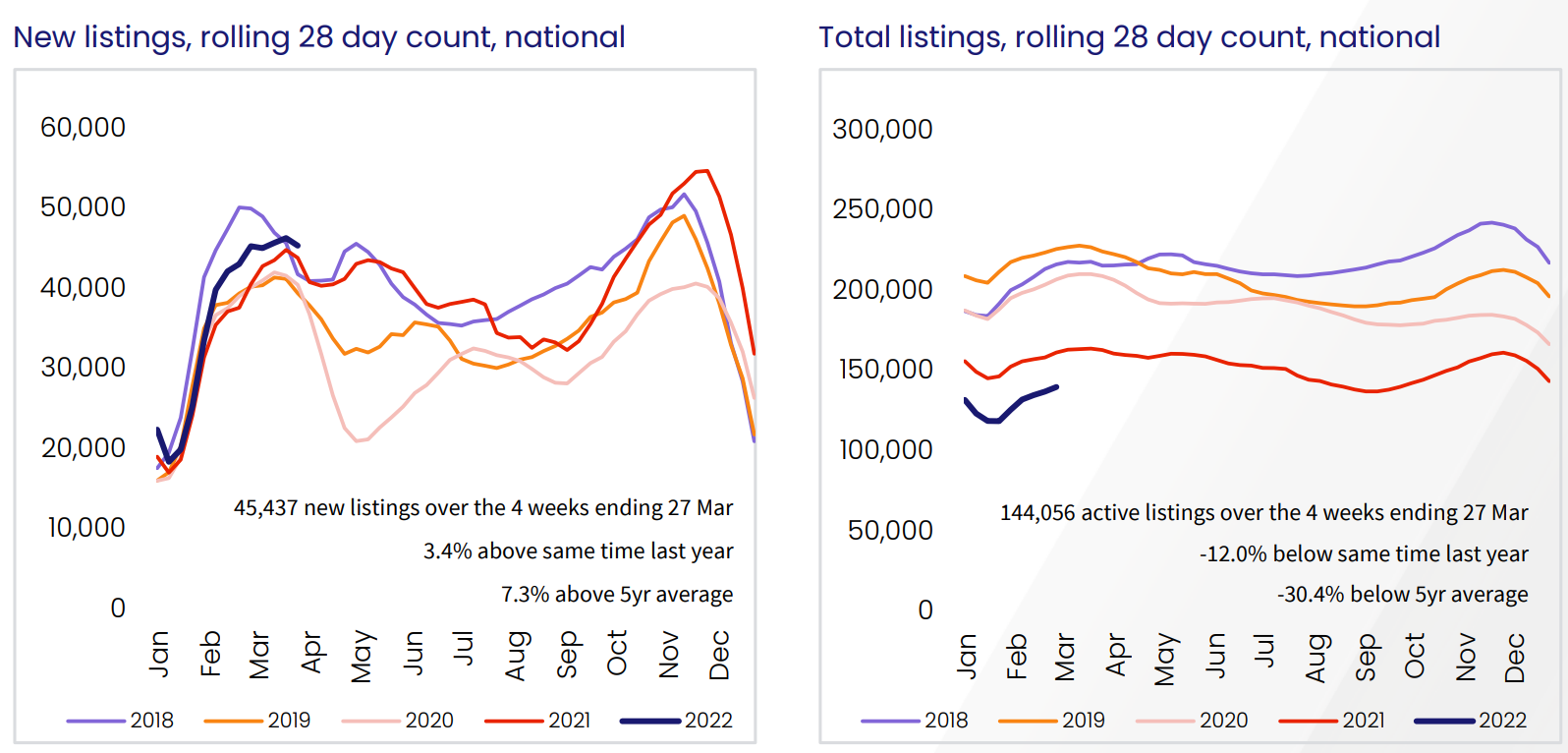

Interestingly, the biggest driver of the rises in dwelling values appears to be the collapse in property listings.

As shown in the next chart, advertised listings at the national level were tracking 30% below the previous five-year average in March:

Australian listings still very tight.

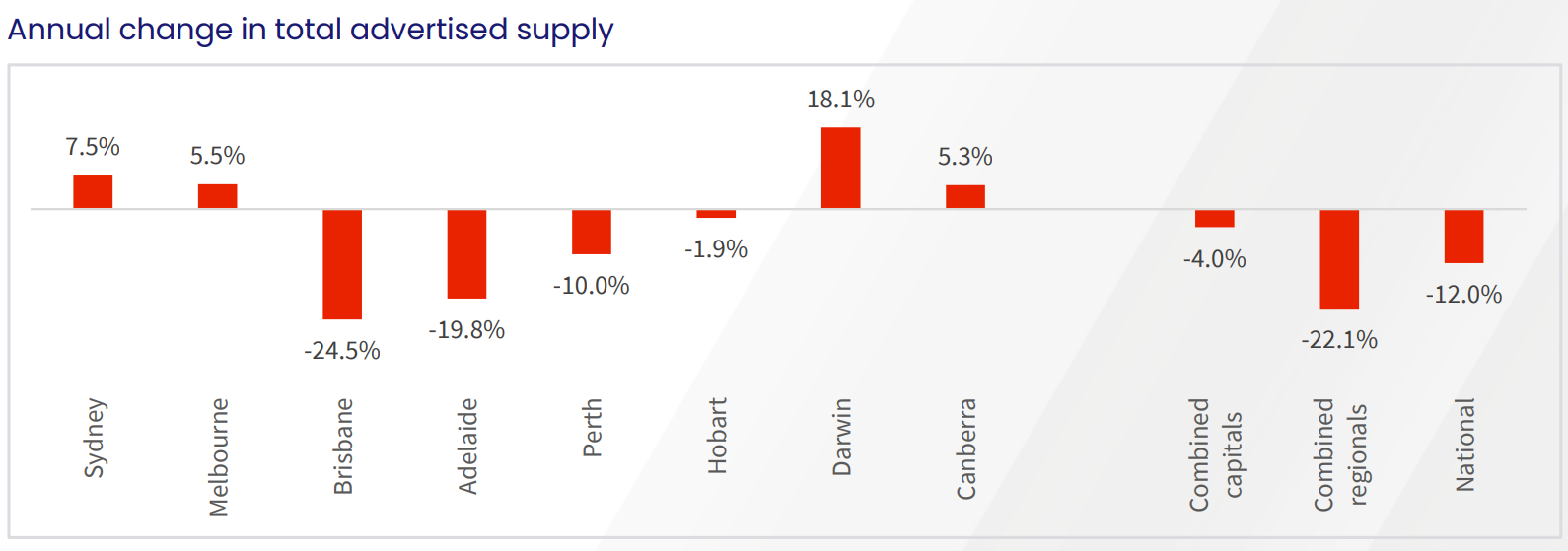

However, the decline in listings has been driven by the fastest growing markets, namely Brisbane, Adelaide and the regions:

Listings tightest in Brisbane, Adelaide and the regions.

By contrast, for sale listings have increased over the past year across Sydney and Melbourne, which helps to explain their recent price weakness.

As noted by CoreLogic:

In Melbourne, total advertised supply was 8% above the previous five-year average towards the end of March, while the number of homes available to purchase in Sydney had virtually normalised to be 7.5% higher than a year ago and only 2.6% below the five-year average. Higher stock levels across these markets can be explained by an above average flow of new listings coming on the market in combination with a drop in buyer demand.

“With higher inventory levels and less competition, buyers are gradually moving back into the driver’s seat. That means more time to deliberate on their purchase decisions and negotiate on price,” Mr Lawless said.

In contrast, advertised stock levels in Brisbane and Adelaide remain more than 40% below the previous five-year average levels and around 20% to 25% down on a year ago. It’s a similar scenario across regional Australia, where total advertised housing stock was 22% below last year’s level and 43% below the previous five-year average. Such low inventory levels along with persistently high buyer demand continues to create strong selling conditions in these areas, supporting the upwards pressure on prices.

Listings levels seems to be the key metric to watch over coming months for those interested in house price movements.