Business journalist John Beveridge has penned a ripping article lambasting the great Australian superannuation “rort”, which continues to lavish tax breaks on wealthy Australians, with the system resembling more of a tax planning scheme than a genuine retirement pillar:

The “rort”, which at this stage is entirely legal, is to build up superannuation funds to well in excess of what is required for actual retirement and then use the tax-sheltered environment as an investment account…

More than 11,000 people now have super balances above $5 million… The rort appears to be growing too, with more than 370 Australians younger than 30 now having superannuation balances exceeding $2 million…

All told, there are about 80,000 uber-wealthy self-managed super funds that are way above what is required to achieve a very comfortable standard of living in retirement…

The government’s retirement income review found a person with a superannuation balance of $5 million could achieve annual earnings tax concessions of about $70,000…

Mercer research… showed the tax concessions enjoyed by a single $10 million self-managed super fund could fully fund 3.1 full aged pensions.

That is not a fantasy figure either – there are 27 SMSFs that hold more than $100 million each in concessionally taxed savings in the 2018-19 financial year, including one mega-SMSF that had accumulated $544 million.

Those numbers are likely to have increased since then.

There are multiple reasons why Australia’s superannuation system is a tax dodge for the rich that actually drives inequality.

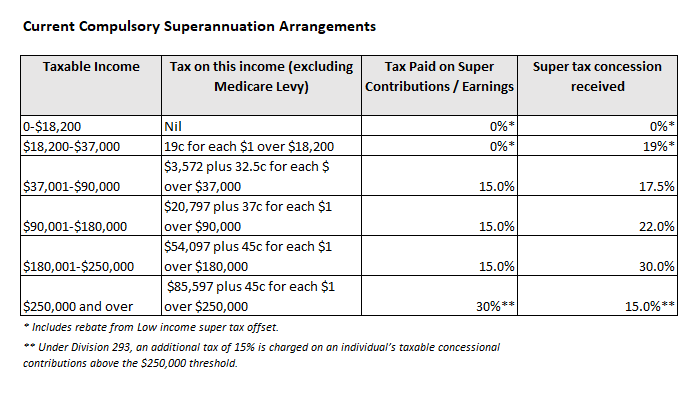

First, because of Australia’s progressive personal income tax system, the 15% flat tax on superannuation contributions and earnings means those higher up the income scale generally receive the largest tax concessions, as illustrated in the next chart:

Superannuation tax concessions typically favour high income earners.

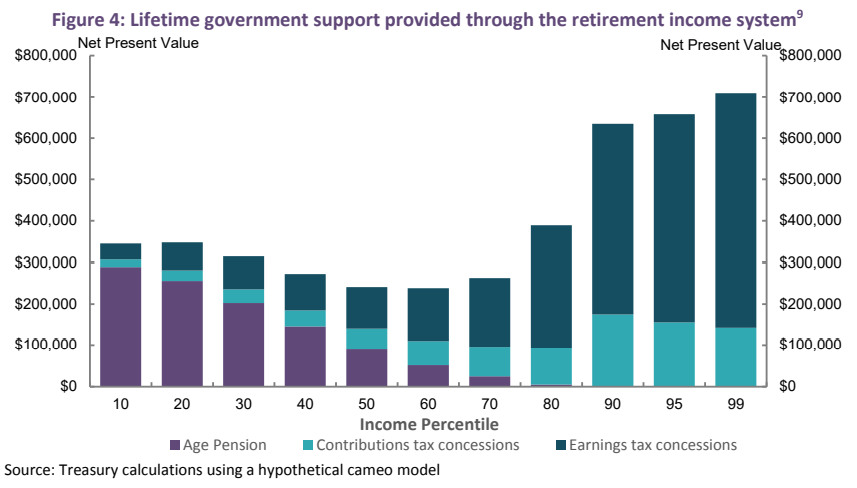

Since the size of one’s superannuation nest egg is also a function of how long one works and how much they earn, the lifetime taxpayer support provided via the retirement system is heavily skewed towards higher income earners, according to the Australian Treasury:

The wealthy earn far more retirement support than the poor.

As illustrated above, Australian taxpayers spend more than twice as much supporting the retirements of the top 1% of income earners than they spend supporting someone on the aged pension.

Looking at superannuation concessions specifically, the top 1% of income earners are projected by the Australian Treasury to receive more than $700,000 in taxpayer support over their working lives, roughly 14-times the $50,000 of concessions received by the bottom 10% of income earners.

Since men typically earn more and have less interrupted working lives than women, they also accumulate far bigger nest eggs.

Second, because higher income earners accumulate the largest superannuation nest eggs, the passing of fund balances onto their heirs will inevitably “increase intragenerational inequity”, according to Treasury’s Retirement Income Review:

Australia’s superannuation system entrenches inequality.

Ultimately, Australia’s compulsory superannuation system misses on almost every policy mark:

- It is poorly targeted away from those in genuine need.

- It costs the budget far more than it saves in aged pension costs.

- It reduces workers’ take home pay.

- It entrenches inequality by encouraging tax avoidance and wealth accumulation by the rich.

The superannuation system effectively takes the disparities in working-life incomes and magnifies them in retirement, enshrining inequality.

Australia would gain massively if it unwind the compulsory superannuation system and instead ploughed the billions in budget savings into a more generous universal aged pension – Australia’s true retirement pillar.

This would never happen of course. The superannuation lobby is now so large and powerful that it would bring down any government that dared tried to disband it.

To the contrary, a Labor Government is more likely to double-down and lift the superannuation guarantee even higher, since it is captured by the industry super lobby.