The latest data suggests that Sydney’s house price crash has begun.

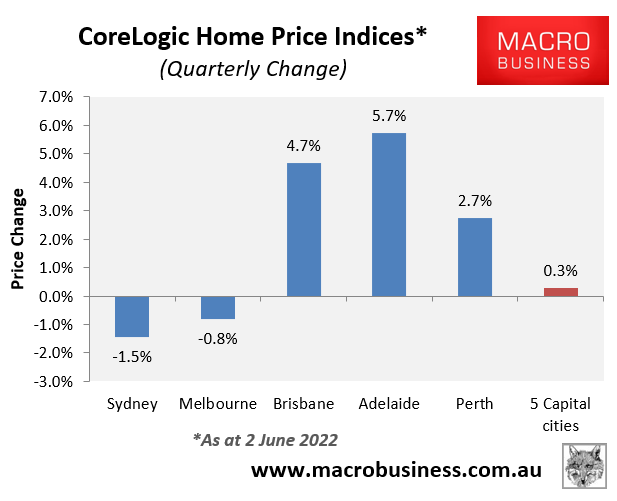

CoreLogic’s daily dwelling values index has Sydney leading the nation’s dwelling downturn with values falling 1.5% over the quarter:

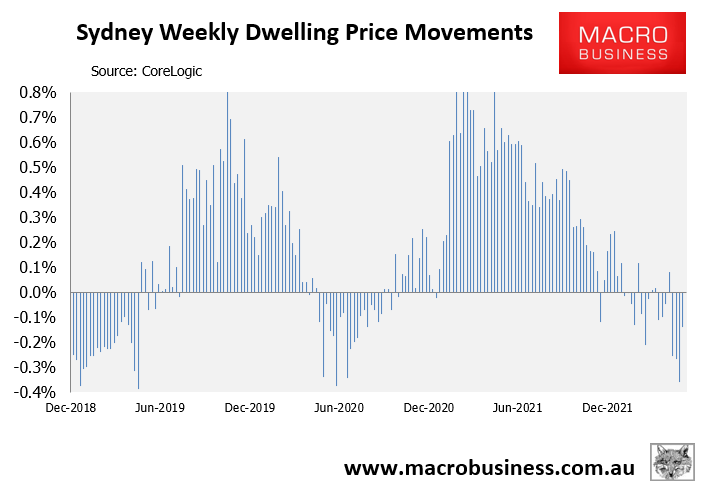

This decline has been delivered on the back of 12 weekly value declines over the past 18 weeks:

Advertisement

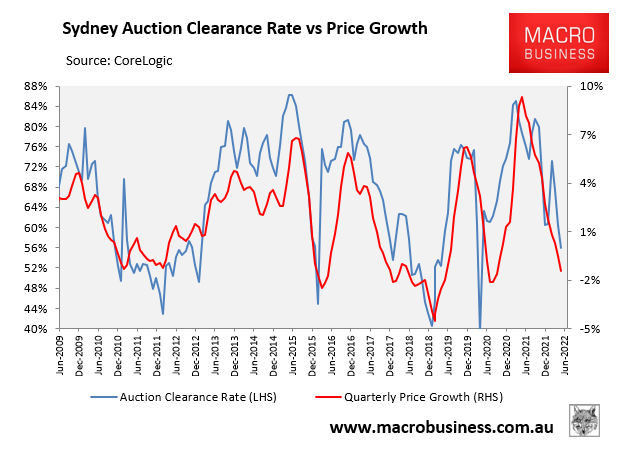

Sydney’s auction clearance rate has also collapsed into the mid-50s. This suggests that buyer demand has evaporated and points to further house price falls:

Advertisement

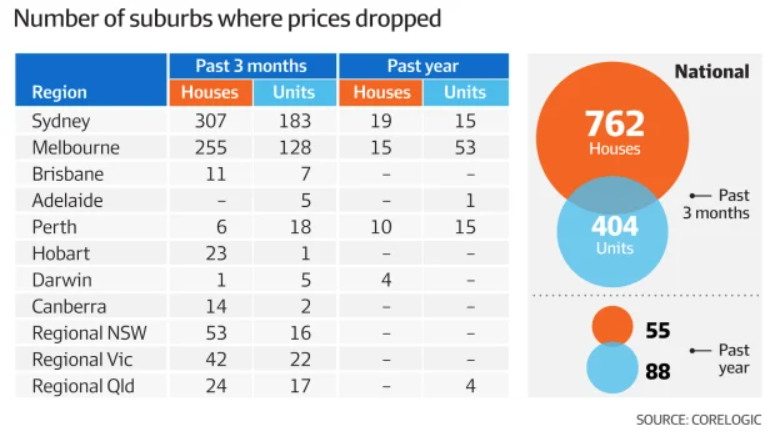

To add further insult to injury, new data from CoreLogic shows that house prices fell in 307 suburbs in Sydney over the May quarter, with many recent buyers now at risk of falling into negative equity:

House prices in more than half of all Sydney suburbs are now lower than they were three months ago, or a total of 307 house markets racking up quarterly losses. Nearly six in 10 unit markets in the city also notched up a quarterly decline…

“Those people who bought in our two major capital cities of Melbourne and Sydney in the last few months are the most likely to be vulnerable right now, especially if they have purchased with a 90 per cent to 95 per cent home loan, which many buyers have done,” said Margaret Lomas, founder of Destiny Financial Solutions.

The deteriorating situation has prompted Coolabah Capital’s Chris Joye to declare that “the great Aussie house price correction has started” with Sydney leading the way:

Advertisement

The key drivers of the great Aussie house price correction include:

A massive increase in fixed-rate borrowing costs with the typical 3-year fixed-rate jumping from circa 2% one year ago to 4.5% today…

Market perceptions that the RBA would start raising rates in 2022, which penetrated the popular consciousness in late 2021…

The RBA commencing its monetary policy normalisation process with an inaugural 0.25 percentage point cash rate increase in May 2022…

The RBA’s governor, Phil Lowe, advising the public in May that he expects to lift his target cash rate to at least 2.5%, which would mean that discounted variable-rate home loan costs will rise from circa 2% prior to the RBA’s May hike to 4.5% once the cash rate hits 2.5%. Financial markets have a much more aggressive view: they are pricing in a terminal RBA cash rate of 3.6%, which would imply that discounted variable-rate home loans will increase to 5.6%…

We expected the RBA to begin hiking in mid 2022 at the earliest (having planned to kick-off in June, they got the yips and started in May) with the first 100 basis points of RBA rate increases triggering a subsequent 15-25% correction in national home values, which would be the largest draw-down on record. Care of CoreLogic we now know that the great Aussie housing correction has indeed begun…

Note from the above that Coolabah Capital’s modelling predicts that the first 100 basis points of RBA tightening would trigger a “15-25% correction in national home values”.

Given the RBA and median economist expects the cash rate to rise to around 2.5% (i.e. 240 basis points of tightening), this would imply a full blown house price crash for the nation, led by its most expensive market of Sydney.

Advertisement

My view is that the RBA will be stopped-out well short of the 2.5% cash rate forecast, thereby limiting the damage. But Australia will still likely experience the biggest house price unwind in generations, with Sydney bearing the brunt.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.