By Gareth Aird, head of Australian economics at CBA:

Key Points:

- We expect the headline CPI to increase by 1.9% in Q2 22 (6.2%/yr).

- The trimmed mean CPI on our forecasts will rise by 1.3% (4.6%/yr).

- An outcome in line with our forecasts for both headline and underlying CPI should see the RBA raise the cash rate by 50bp at the August Board meeting.

Overview

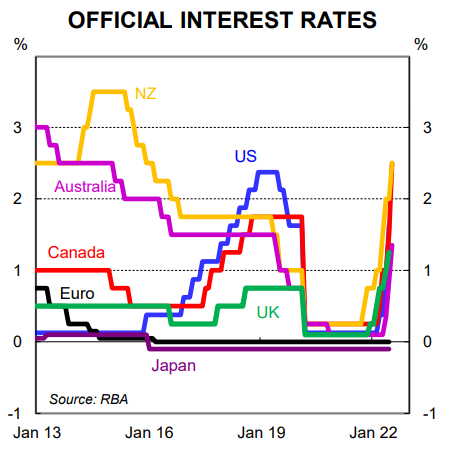

High inflation is now the main issue for central banks globally. Most major central banks are tightening monetary policy swiftly in an effort to put downward pressure on aggregate demand and in turn inflation.

The RBA argued over 2021 and early 2022 that Australia was ‘different’ on the inflation front. Indeed their primary concern was that inflation had to lift in a way that meant it was ‘sustainably with the target range’. As such, there was a specific focus on labour costs rising sufficiently to ensure that inflation would be ‘sustainably within the target range’. But those objectives are from yesteryear. In a short space of time the RBA, like many other central banks, have become inflation fighters.

The upcoming Q2 22 CPI, due to print on 27 July, is expected to show that inflation pressures remained red hot over the June quarter. This means that monetary policy will be tightened again at the August Board meeting. We consider our forecasts for both headline and underlying inflation to be consistent with the RBA increasing the cash rate by 50bp at the August Board meeting (the risks sits with a larger increase).

A brief recap of the Q1 22 inflation data

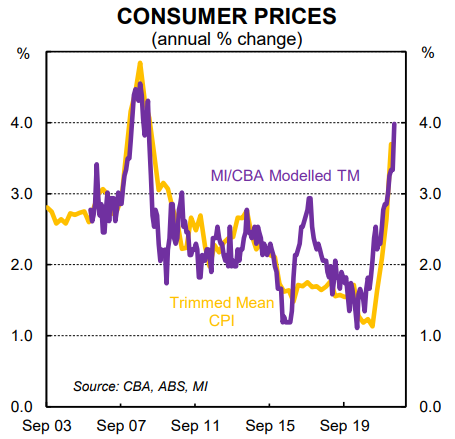

The trimmed mean, the RBA’s preferred measure of underlying inflation, rose by 1.4%/qtr over Q1 22. It was the strongest quarterly increase since 2008. The annual rate of the trimmed mean CPI accelerated to 3.7%. Interestingly, the other measure of underlying inflation, the weighted median, came in significantly lower at 1.0%/qtr. The annual rate of the weighted median lifted to 3.2%, which means there is a significant spread between the two measures. That spread may narrow in Q2 22.

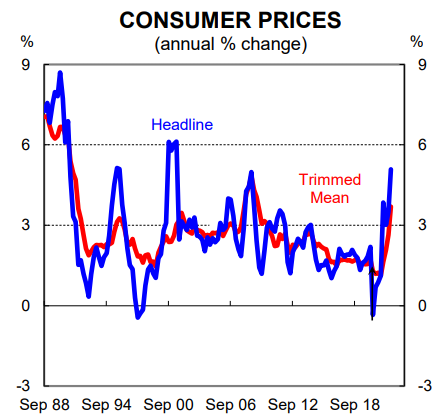

The headline CPI in the March quarter was also very strong. It rose by a whopping 2.1%/qtr in Q1 22 following a big 1.3%/qtr increase in Q4 21. The headline rate of inflation accelerated to 5.1%. It was the strongest annual rate of inflation since 2001 when the introduction of the GST caused a temporary spike in domestic inflation. The headline rate will further lift in Q2 22.

There was evidence of broad-based inflation in the Q1 22 CPI. And the overall message was not positive for households because inflation sits well above the annual rate of wages growth (recall that the Q1 22 wage price index was 0.7%/qtr and the annual rate is 2.4%). That picture will not improve in Q2 22.

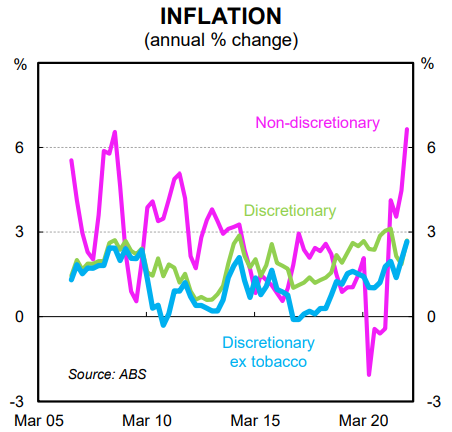

Non-discretionary annual inflation was significantly higher than the Q1 22 CPI and more than twice the rate of discretionary inflation. Put another way, the prices of goods and services that households have to purchase (e.g. groceries, petrol and housing) is running well ahead of price increases for non-essential goods and services. That picture is not anticipated to change in the Q2 22 CPI.

What to expect in the Q2 22 CPI

We expect there to once again be evidence of both demand pull and cost push inflation in the upcoming CPI. Input costs have risen in part due to supply side bottlenecks and the war in Ukraine. And floods on the East Coast of Australia have disrupted the production of fruit and vegetables which has put significant upward pressure on food prices at both the wholesale and retail level.

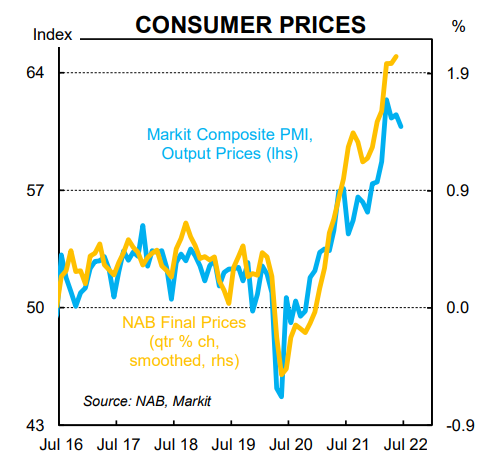

Private surveys like the NAB business survey and the Markit PMIs capture the strength of the inflationary pulse.

Our forecast is for the headline CPI to increase by 1.9% in Q2 22 which would see the annual rate lift sharply to 6.2%. The more policy relevant trimmed mean CPI on our figuring will rise by 1.3%/qtr. This would see the annual rate lift to 4.6%.

Here we should stress that the RBA’s rapid monetary policy tightening since May will not have any impact on the Q2 22 CPI (or Q3 22 inflation data given the lags between changes in the cash rate and consumer inflation).

The detail

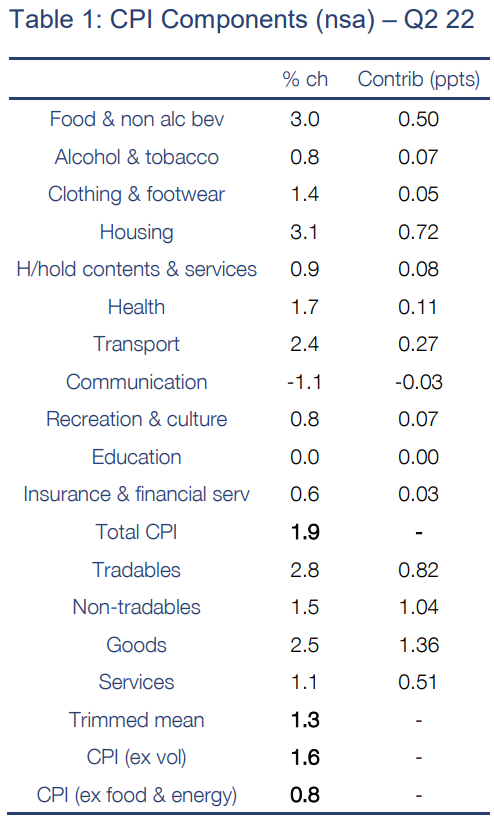

See Table 1 below for our detailed forecasts for the Q2 22 CPI basket.

The main features of our call are as follows:

- a big rise in food prices of 3.0% following a large 2.8% lift in Q1 22;

- a solid 1.8% increase in transport primarily driven by a 5.3% increase in petrol prices;

- a 1.4% increase in clothing prices which is slightly more than the usual seasonal increase;

- a large 3.1% lift in housing driven by a big lift in the cost of building a home and utilities prices and a more modest increase in rents;

- a flat outcome for education prices in line with the usual seasonal pattern and a 1.7% increase in health prices; and

- a 0.8% lift in recreation and culture prices (note that recreation prices generally fall in the June quarter so a quarterly outcome in line with our forecast would be represent a strong result).

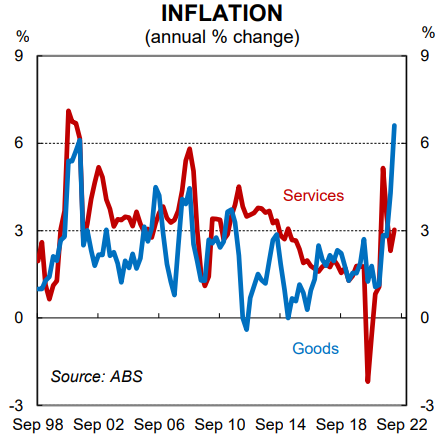

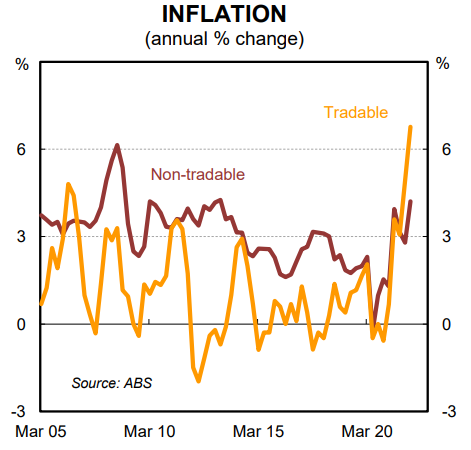

Our expectation is that tradables inflation (i.e. imported inflation) will be significantly stronger than non-tradables inflation. And goods inflation is likely to once again print higher than services inflation (note that the primary driver of services inflation is wages).

On our calculations the CPI excluding food and energy will increase by 0.8% over Q2 22 which would take the annual rate to 4.4% (from 4.0%). The RBA does not put much weight on this measure, but we think it is important. The RBA cannot do much to influence the price of food or energy. And this measure of inflation indicates that whilst inflation is uncomfortably high, the headline rate has been pushed significantly higher by price rises in items (namely food and energy) that are beyond the control of the central bank.

Inflation and the RBA

Governor Philip Lowe recently stated that the RBA now expects inflation to peak at ~7% by the end of the year. This was an upward revision relative to the RBA’s inflation forecasts in the May Statement of Monetary Policy (SMP) – headline inflation was forecast to peak at 5.9% in Q4 22 in the May SMP.

It unusual for the RBA to revise their inflation forecasts between quarterly official forecast updates. But this upward revision has in large part been the basis for the RBA hiking rates in 50bp increments over the past two months rather than moving in ‘business as usual’ 25bp steps as they did in May.

Whilst we do not have an official updated inflation profile from the RBA, based on Governor Lowe’s recent comments on inflation we believe that the RBA’s updated implied inflation forecast for headline CPI in Q2 22 would be broadly in line with our call (note that the RBA has not commented on any updates to their core inflation forecasts, albeit they will also be upwardly revised in the August SMP).

If the headline and underlying inflation rates print roughly in line with our forecast we expect the RBA to increase the cash rate by 50bp at the August Board meeting. A material upside surprise to both headline and core CPI over Q2 22 relative to our forecast would raise the risk of a 75bp increase at the August Board meeting.

At the moment market pricing sits between the 50bp hike we expect and a 75bp increase for the August Board meeting, where some market participants are placing their views. This pricing in part represents the big hike done by the Bank of Canada and the recent discussion of large increases from the US FOMC. But it is worth reminding readers that the RBA Board meet more frequently than most other central banks which reduces the need to deliver a large 75bp hike at any given monthly meeting (here we must stress that 50bp is twice the size of a ‘business as usual’ 25bp hike – the economic fraternity is at risk of ‘normalising’ 50bp hikes).