By Gareth Aird, head of Australian economics at CBA:

Key Points:

- We have revised our central scenario for the RBA based on the latest labour force data, a further modest upward adjustment to our near term inflation forecasts and our expectation that the RBA will follow the path of a number of other global central banks in aggressively hiking the policy rate over coming months.

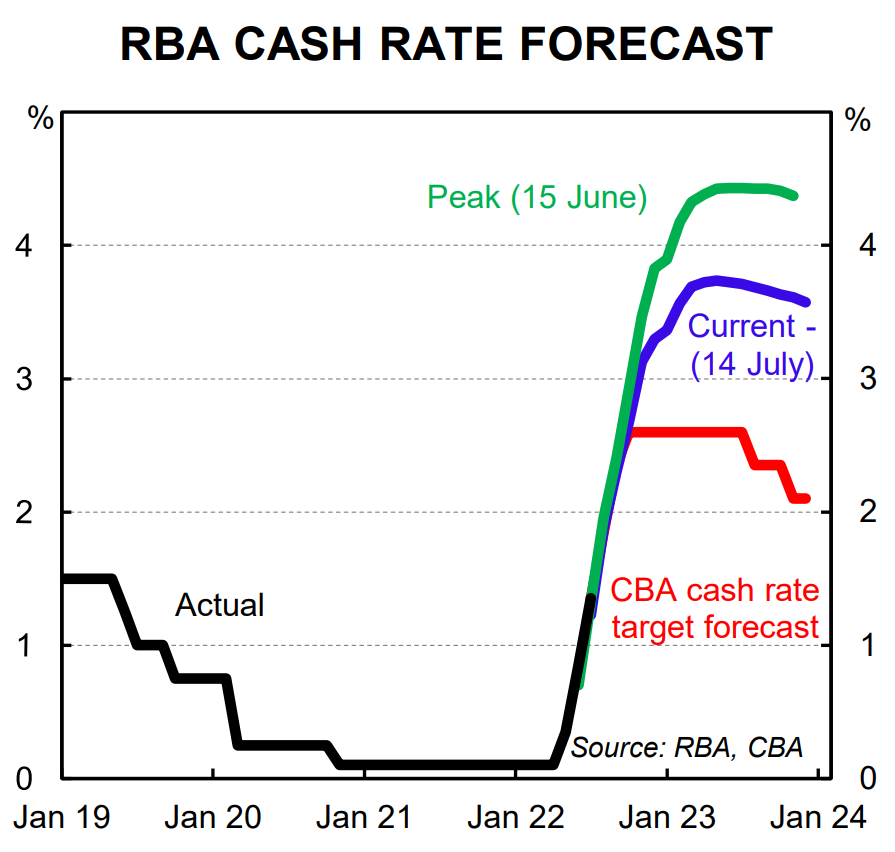

- We now expect the RBA to increase the cash rate by 50bp at both the August and September Board meetings which would take the cash rate to 2.35%.

- We anticipate one further 25bp rate hike in November which would take the cash rate target to 2.60% (our updated terminal rate which is ~100bp above our estimate of the neutral cash rate).

- Financial conditions will continue to tighten over 2023 with no change in the cash rate given the big fixed rate home loan expiry schedule and the impact of the Term Funding Facility being unwound.

- We retain our call for the RBA to cut the cash rate by 50bp in the second half of 2023 and have pencilled in August and November for 25bp cuts.

We upwardly revise the RBA terminal rate to 2.60% – significantly contractionary

We have revised our central scenario for the RBA. We had previously expected the RBA to take the cash rate to 2.10% by November (noting the risk sat with a 2.35% end year cash rate). But given the recent strength of the labour market data coupled with a largely co-ordinated response of central banks globally to raise policy rates quickly we have amended our profile.

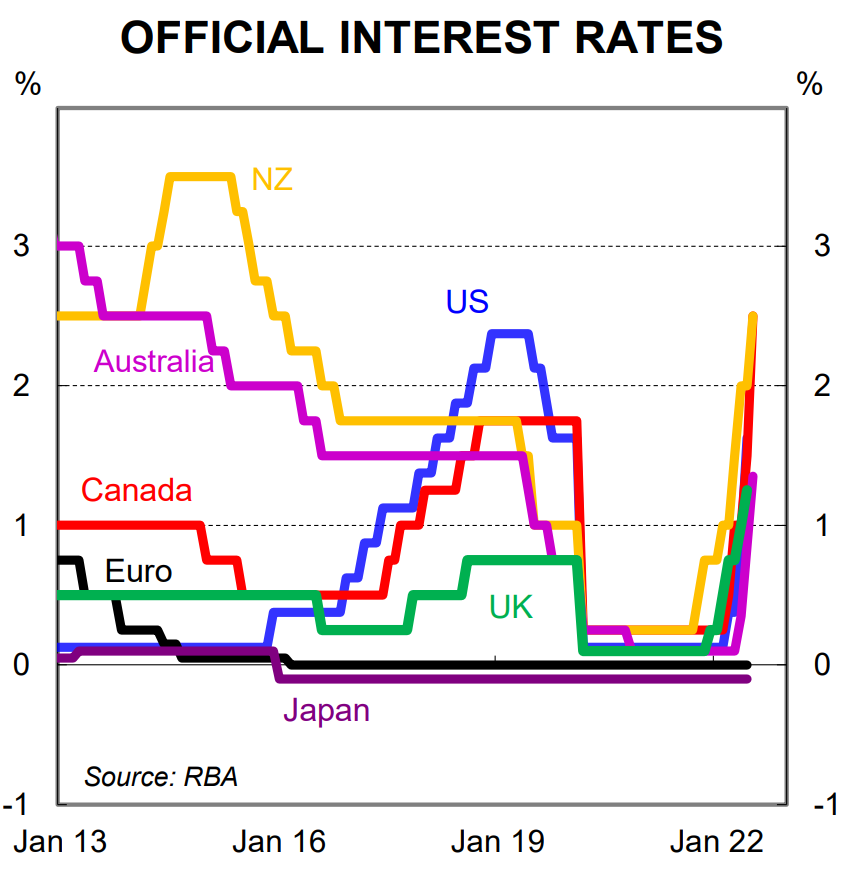

We now expect the RBA to raise the cash rate target by 50bp at both the August and September Board meetings. This would see the cash rate target at 2.35% in September. If the RBA delivers 100bp of tightening over the next two meetings it would mean that the RBA has taken the cash rate up by 225bp over just four months (five meetings).

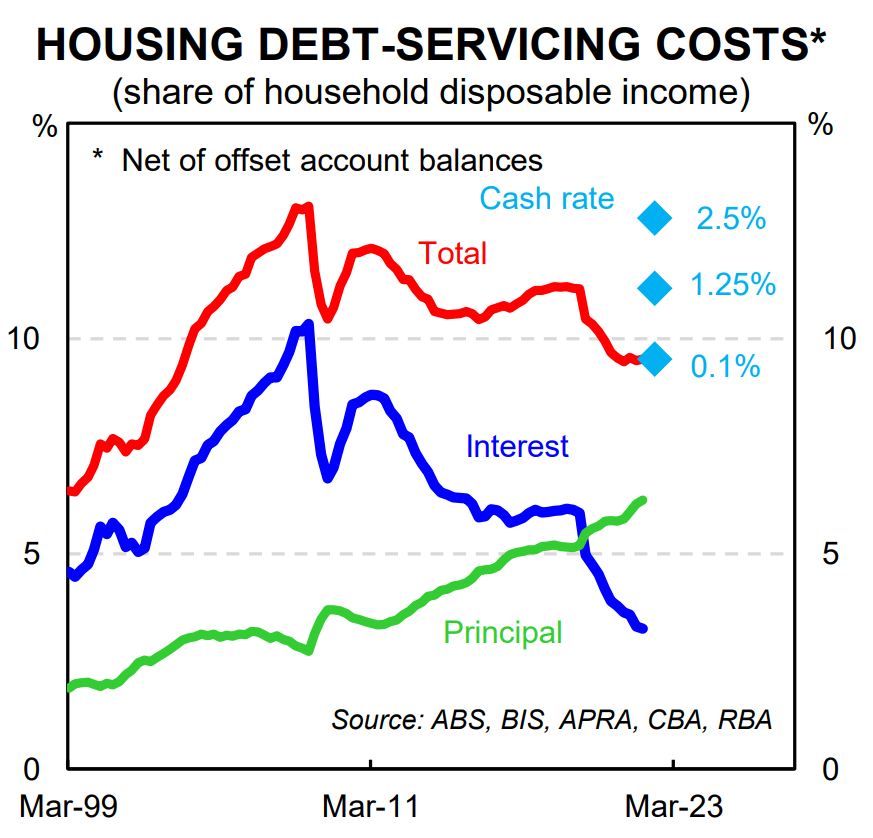

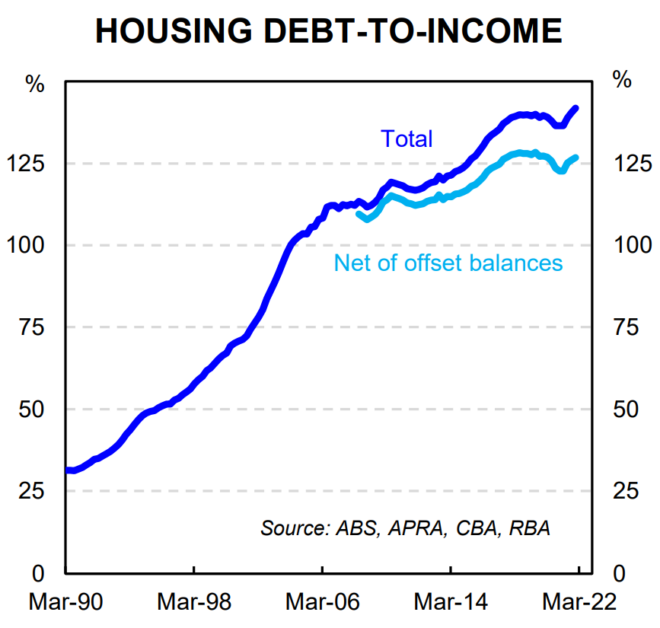

This would represent an incredible pace of tightening, particularly given the starting point was a cash rate of just 0.10% and household debt sits at a record high as a share of income (Australia has one of the most indebted household sectors in the world).

The impact on households with a mortgage will be very significant given the percentage change in the mortgage rate will be incredibly large. Some households with a home loan with be insulated, at least initially, if they are on a fixed rate loan. But the majority of home borrowers are on floating rate loans and the interest cost on their debt will go up very quickly. Softer growth in consumer spending will follow and there is a clear risk that the volume of household consumption falls by late 2022.

Our updated forecast profile is of course based on what we think the RBA will deliver and not what we believe the RBA should do (as is always the case).

There will be significant dichotomy in the economic data over coming months. We expect forward looking indicators of the economy to slow sharply while backward looking indicators, notably the unemployment rate, inflation and wages, will continue to strengthen. We got a taste of the major disparity in the backward and forward looking data this week.

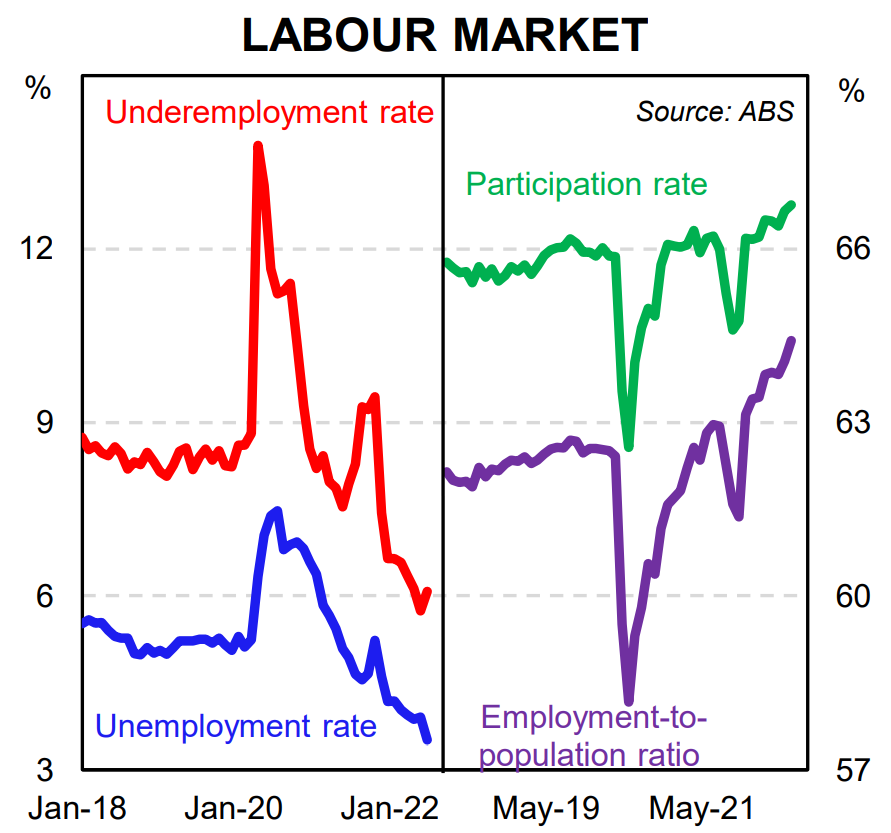

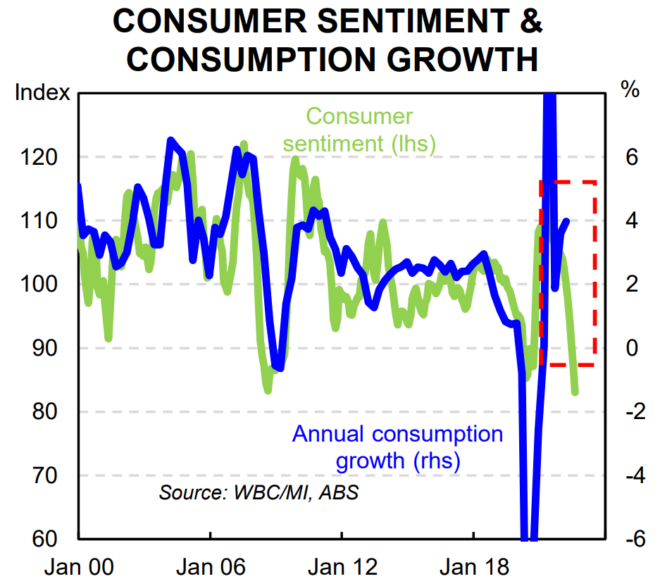

The unemployment rate dropped to 3.5% in June, its lowest level since 1974. In contrast, consumer sentiment, as measured by the Melbourne Institute/WBC monthly survey, slumped to just 83.8 (deeply pessimistic territory).

Households are not just concerned about rising inflation. They are very much concerned about rising interest rates (which in turn will put downward pressure on inflation).

According to the latest consumer confidence survey sentiment amongst those polled after the RBA’s July 50bp rate hike was 7.4% below that of those surveyed before the decision (the survey was taken over the week beginning 4 July).

Falling home prices are also feeding into growing anxiety about the economic outlook, particularly for those households who have entered the housing market more recently and are faced with the combination of rising rates and falling dwelling prices (a bad mixture for both the household budget and balance sheet, which in turn negatively impacts consumer confidence).

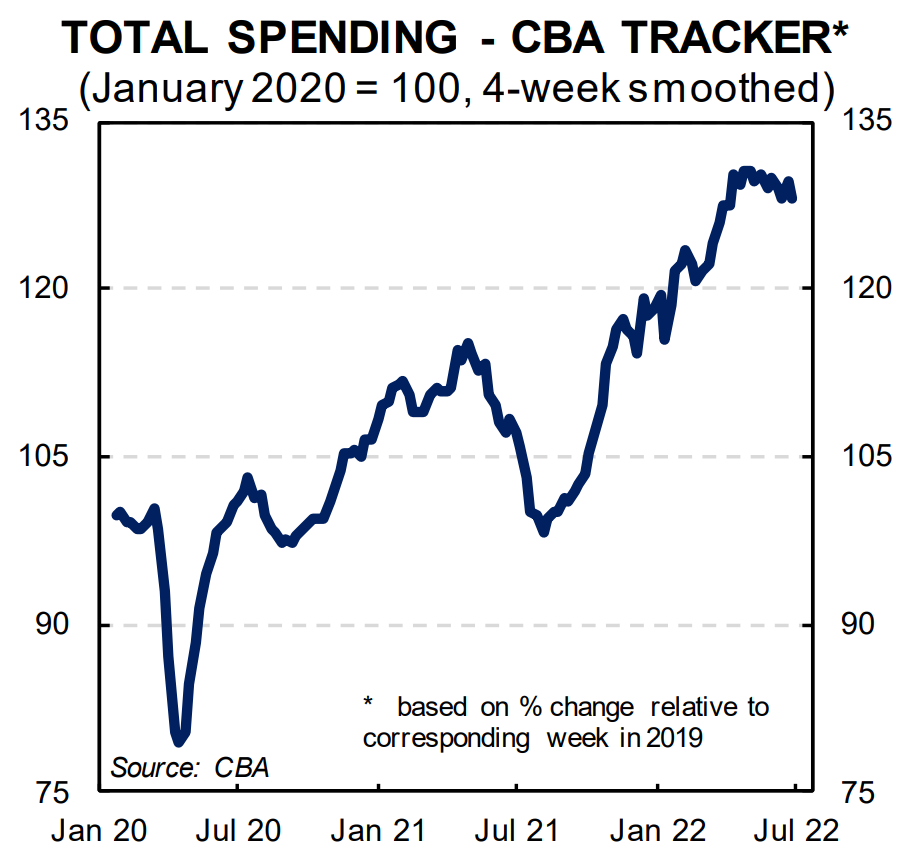

Consumers who are concerned about the economic outlook invariably spend less, though not necessarily straight away. The lags, however, between changes in sentiment and spending decisions are not particularly long. And there is evidence in our internal credit and debit card data that spending momentum has cooled considerably (see below chart).

Despite forward looking indicators of the economy slowing and the expectation they will weaken further we now anticipate that the RBA will continue to raise rates at a rapid pace over the next two months.

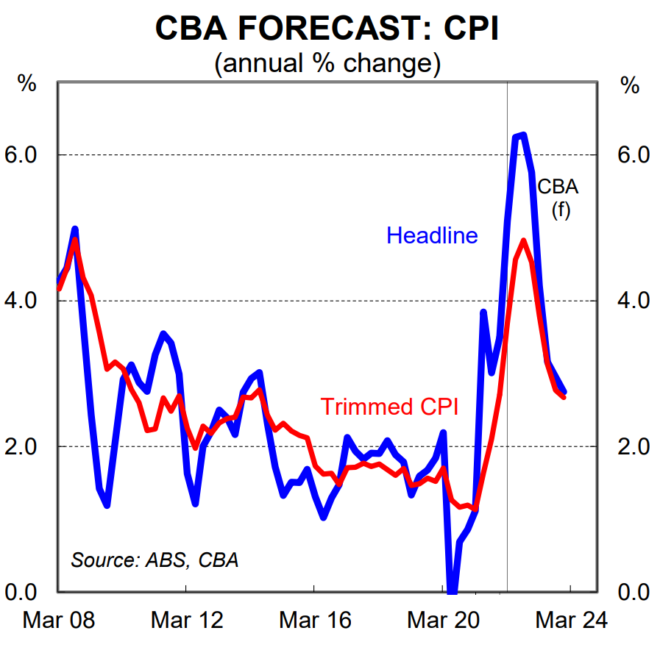

Our expectation is for the headline Q2 22 CPI to increase by 1.9%/qtr which would take the annual rate to 6.2%. We forecast the trimmed mean, the RBA’s preferred measure of underlying inflation, to increase by 1.3%/qtr which would see the annual rate step up to 4.6% (our full preview will be published next week).

We believe inflation data in line with our forecast coupled with the recent labour market data will see the RBA raise the cash rate by 50bp in August. The risk sits with a 75bp hike rather than a 25bp increase, although we see the risk as low.

The RBA Board meet more frequently than most other central banks which reduces the need to deliver such a large hike at any given monthly meeting (here we must stress that 50bp is twice the size of a ‘business as usual’ 25bp hike – the economic fraternity is at risk of ‘normalising’ 50bp hikes).

There is a strong case to pause after delivering another 50bp hike in August (note that by that stage the RBA will have increased the cash rate by 175bps in just three months; over four meetings). But we think the RBA will be sufficiently concerned about the tightness in the labour market, capacity constraints and a potential shift in “inflation psychology” that they will increase the cash rate by a further 50bp in September. Note that we do not share those same concerns.

Our central scenario sees the RBA pause in October. And we have one final rate hike for this cycle in November (25bp which would take the cash rate to 2.60%).

If the RBA wanted to send a clear signal that they intended to stay on hold for an extended period of time after November they could increase the cash rate by 15bp which would take the target to a conventional metric of 2.50%. We suspect, however, that the RBA will not have enough conviction at that point to send such a signal given the Q3 22 inflation data is likely to be red hot (it prints 26 October).

We assess the neutral cash rate to be ~1.50%. As such, our forecast for the cash rate to peak at 2.60% means we believe policy will end up significantly contractionary (note that the RBA does not share our view of neutral and think it is more likely to be ~2.50%; i.e. the mid-point of their inflation target).

A contractionary policy setting means below trend growth in 2023 and a subsequent lift in the unemployment rate unless there is a new round of fiscal stimulus (not out base case). As such, we do not expect any rate hikes in 2023 and we continue to expect rate cuts in 2023 (we have pencilled in August and

November).

Our expectation for a terminal rate of 2.60% versus our previous call of 2.10% should imply further downward revisions to our forecasts for home prices (we expect dwelling prices to fall by 15% peak to trough). But given we have pulled forward the expected timing of cuts in 2023 we leave our forecasts for home prices unchanged.

Despite the change in our call for the cash rate our overall message remains unchanged. RBA rate hikes will be powerful and will slow momentum in the economy considerably.

The total stock of household debt has not disappeared (or been paid down) and borrowers are facing a very large percentage change in the interest cost on their debt. Fixed rate borrowers will be rolling off an average fixed rate mortgage of around 2¼% onto a rate around 4½-5% in 2023 based on our forecast profile for the cash rate. This will result in a very big step change in the interest cost on debt (for context, mathematically moving from a mortgage rate of 8% to 16% is the same as 2¼% to 4½% in terms of what happens to the interest cost on debt; it doubles).