One of the better Wall Streert analysts, Michael Hartnett at BofA, recently said that markets will stabilise if there is no “Lehman event” Well, there is one underway in China:

The clock is ticking for the world’s most indebted developer, whose liquidity woes sparked a broader debt crisis in China’s property industry that’s gone on to engulf more home builders, threaten banks and pose growing challenges for President Xi Jinping.

China Evergrande Group, once the country’s largest real estate firm, previously said it was on track to deliver a preliminary restructuring plan by the end of July. That leaves mere days for the builder with about $300 billion of liabilities, just as a shakeup stirs fresh uncertainties.

The group said Friday that Chief Executive Officer Xia Haijun was forced to resign amid a company probe into how 13.4 billion yuan ($2 billion) of deposits were used as security for third parties to obtain bank loans, which some borrowers then failed to pay back. Chief Financial Officer Pan Darong was also made to step down.

The property crash is epic, unchanged and heading for China’s banking system. The Last Bear Standing explains:

There are two distinct elements to financial viability: liquidity and solvency.

Being liquid means that you have the cash you need to operate the business today. You can pay your bills.

Being solvent means that you will eventually be able to repay all your debts, or that your assets exceed your liabilities.

While both elements matter, liquidity is much harder to fake. Determining solvency, however, requires forward looking assumptions that are easy to manipulate and are harder for an outside observer to disprove2.

The property developers that have failed have been insolvent for years, they just lied about it. Evergrande never reported a loss and its balance sheet showed that current assets exceeded its current liabilities. This farce continued because the company had liquidity through financing channels. When the liquidity dried up, the charade was over.

The same concept applies to banks.

Given the massive exposure to the collapsing property sector and the history of grossly underreported non-performing loans, it is likely that some Chinese rural and midsize banks are insolvent today3. Of course, none will admit this reality, and it is nearly impossible for an outsider to determine independently due to lack of clear and reliable information. It is only once these banks become illiquid that their insolvency becomes unavoidable. A bank failure will not happen based on a reasonable expectation of future losses, but rather, it will happen when one runs out of money.

Pressure on rural and midsize bank liquidity is growing4.

Every loan that goes unpaid puts liquidity pressure on banks (even if it is “extended”). A year ago, the list of delinquent borrowers included just a handful of developers, but now it has grown to include nearly all of the largest developers, their suppliers, and homebuyers.

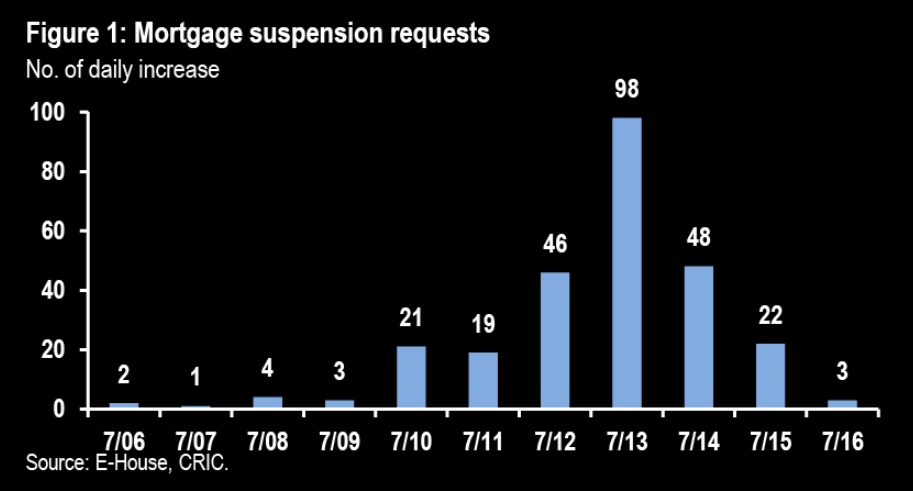

In recent weeks, owners of unfinished apartment projects have begun to organize mortgage boycotts that have quickly spread to over 300 projects in 90 cities and are estimated to involve mortgages worth 2 trillion yuan. This is a startling new development that prompted an emergency bank meeting with regulators. So far, banks are being asked to provide even more funding to bankrupt developers in order to help keep construction going. As construction at projects stall, this problem only grows.

Liquidity pressure can also come from the depositors. If individuals become concerned about a bank’s health (perhaps due to a rapidly expanding mortgage boycott), they will try to pull out their money. Glimpses of this phenomenon were visible recently as depositors protested outside several rural banks in Henan after being denied withdrawals since April5.

Finally, when other banks become concerned about a bank’s health (perhaps due to a rapidly expanding mortgage boycott and a bank-run of depositors), they will stop lending to it in the interbank market.

Then, the bank fails.

The Prognosis

In plain English, what do I expect to happen next?

Here are some high-confidence working assumptions:

The Chinese banking system is overrun with bad debt and non-performing loans, which are mostly hidden from regulators and public investors

Property represents the largest exposure of banks. Rural and mid-size banks have the highest exposure to the worse property markets

More developers and their suppliers will default and the cumulative weight of their delinquency will put pressure on banks

Mortgage boycotts will continue to spread – people will not pay for houses that don’t exist

Central authorities have no “master plan” to address these problems

Based on these assumptions, the following conclusions are likely:

Faith in at-risk banks will continue to erode leading to further liquidity pressure from depositors and lenders

Some banks will fail

The remaining question is whether a failure will happen at a large enough bank to create panic in the financial sector. My best guess is yes.

Remember Huarong? The “bad debt bank” was clogged with its own bad debt prompting a too-big-to-fail scare before the property downturn even began. This year, a second AMC, China Great Wall Asset Management, failed to produce an audit as well. USD bond yields on both companies are approaching 10% – a large spread implying significant credit risk.

Meanwhile, many publicly traded banks stocks are at or near all-time lows. Even the major state-owned banks have continued to trend lower and are now trading at 0.3x of book equity on average, considerably lower than prior periods.

While trying to pinpoint the weakest link is next to impossible, there are a couple to keep your eyes on – national banks smaller than the state-owned conglomerates but large enough to ripple through markets such as Minsheng, Everbright, Bohai, and Ping An.

It’s also possible that trouble could originate in an non-bank financial sources – insurance products (think AIG), shadow banks, wealth management products to name a few. There are no end to risks in this high-stakes game.

Banks are now contending with an uncontrolled implosion of their largest borrowers, a revolt from mortgage payers and a bleak, slowing economy overall. It won’t be an easy path forward, and there will be more casualties.

The chain reaction is in motion, the last domino will fall.

Advertisement

That sounds right to me. It will not mean a Lehman-style seizure of the overall banking system because China can always force publically owned banks to lend. But it will entail disruption to lending and some credit rationing as counterparty risk surges. It already is.

Beyond an immediate crisis, it will also mean interminably slower growth as bank balance sheets are weighed down in perpetuity a’la Japan post-1990.

Thus, it spells the end of the great Chinese property ponzi.

Advertisement

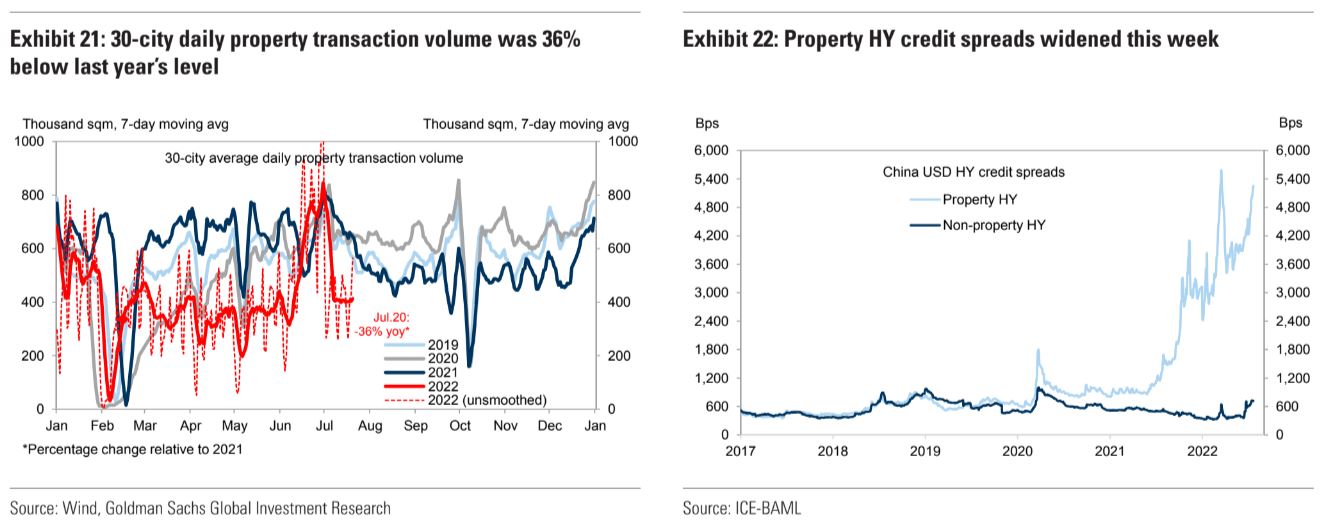

Where are we today in that process? Sales are still down bigly but the base effect is beginning to slow year-on-year falls. Developers continue to face ever greater funding pressure:

The second point is critical. The latest efforts to prevent contagion are targeting developer funding. BofA:

Advertisement

The million-dollar question remains what policy actions to expect next. Regulators havemoved torein in the risks, as the China Banking and Insurance Regulatory Commission (CBIRC) urged local governments and banks to work together to ensure projectcompletion and delivery. Posts on the mortgage boycott have been removed, and media reported that the government is considering to allow homebuyers to temporarily halt mortgage payments on stalled projects. However, the government has yet to offer any top-down plan to address this problem.

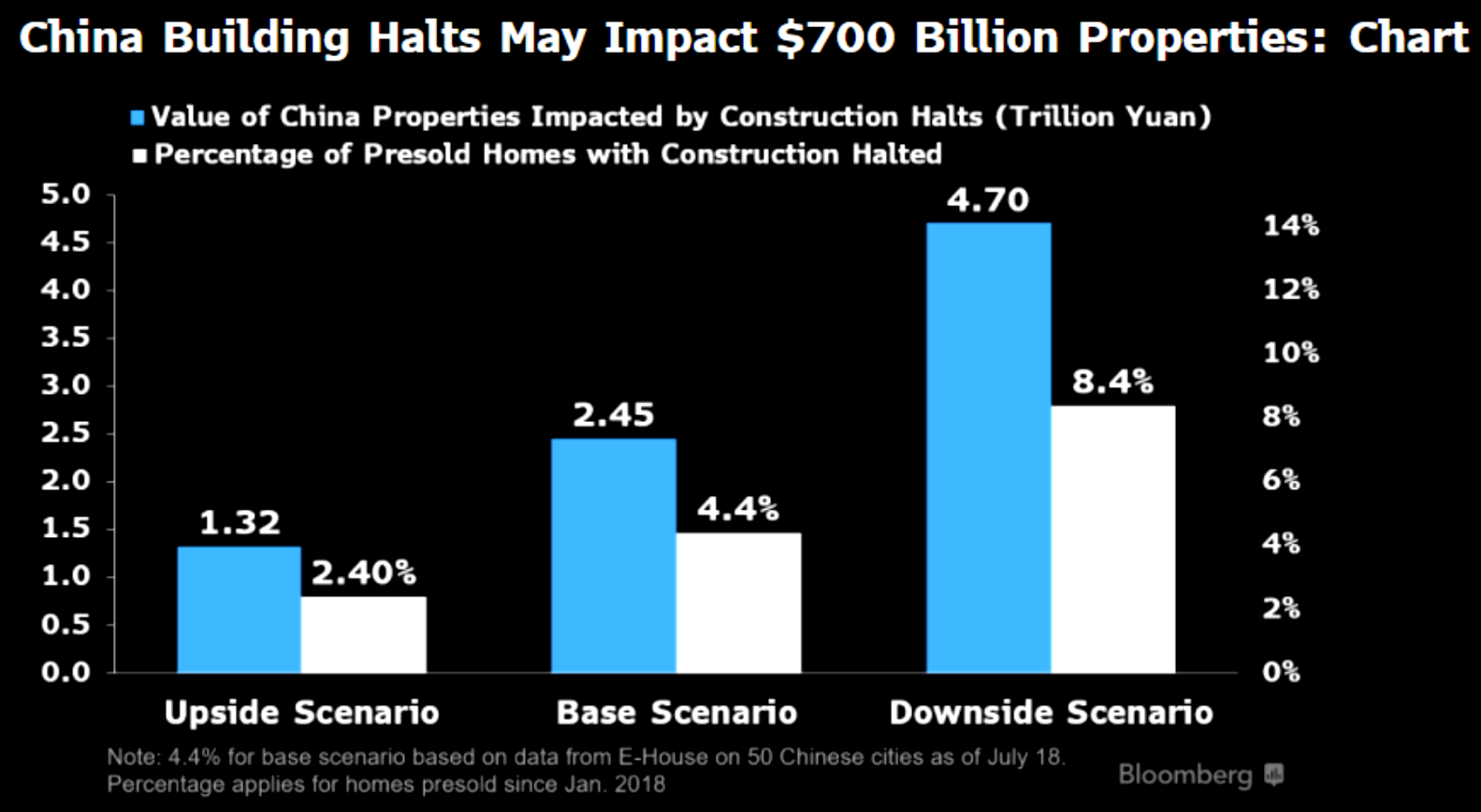

Given the potential scale of suspended construction (est. 244mn sqm), we estimate asmuch as RMB1.2tn worth of funding would be needed to ensure project completionacross the country. This is not a small number, especially as the Chinese governmentalready faces a sizable fiscal shortfall of nearly RMB3.5tn this year. In our view, given the fiscal strains and concerns about moral hazard, top decision makers are unlikely to roll out any top-down “bazooka” measures to tackle the problem.The most likely policy outcome is to have local governments, local government financing vehicles (LGFVs) and state-owned enterprises (SOEs) step in to complete unfinishedprojects batch by batch. This solution, if carried out successfully, has the potential to backstop the housing market and gradually rebuild confidence, without overextending the government’s fiscal resources. Since private developers have little liquidity or credibility left now, the key would be to leverage local governments’credibility to secure funds for construction.

In the absence of strong top-down policy intervention, further downside risks to the property market seems inevitable. Even if local governments could step in and complete the unfinished projects in 2H, it would take time to restore market confidence. Combined with the recent COVID flare-ups, grim labor market outlook, and slower household income growth, home sales growth might not see a sustainable recovery in coming months, even with the help of a lower year-ago comparison base. Property investment growth could turn out to be even weaker than we had anticipated earlier (-4% in 2022). With the stalled projects and new starts likely to remain incontraction (Exhibit 11), spending on construction and installation, which makes up more than 60% of the total real estate investment, could continue to drag the headline property investment growth in 2H22. We now expect property investment to decline by 7% this year. Even with a rebound in infrastructure fixed-asset investment (FAI) in 2H, this could still shave off headline FAI growth by 0.7ppt. Moreover, the negative impact may not be felt just in the property sector. More than 28% of China’sGDP is directly or indirectly related to the property sector, if we take into account all the upstream sectors and key downstream consumer sectors. This implies stiff headwinds on China’s economic growth in the coming quarters. More policy easing measureswill be warranted to help stabilize growth and confidence, in our view

Fine. But leaving it to be addressed piecemeal often backfires:

Xi’an announced all presale funds of commodity housing units should be deposited directly into escrow accounts. Ningbo plans to hold a meeting with 6 developers to address the presale supervision & market regulations.Tianjin investigates the financing needs & Chongqing formed risk resolution team to tackle the stalled projects.

Advertisement

Notice how some of these make the developer funding needs worse, not better, such as enforcing escrow account integrity. I can’t see how the context improves when such idiosyncrasies rule the day.

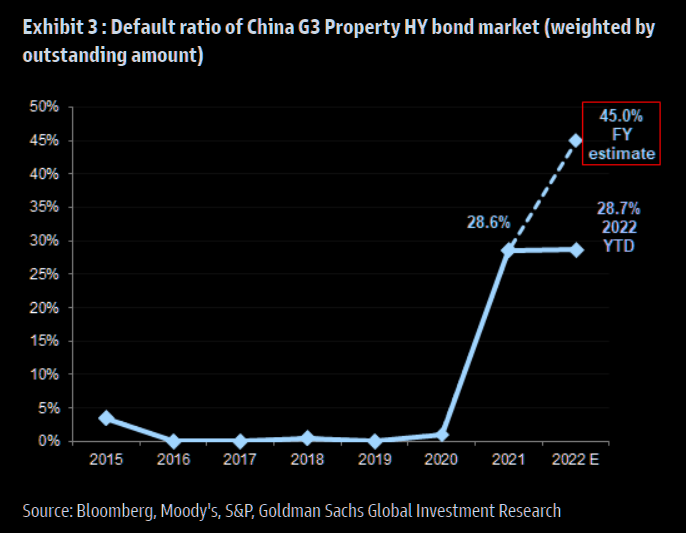

The loan losses are climbing:

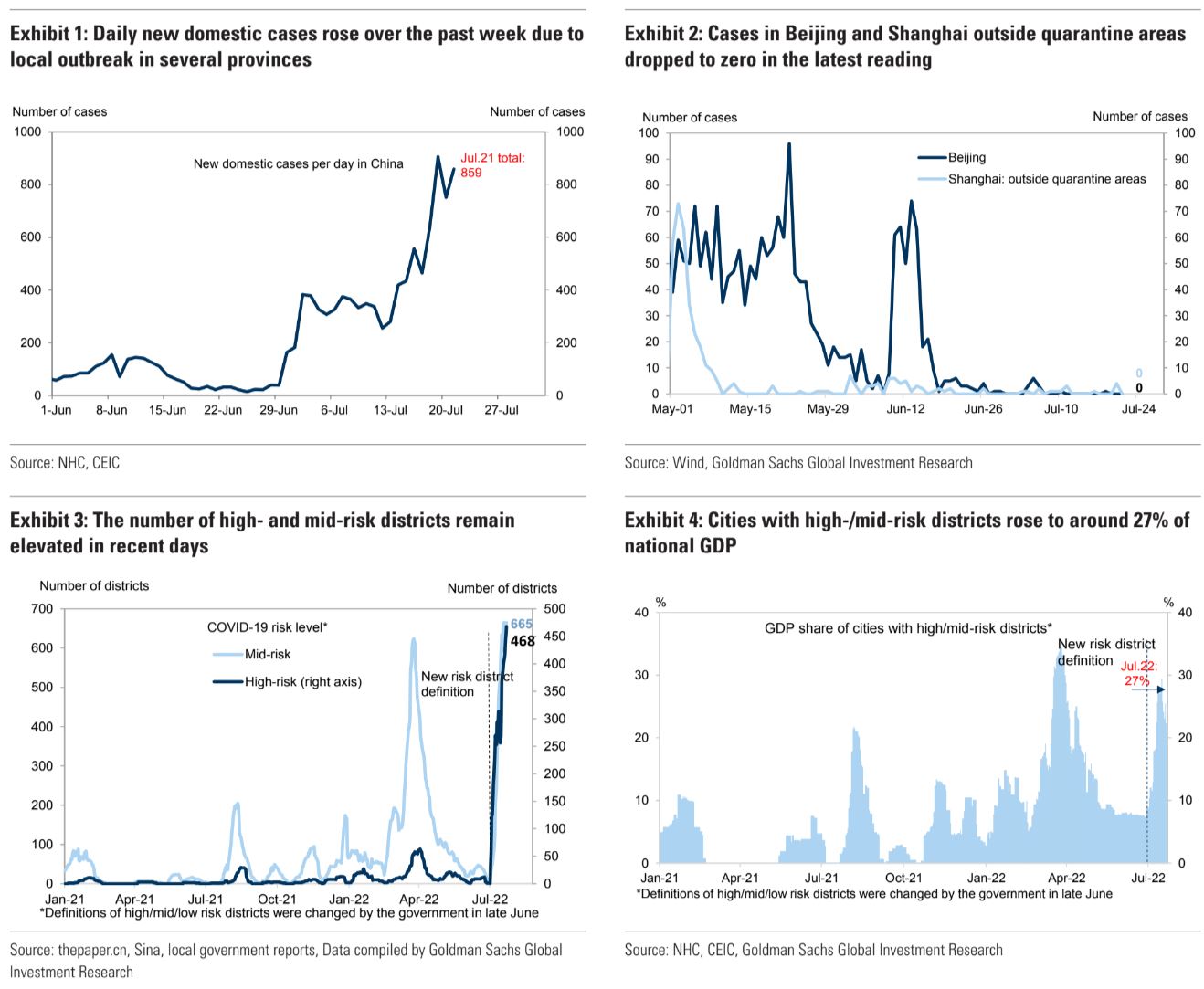

Add to this COVID which will keep breaking out:

Advertisement

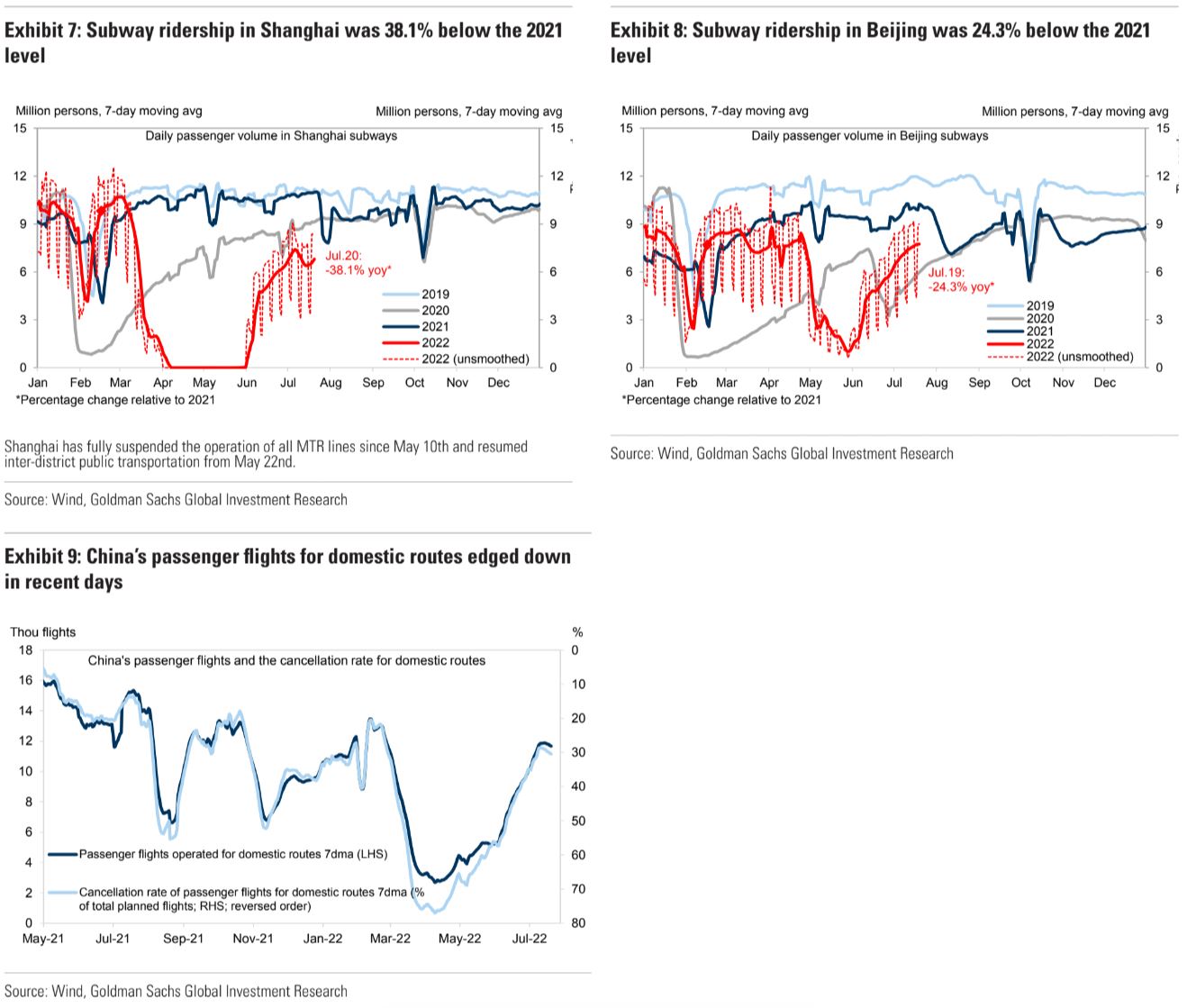

Mobility is struggling again:

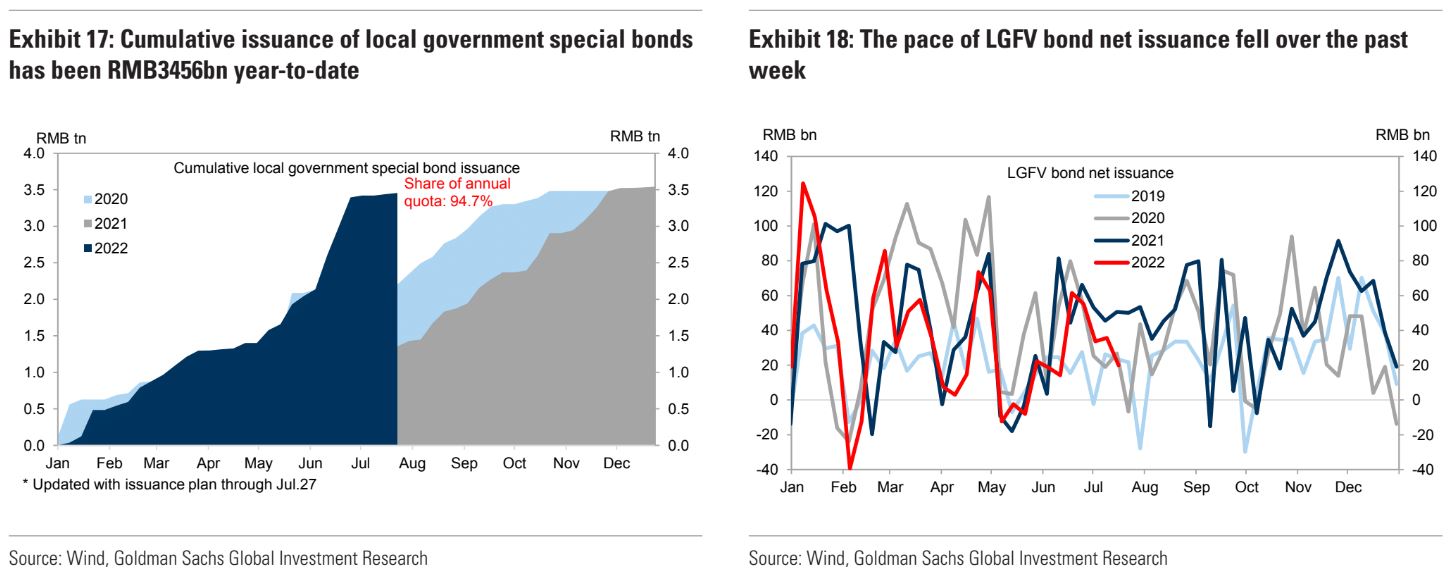

But, there is still the infrastructure push to support activity even if it is inadequate:

Advertisement

There will need to be more easing. A lot more. That’ll mean more pressure on the CNY as the crisis grows. Goldman:

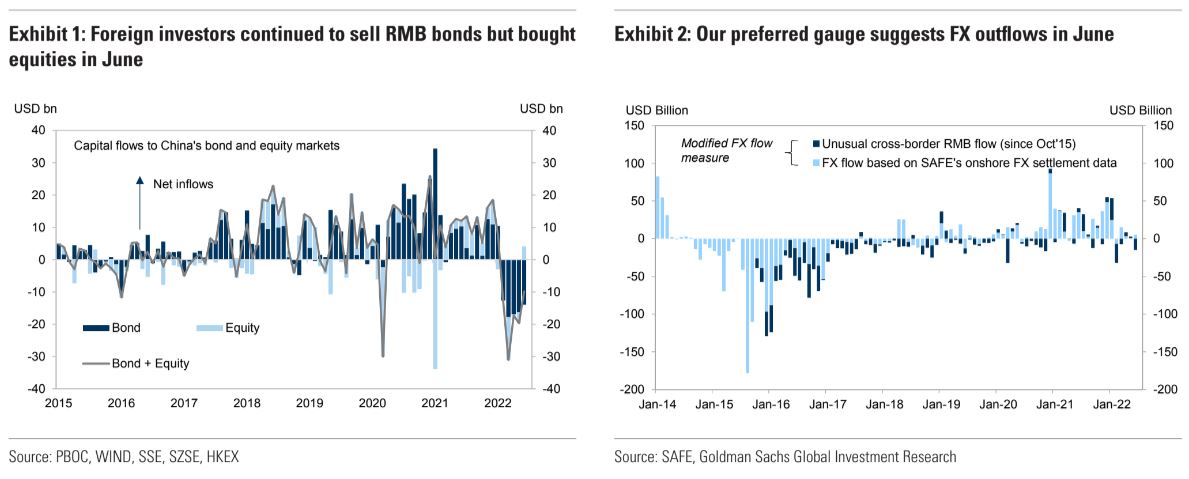

In June, we saw US$4bn in net inflows via onshore outright spot transactions, and US$2bn inflow via freshly entered and canceled forward transactions. Another SAFE dataset on “cross-border RMB flows” shows that domestic banks made net RMB payments of US$15bn from onshore to offshore. Our preferred FX flow measure therefore suggests in total US$9bn outflows in June, in comparison with US$2bn inflows in May (Exhibit 1).

China can prop up falling banking dominos to prevent an outright Lehman event but a falling CNY and weak commodity prices amid the looming trade shock is how this crisis can go global.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.