Last week, Westpac and ANZ hiked their fixed mortgage rates by 0.5% and 0.9% respectively, which more than doubled fixed rates from a year earlier.

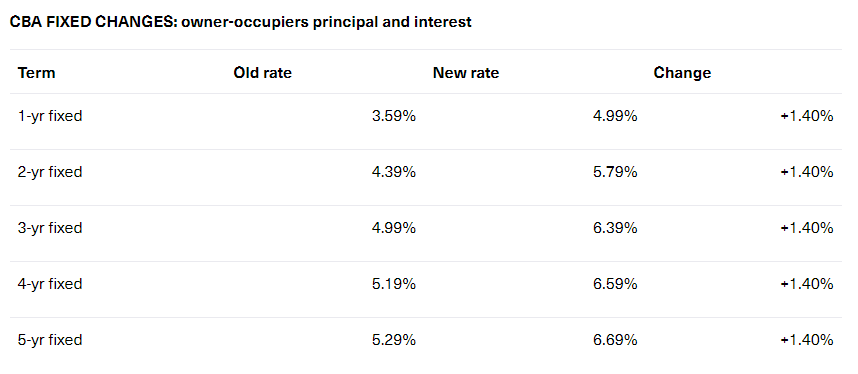

Yesterday, Australia’s biggest bank CBA joined the fold hiking its fixed rates by a whopping 1.4% across all loan terms:

This has taken CBA’s fixed mortgage rates to more than double or triple the level of a year ago, depending on the loan term:

RateCity.com.au research director Sally Tindall described the hikes as “incredible” and expects other banks to follow CBA’s aggressive lead:

“Today’s fixed rate hikes from Australia’s biggest bank are anything but typical”.

“The bank is responding to the rising cost of fixed rate funding and a market that refuses to believe the RBA will stop hiking the cash rate at around 2.50 per cent,” she said.

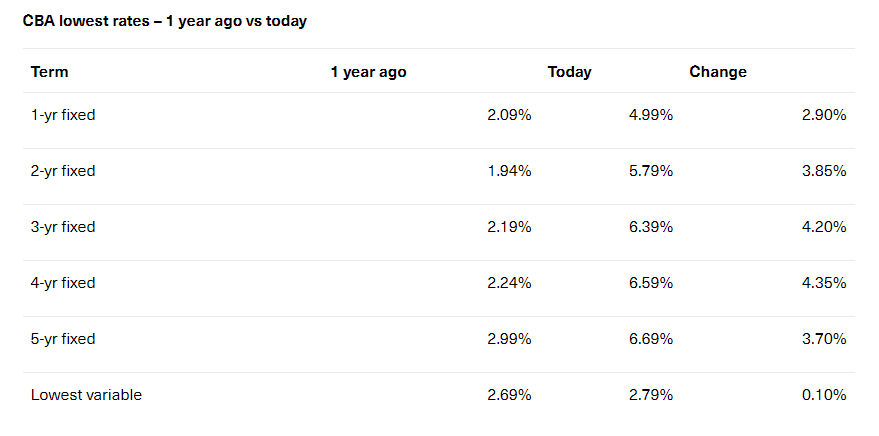

“Less than a year ago, CBA was still offering one fixed rate under 2 per cent. Today the bank’s lowest fixed rate is just under 5 per cent, while the majority are well over 6 per cent.

“It’s incredible to see fixed rates move this dramatically in such a short space of time. The sub-2 percent fixed rates from 12 months ago now seem like a distant dream.

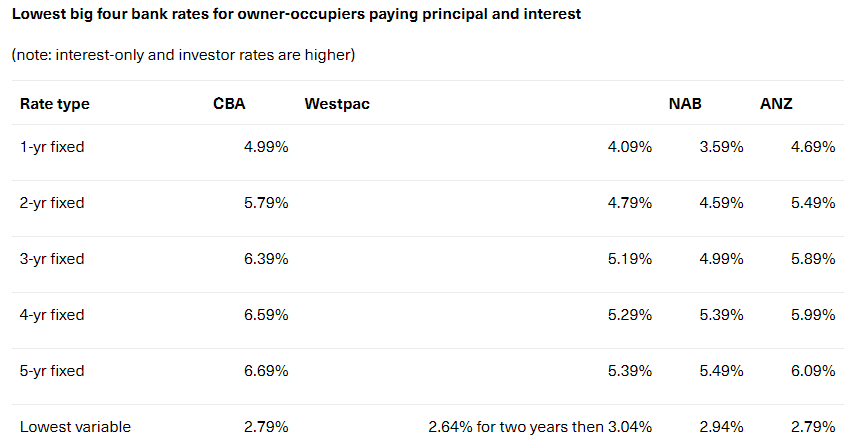

“We expect other banks will follow in CBA’s wake. Westpac and NAB’s fixed rates are now, in many cases, over a percentage point lower. It’s only a matter of time before these banks hike fixed rates again”.

Fixed mortgage rates are now universally high across the major banks:

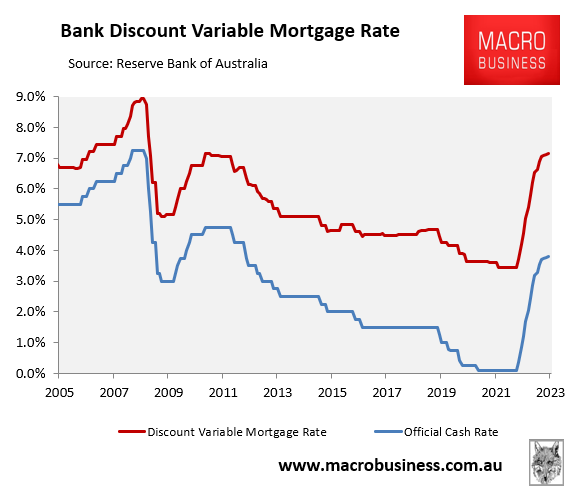

Variable rates are currently much lower, but will catch up with fixed rates as the Reserve Bank hikes aggressively.

If the futures market gets its way, and the official cash rate hits 3.15% by Christmas and 3.7% by June 2023, then the average discount variable mortgage rate will soar to 7%:

Futures market: 7% discount variable mortgage rate by June 2023.

Then there will be blood on the mortgage streets and the housing market will crash.