The AFR’s latest survey of 31 economists reveals a median forecast for the official cash rate (OCR) of 2.35% by December and a peak of 2.85%. Thus, Australia’s OCR would rise another 2.0% from its current level under the economists’ median projection.

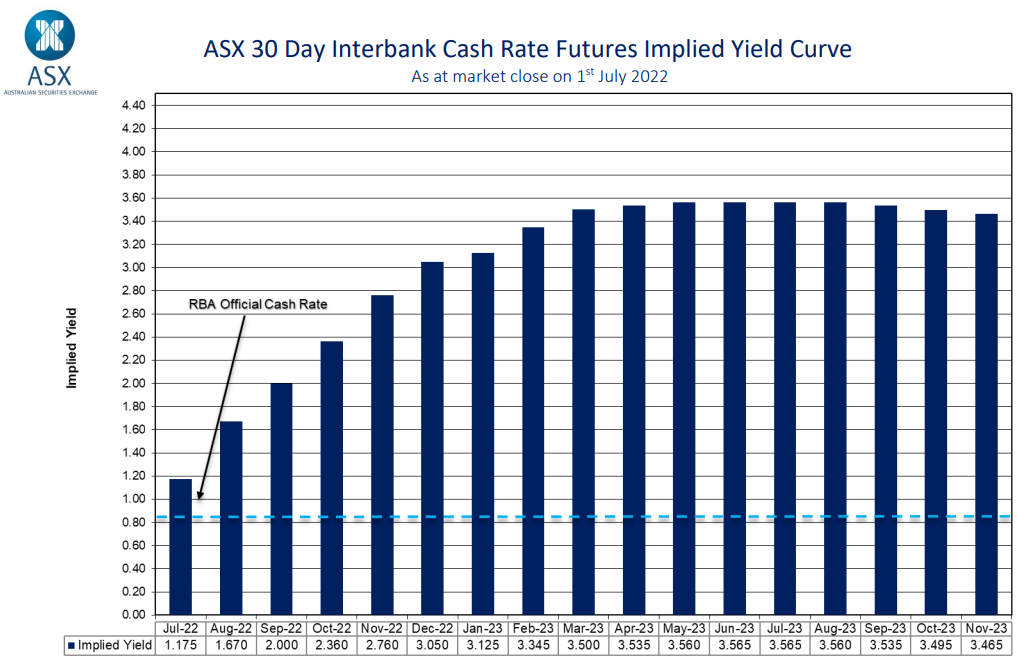

The futures market remains even more bullish, tipping an OCR of 3.0% by December and 3.6% by June 2023:

Futures market still bullish on rates.

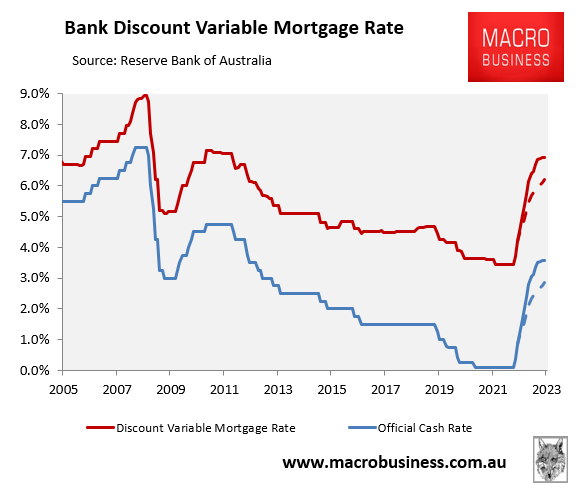

If either interest rate forecast came to fruition, it would see Australian mortgage rates soar.

Assuming increases in the OCR are passed onto mortgage holders, Australia’s average discount variable mortgage rate would climb to 6.2% under the economists’ forecast (dashed red line below) and to 6.9% under the market’s forecast (solid red line below):

Australian mortgage rates are tipped to soar.

The market’s OCR forecast would mean that the discount variable mortgage rate would climb to precisely double its level (3.45%) before the Reserve Bank’s tightening cycle, whereas the economists’ forecast would be 0.7% lower. Either way, Australian households would face a gigantic rise in monthly mortgage repayments, which would see many fall into severe financial stress, would hammer house prices, and would see household consumption – the main driver of the Australian economy – fall sharply, risking a painful recession.

For these reasons, I believe both the market’s and economists’ OCR projections are unrealistically bullish and will yet again be proven wrong. The Reserve Bank will be stopped out before the OCR hits such extreme levels.

Otherwise the Australian economy will face a nasty recession that will cause the Reserve Bank to slam into reverse and sharply cut rates – much like it did during the GFC when it wrongly tightened monetary policy into the global recession.