This week has seen two Big Four New Zealand banks – ANZ and ASB – hike their forecasts for the official cash rate (OCR). This followed Monday’s 32-year high inflation print of 7.3%.

ANZ now sees the OCR peaking at 4% by the end of this year, up from their previous high forecast of 3.5%. ASB now sees a 3.75% OCR peak by the end of the year, up from 3.5% previously.

Both forecasts are more aggressive than the Reserve Bank’s ‘forward track’ guidance, which tipped the OCR to peak at 3.9% by September 2023.

Rodney Dickens from Strategic Risk Analysis believes New Zealand mortgage rates would hit 7% under the banks’ OCR forecasts, which would represent a record increase and risks driving the nation into recession:

Advertisement

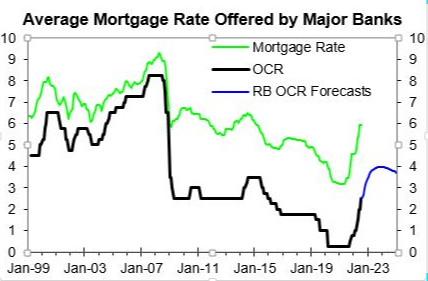

In the last 16 months the average rate has increased from a low of 3.2% to 5.9% currently, an increase of 2.7 percentage points. If the average rate increased to 7% it would be a 3.8 percentage point rise…

In terms of interest costs faced by borrowers there has already been an 84% increase based on the average mortgage rate in just 16 months versus a 47% rise in almost five years during the last inflation battle. And if the average rate were to rise to 7%, it would be a 119% increase in mortgage interest costs…

The Reserve Bank and bank economists are way off the mark in assessing the fallout from the OCR hikes delivered already…

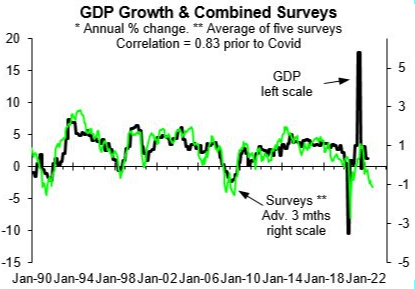

None of the bank economists predict anything close to a recession and the Reserve Bank predicts moderate growth in residential building activity despite it being highly sensitive to interest rates. By contrast, the first chart below shows a combined business and consumer survey that predicts an imminent recession or fall in GDP…

The outlook for GDP growth is dramatically worse than the Reserve Bank and bank economists predict, as should be no surprise given the scale of the increase in interest rates so far…

In an extremely short period interest costs have risen dramatically more already than was needed to cool inflation last time. Considering this and it taking up to two years for changes in interest rates to impact on inflation, sound judgement points to a need to wait to see what impact the largest increase in interest costs on record will have rather than charge ahead with even more aggressive OCR hikes.

Given the majority of Kiwi borrowers have fixed rate mortgages, the impact of the Reserve Bank’s aggressive tightening is yet to be felt across New Zealand’s economy.

Accordingly, the Reserve Bank is at grave risk of tightening too far, crashing the housing market, household consumption, and the economy.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.