TD Securities has published an interesting report showing how soaring shelter costs have been one of the biggest drivers of US inflation this year:

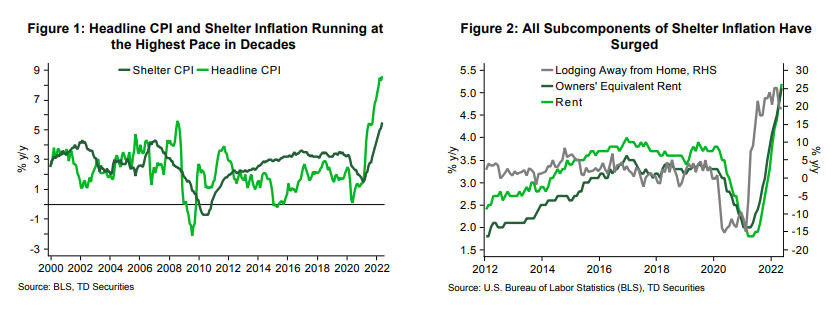

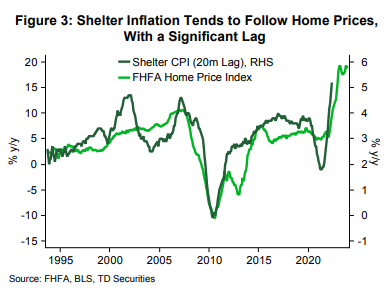

Rising shelter costs have been one of the biggest drivers of surging inflation this year. Shelter inflation was running at 3.4% y/y prior to the pandemic and decelerated to 2.7% y/y in mid-2021. However, shelter inflation is currently running at 5.5% y/y, which consists of rent inflation (5.2% y/y), owners equivalent rent or OER (5.1% y/y) and hotel prices (19.9% y/y). Note that rent, OER, and lodging away from home account for 22%, 74%, and 3%, respectively, in terms of their contributions to shelter inflation…

We forecast rent inflation to peak at about 6.2% y/y by January 2023 before moderating slightly during 2023 to finish the year at 5.1% y/y. OER should follow the surge in rents, peaking around 5.2% y/y in January and finishing 2023 at around 4.5% y/y…

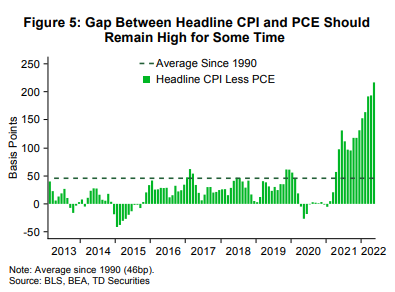

Our forecast should result in shelter inflation peaking at 5.8% y/y around early-2023 and moderating to about 4.9% y/y by the end of 2023. This will allow headline CPI to decline through the course of 2023, but note that shelter inflation will continue to run well above the pre-COVID trend. Given the high weight of shelter in headline CPI, this could keep inflation elevated and the Fed hawkish despite slowing growth momentum.

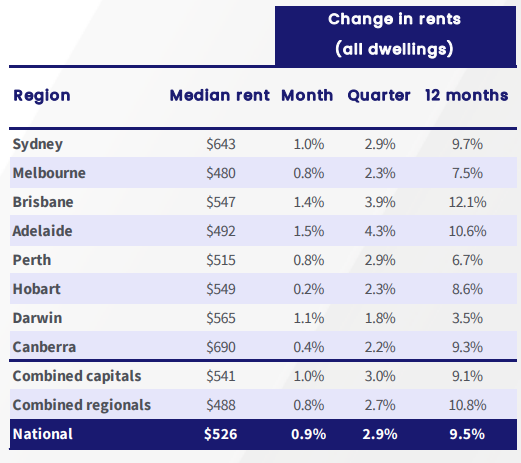

CoreLogic reported that Australian rents grew by 9.5% in the year to June 2022 – the highest rate of growth since December 2007 when Australia was importing a record number of migrants.

Rents soar across the nation.

Advertisement

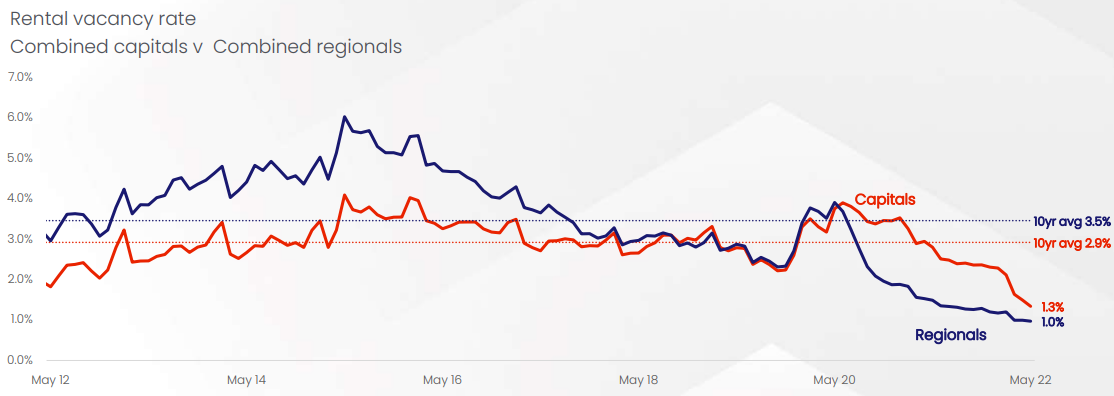

Vacancy rates have tanked to record lows, led by the regions, suggesting rents will continue to rise swiftly:

Rental vacancy rates at record lows.

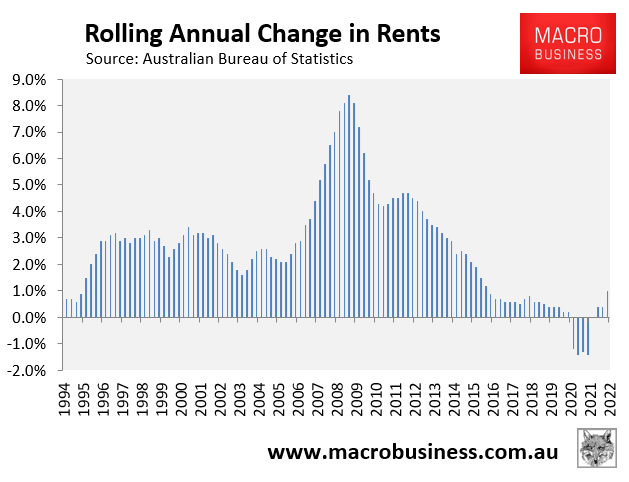

The surge in rents will soon have ramifications for inflation given the ABS’ rental series – measured as part of the CPI – rose by only 1.0% in the year to March 2022. This rental increase was less than one-fifth the rate of headline inflation (5.1%):

Advertisement

ABS is badly understating rental growth.

The ABS measures rents paid across the market, whereas CoreLogic and the other private data providers measure newly signed rents.

Thus, once the ABS updates its rental series with the actual market, rents will lift sharply and add to Australia’s inflationary pressures.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.