The ‘market’ is still deluded on Australian interest rates

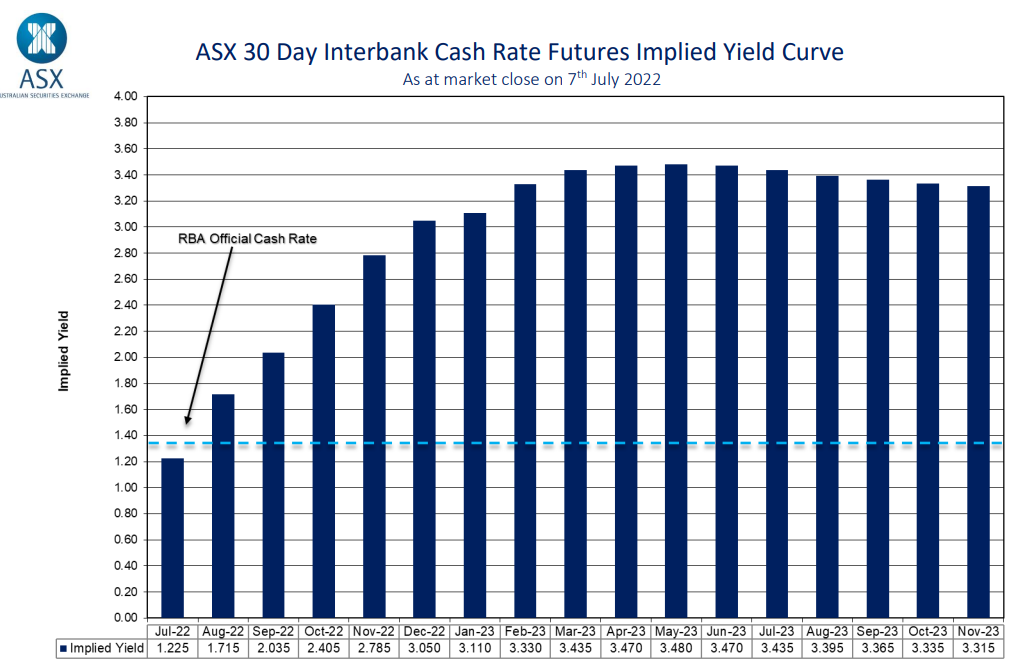

The futures market remains wildly bullish on Australian interest rates. At the close of business on Friday, the market was still tipping that Australia’s official cash rate (OCR) would peak at 3.5% in May 2023, before rate cuts push the OCR down to 3.3% by December 2023:

Still the fastest rise in rates in Australia’s history.

One month ago, the market forecast an OCR of 4.4% by May 2023 and has thus shaved 0.9% from its forecast.

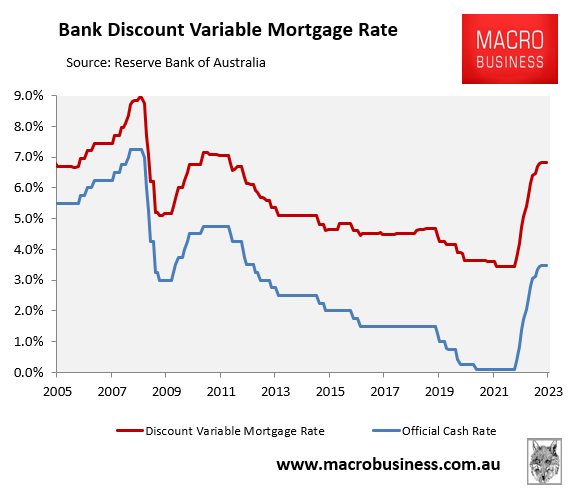

Nevertheless, if the market’s latest forecast comes to fruition, then Australia’s average discount variable mortgage rate would lift to 6.8% by May 2023, which would be nearly double its pre-tightening level of 3.45%:

Australian mortgage rates to double?

Like MB, the ABC’s business editor Ian Verrender believes the market’s OCR forecast is far too bullish and that they have “abandoned” a couple of basic principles “in their quest to frighten the living daylights out of everyone. And at the very top of that list is logic”.

First, Verrender notes that “Australia is uniquely vulnerable to an economic downturn from interest rate hikes” because unlike most other nations, “our mortgages are struck on variable rates” and “even our fixed rate loans are for relatively short terms”. This means that “interest rate movements directly impact Australian households more than many other countries”.

And because Australia’s mortgage debt load is among the very highest in the world, “the kind of rate hikes being bandied about by experts would hit the property market hard and potentially plunge the economy into recession”.

Second, Verrender notes that having mortgage rates soar above 6% would stymie household consumption, which drives around 60% of our economic growth. So, “if spending falls off a cliff, because of a rapid-fire lift in interest rates, we’ll tip into recession. And then we’ll have a much bigger problem”.

Third, Verrender argues that rate hikes hurt far more than they used to because of Australia’s record house prices and mortgage debt. “That huge valuation jump has been funded with debt, and — because we owe so much more than we once did — the effects of interest rate rises are magnified… As a result, our economy now is hypersensitive to interest rate movements”.

Fourth, Verrender notes that interest rates are a demand management tool. Therefore, they won’t do much to cure inflation, which is primarily supply driven. Moreover, inflation will resolve itself anyway as supply pressures ease (or at least don’t get any worse):

It’s likely the supply driven inflation problem will cure itself. Think of it this way. The price of carrots may have doubled in a month because of shortages. That’s 100 per cent inflation. However, if they stay at that higher price, then there’s no inflation.

The carrots are still expensive. But the price isn’t rising.

Finally, Verrender warns that excessive rate hikes risk plunging the economy into recession, which will likely force the RBA to cut rates next year:

If we keep driving rates higher at this pace, it may have limited impact on inflation and only serve to kill demand, thereby — unnecessarily — creating a recession…

And that leaves the RBA and its ilk with just two choices: Start dialling back the speed of rate hikes now or tip the economy into recession and be forced to start cutting next year.

The destination will be the same. Rates will be lower next year than many predict. How we get there is the unknown.

Regular readers will know that I too believe the market’s interest rate forecasts are delusional. The RBA will be stopped out long before the OCR hits the extreme levels forecast by the market.

Otherwise the Australian economy will be plunged into an unnecessary recession that will cause the RBA to slam into reverse and sharply cut rates next year – similar to the Global Financial Crisis when it wrongly tightened rates into the global recession.