Goldman has a crack at it. Like so much of its material, its market reading tools are brilliant but the analysis sucks. Global recession is the base case.

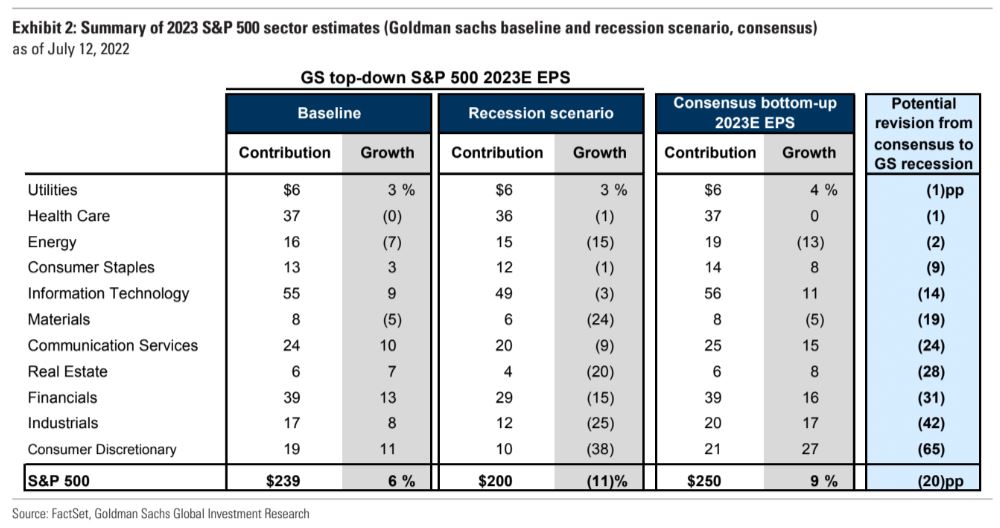

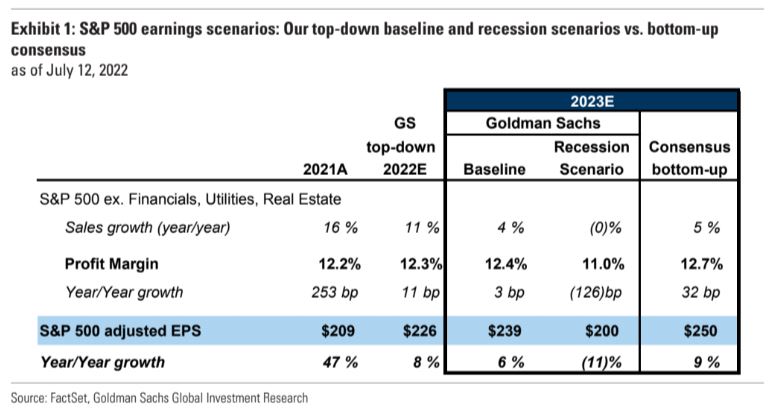

In this note, we quantify the downside risks to consensus 2023 EPS estimates. Last week we published a recessionary EPS scenario for the S&P 500 index as well as the 11 sectors. In addition, several of our single stock equity research analysts have recently published recessionary EPS scenarios for their covered companies. The baseline GS Economicsforecastassigns just a 30% probability that the US economy enters a recession during the next year. However, if a recession materializes, the potential negative revisions to consensus EPS estimates would be substantial. If the consensus bottom-up EPS estimate converges to our top-down recession profit forecast it would represent a 20 percentage point (pp) cut to 2023 growth (from +9% to -11%).

At the sector level, the reduction in EPS growth would range from -1 pp (Utilities) to -65 pp (Consumer Discretionary). At the stock level, the range of potential revisions from current consensus to our analysts’ downside EPS estimates is extremely wide. Six of our single stock analysts recently published downside 2023 earnings scenarios for their covered companies. The average potential negative EPS revision was 33% and the expected growth rate declined by 39 pp (+10% to -29%). These analysts included: Jordan Alliger (Transportation), Emily Chieng (Metals & Mining), Mark Delaney (Autos &Industrial Tech), Rod Hall (Tech Hardware), Susan Maklari (Building Products), and Richard Ramsden (Banks). Three of our single stock analysts now incorporate a potential economic downside scenario in their 2023 EPS forecasts. Our Energy analyst Neil Mehta (Oil & Gas – E&P) actually raised estimates by an average of 11% following our commodities team’s upgraded oil price forecasts. The expected EPS growth across Energy stocks increased by 12 pp (+11% to +23%). In contrast, Joe Ritchie (Multi-Industry) and Eric Sheridan (Internet) showed an average hit of 5% to the level of 2023 EPS and reduced expected 2023 growth rates by 4 pp.