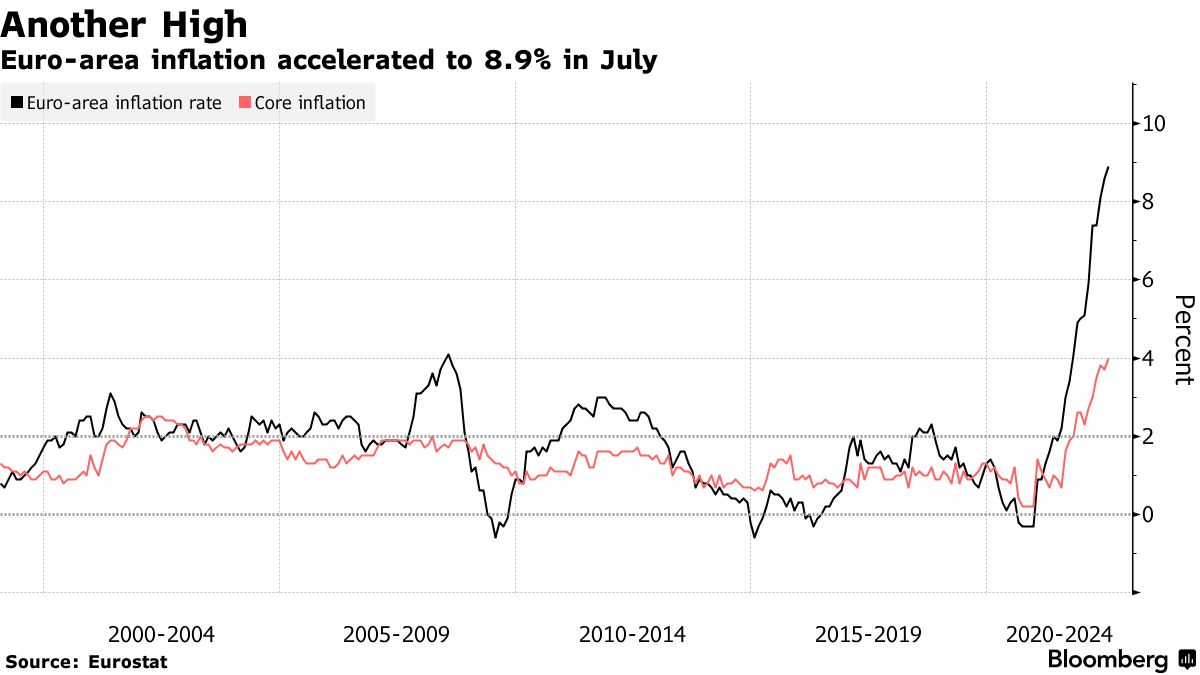

Friday evening printed two nasty inflation outcomes. Europe is still getting worse:

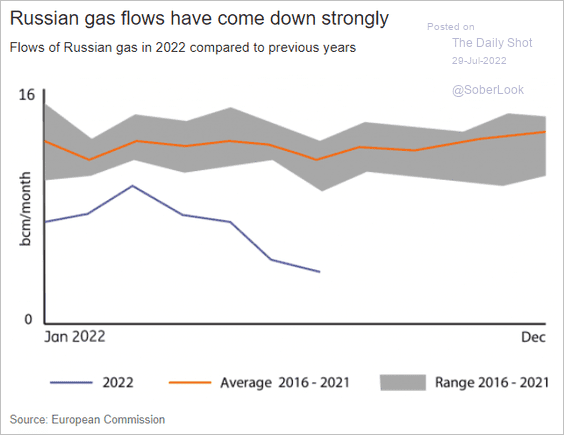

With winter approaching, markets really need to ask if they want to bet on Vladimir Putin’s generosity:

Advertisement

Given his supply to Europe is already stuffed long-term why wouldn’t go for a little scorched earth on the way out? Surely this make EUR investable.

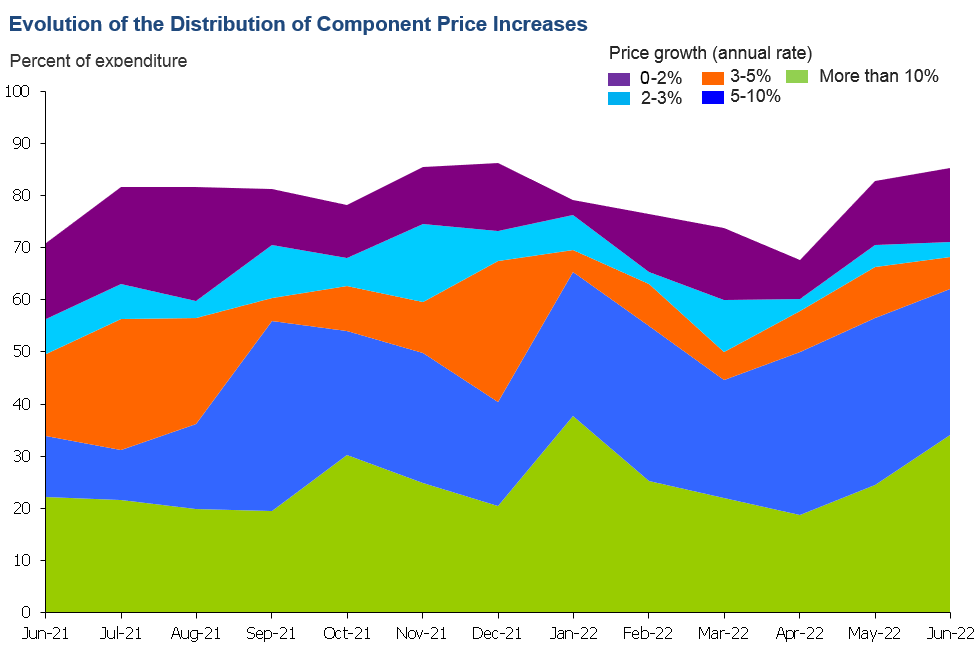

Second, the Fed’s preferred inflation measure, PCE, came in much stronger than expected. Goldman:

Advertisement

The June core PCE price index rose by 0.59% month-over-month, above consensus expectations, and the year-over-year rate increased to 4.79%. Personal income and spending both increased a bit more than expected, and the saving rate dropped to 5.1% in June. The Employment Cost Index rose 1.3% in Q2(not annualized), with firm underlying details. Our composition-corrected wage tracker stands at +5.5% year-over-year in Q2 (vs. +5.4% in Q1), and our quarterly annualized composition-corrected wage tracker based on average hourly earnings and the Employment Cost Index stands at +5.3% in Q2 (vs. +5.6% in Q1).

The notion that the Fed is about to pivot strongly and reflate everything with oil above $100 and PCE still rising strikes me as wishful thinking.

The Fed turned data dependent this week and the data is unequivocal. Its job is not done.

Advertisement

The AUD short squeeze has been fueled by falling yields. Beware.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.