By Gareth Aird, head of Australian economics at CBA:

Key Points:

- We maintain our central scenario that national home prices will fall ~15% peak to trough, but that forecast is now expected to be realised sooner.

- We expect national dwelling prices to reach a floor in mid-2023 before gradually rising over the second half of 2023.

- Our forecasts for home prices are conditional on a peak in the cash rate of ~2.60% (to be reached in late 2022) and two 25bp interest rate cuts in H2 2023.

Overview

In early June we published updated home price forecasts following the RBA’s 50bp June rate hike. Prior to that forecast revision we had expected the RBA to tighten policy in ‘business as usual’ 25bp moves. But the 50bp rate hike signalled that the RBA would front load their tightening cycle, which would have implications for home prices.

In June we wrote, “we expect home price falls nationally of ~15% over the next eighteen months. Prices in Sydney and Melbourne are anticipated to decline by more than the other capital cities. The expected falls in home prices are significant. But context is key. Price gains in 2021 nationally were extraordinary. And therefore a contraction in dwelling prices is a natural response to rising interest rates given it was record low interest rates that drove the phenomenal lift in prices in 2021.”

We have not changed our expectation that national dwelling prices will fall from peak to trough by ~15%. But we now see that trough reached sooner given prices are falling at a slightly quicker pace than we anticipated. Our expectation that the RBA cuts the cash rate by 50bp in H2 2023 sees home prices rise modestly on our central scenario over late 2023. In summary we have essentially modified our forecast profile for home prices rather than changed the overall message.

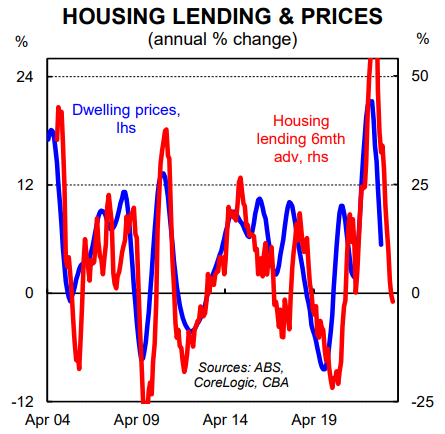

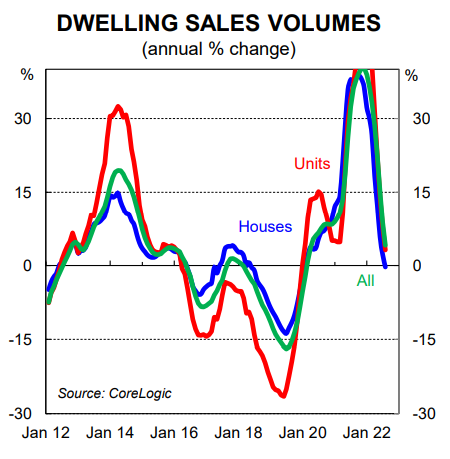

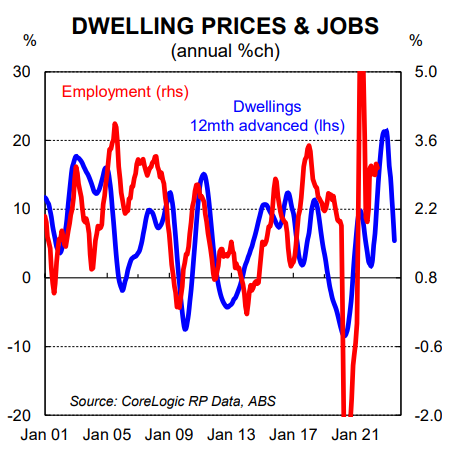

The historical lags between changes in the cash rate and the impact on home prices have shortened over the past five years. The current RBA tightening cycle is a case in point. The peak in home prices nationally was in April 2022. Dwelling prices began their descent as soon as the RBA commenced normalising the cash rate the following month in May.

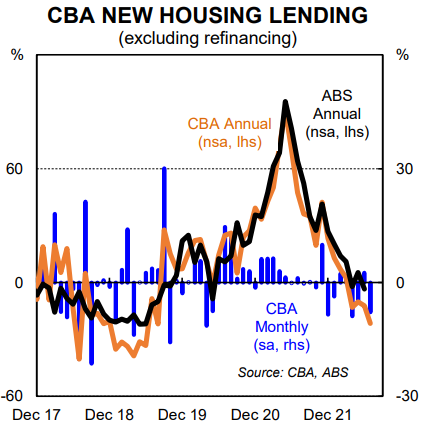

The rapid pace of RBA tightening has had an almost immediate impact on the demand for credit and by extension home prices (see facing charts). The upshot is that national dwelling prices are currently falling at a swift pace. That picture is not anticipated to change in the near term as the RBA continues to raise the cash rate.

Our central scenario sees the RBA deliver a further 75bps of rate hikes over coming months and for the cash rate to peak at 2.60% (the risks sits with a higher terminal rate of ~2.85%). As such, our home price forecasts are conditional on a cash rate peak of 2.60%. We would anticipate a larger fall in dwelling prices if the RBA takes the cash rate higher than our terminal rate forecast.

Recent data

Corelogic data indicates that home prices nationally fell by 1.4% in July and will likely be down by 1.5% in August (8 capital city benchmark index). Such an outcome would see dwelling prices down by 4.0% from their peak in April 2022.

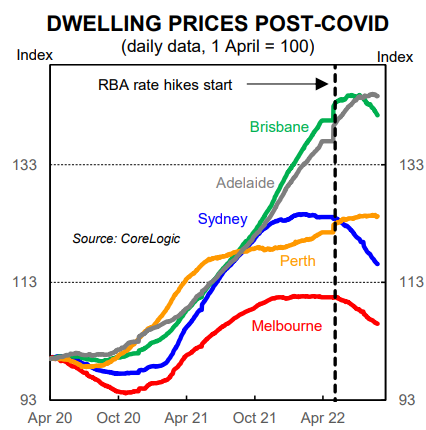

Outcomes are divergent across the country. Home prices are sliding quickly in the major capital cities on the east coast. Sydney dwelling prices are likely to post a second consecutive monthly fall of a little over 2% in August which would take the cumulative fall since the peak in January 2022 to 7.0%.

Prices in Melbourne look set to fall by 1.3% in August which would take prices down by 5.0% since their peak earlier this year. Brisbane dwelling prices have recently turned down having risen earlier this year. Brisbane property prices look set to post a sizeable fall of 1.7% in August.

Dwelling prices in Adelaide and Perth are so far holding up but momentum is clearly slowing. Corelogic daily data suggests home prices have crabbed sideways in Adelaide and Perth over August. We expect prices to decline in those markets from here as higher interest rates further dampens the demand for

housing credit and in turn price expectations and outcomes adjust downwards.

Falling property prices across our three largest capital cities is not surprising given the rapid pace of RBA tightening and the big lift in home prices over 2021. But the recent pace of price falls is likely to cause some angst for policymakers if they persist for too long.

The RBA does not target dwelling prices and they have made that explicitly clear. But home prices cannot be divorced from the broader economy and changes in home prices influence the economic outlook. Indeed they are a forward looking indicator (changes in home prices impact wealth, consumer confidence, spending decisions and employment). Housing turnover also impacts spending and price outcomes and turnover are positively correlated. More turnover in the housing market means more spending on household goods, all else equal. The reverse is also true. The RBA will be monitoring activity in the housing market closely for these reasons.

Outlook

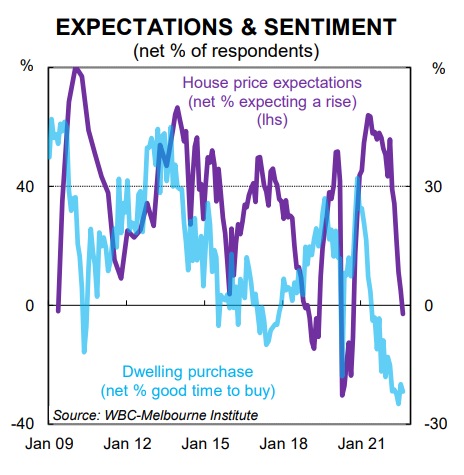

Dwelling prices nationally will continue their downward trend over 2022 as the impact of higher interest rates weighs on borrowing capacity. The Melbourne Institute/WBC ‘time to buy a dwelling’ index sits at a very low level, while the ‘house price expectations index’ has collapsed over the past few months (see facing chart).

In many parts of Australia the housing market has swung from FOMO (fear of missing out) in 2021 to FOGI (fear of getting in). That dynamic of course does not last indefinitely and prices will stabilise and rebound at some stage. But we are not there yet given the RBA is broadly expected to continue to raise the cash rate, which means standard variable mortgage rates have further to lift.

It is worth noting that CBA’s expectation for the cash rate to peak at 2.60% is one of the most conservative amongst the forecasting community. And our call for the RBA to cut the cash rate by 50bp in H2 2023 is also a non-consensus call.

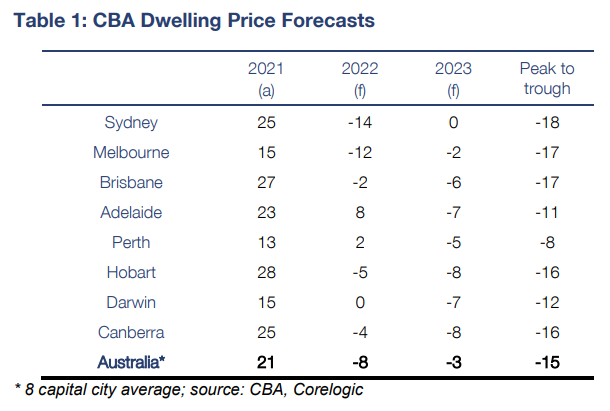

Table 1 below contains our updated home price forecasts by capital city. We expect the largest peak to trough fall to be in Sydney (a fall of ~18% is anticipated; unchanged from our previously published view in June). Broadly similar peak to trough falls are forecast for Melbourne and Brisbane, albeit

Brisbane prices rose much more strongly than Melbourne over the past two years so the correction is not as large in that context. We expect Perth to be the best performing market through this correction phase and to have the smallest peak to trough fall.

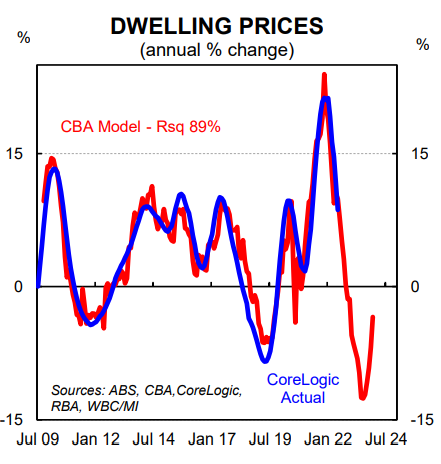

Forecasting is not an exact science and all models have limitations. As such we encourage readers to focus on our message around the housing market rather than our point estimates.

Our narrative is quite simple on the housing front. RBA policy decisions from here will drive the demand for credit, which in turn will influence home price outcomes. Dwelling prices will continue to slide in the short run, but if the RBA takes the cash rate lower in H2 2023 as per our forecast then home prices are likely to rise. We expect the Sydney and Melbourne housing markets to be the most responsive initially to RBA rate cuts given they were the first to enter their correction phase.

Our view that the RBA will cut the cash rate in H2 2023 is largely based on our estimate of the neutral rate which we put at ~1.50% (~100bp lower than the RBA’s estimate of 2.50%). We expect the cash rate to sit in contractionary territory for around a year, which would generate below trend GDP growth and an increase in the unemployment rate. We expect the inflationary impulse to slow next year and that will allow the RBA to ease policy to support the economy on our forecast profile in H2 2023 (note we expect inflation to return to the top of the RBA’s 2-3% target band by late 2023).