Goldman Sachs has identified Australia’s housing market collapse as the “single greatest domestic downside risk to Australia’s macro outlook”, given household consumption and dwelling construction are key drivers of growth.

Alongside other economists, they warn that Australia’s slumping housing market could plunge the economy into recession:

Andrew Boak, Goldman chief economist for Australia, sees a 15-20% peak-to-trough decline in house prices as construction insolvencies become “more widespread”… [Home building] insolvencies have jumped 70% in the year to June, Goldman Sachs Group Inc. says…

“The housing cycle is the single greatest domestic downside risk to Australia’s macro outlook,” Boak says. “The outlook is uncertain and pressures on the building cycle and house prices warrant close monitoring”…

Eleanor Creagh, a senior economist at real estate advertiser REA, says if prices fall by 20% or more it will be “like a sigma event. It’s something that has never occurred before”…

The risk is a vicious cycle emerges from households cutting spending and property prices falling together with rates rising and inflation quickening. That could see unemployment rise, spark forced home sales and see the economy contract…

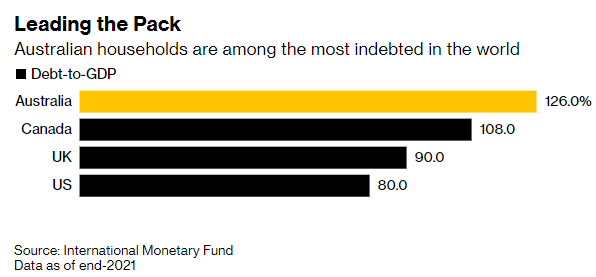

“Australia is quite an exposed market in the world in the sense that household credit and mortgage debt as a share of GDP ranks quite high,” said Louis Kuijs, chief Asia economist for S&P Global Ratings. “There’s a lot of debt out there. The higher the debt-to-GDP, the more the rate channel starts to matter”…

The RBA’s hikes have added about A$690 a month to repayments on an average A$767,000 mortgage, according to Diana Mousina of AMP Capital Markets…

“A good rule of thumb is that every percentage point increase in the cash rate would reduce house prices by about 8%,” said Peter Tulip, chief economist at the Centre for Independent Studies and a former senior member of the RBA’s economic research department.

“So suppose we get a 3 percentage point increase in the cash rate, that would translate to a 24% reduction”…

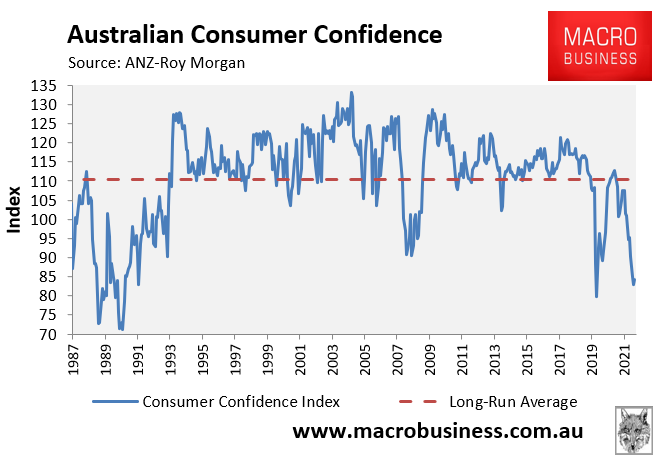

Outside of the pandemic, Australian consumer confidence is tracking around its lowest level since the early 1990s recession, way below the trough experienced during the Global Financial Crisis in 2008:

Advertisement

Australia’s consumer confidence is tracking near recessionary levels.

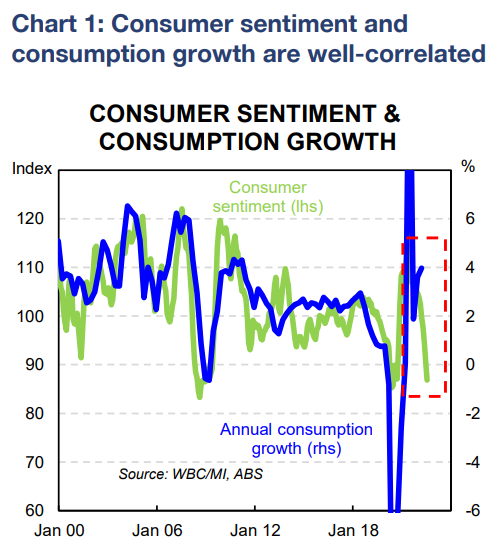

Household confidence/sentiment has traditionally been a leading indicator for household consumption, suggesting spending will soon fall sharply:

Confidence generally leads consumption spending.

Advertisement

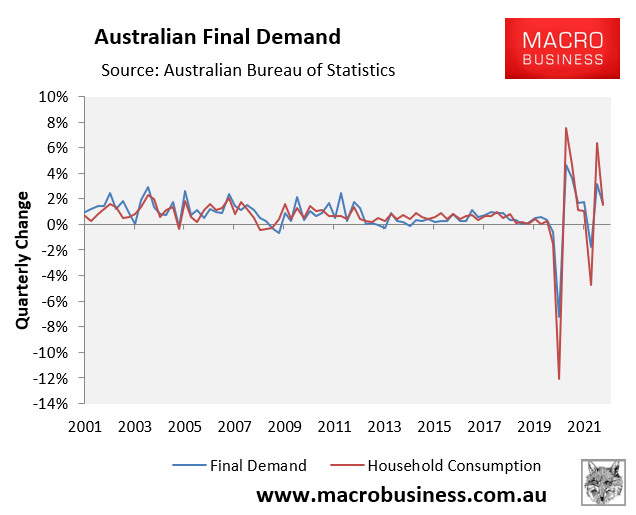

This is important because household consumption is the engine room of the Australian economy, accounting for 55% of growth in a typical quarter. Thus, where household consumption goes the economy usually follows:

Household consumption generally drives economic growth.

So, as mortgage repayments soar on the back of rate hikes, there will be less funds available for spending across the Australian economy. This will drain economic growth.

Advertisement

The negative drag on household consumption will be exacerbated by the sharp fall in house prices, which will make Australians feel poorer.

Add to that a projected sharp fall in dwelling construction levels, and you have the ingredients for a recession.

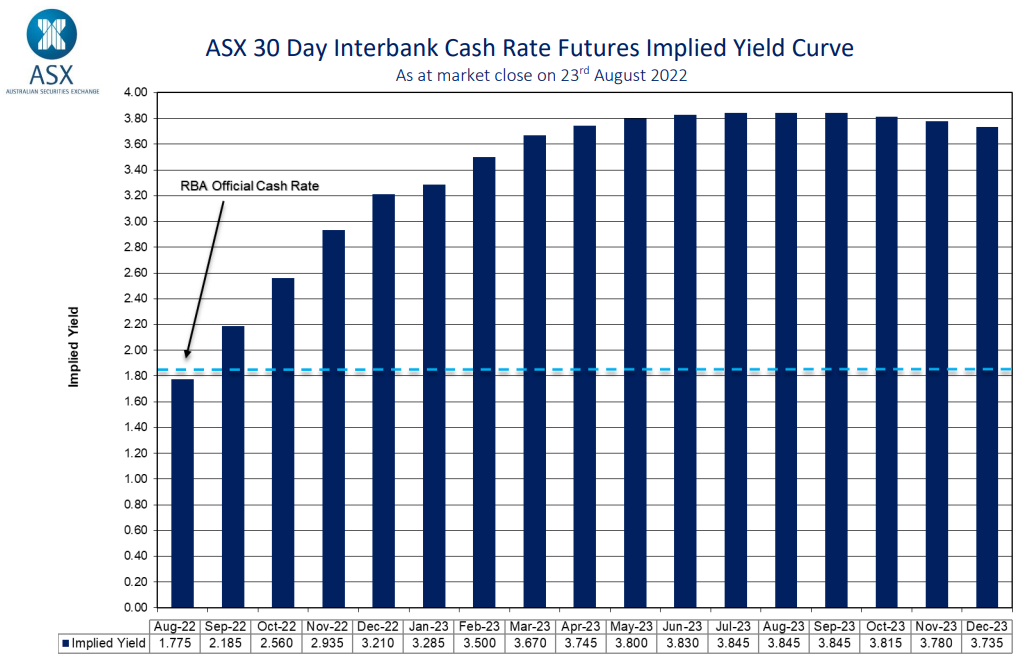

Futures market: Official cash rate to peak at 3.85%.

Advertisement

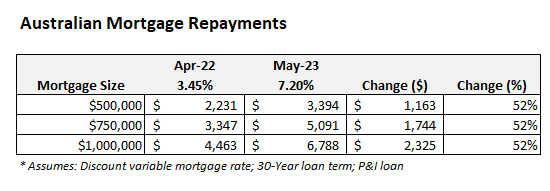

Ultimately, whether Australia plunges into recession depends largely on how high the RBA hikes interest rates. For example, if it follows the lead of the futures market, and hikes the official cash rate to 3.85% (implying a discount variable mortgage rate of 7.2%), then mortgage repayments will soar to obscene levels (see below table) and house prices will likely crash.

Futures market: Mortgage repayments to soar 52% above their pre-tightening level.

If that happens, then a recession is likely for the Australian economy. Hopefully the RBA will stop hiking long before that point.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.