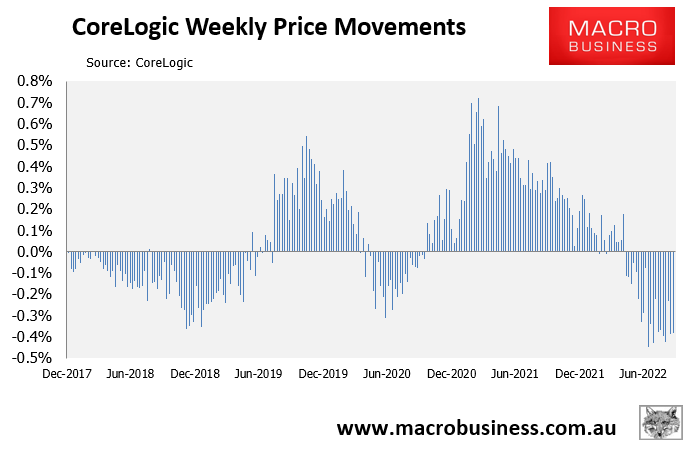

CoreLogic’s daily dwelling values index, which measures value changes across Australia’s five major capital cities, fell another 0.38% in the week ended 22 September. It was the 20th consecutive weekly price fall:

20th weekly price fall at the 5-City level.

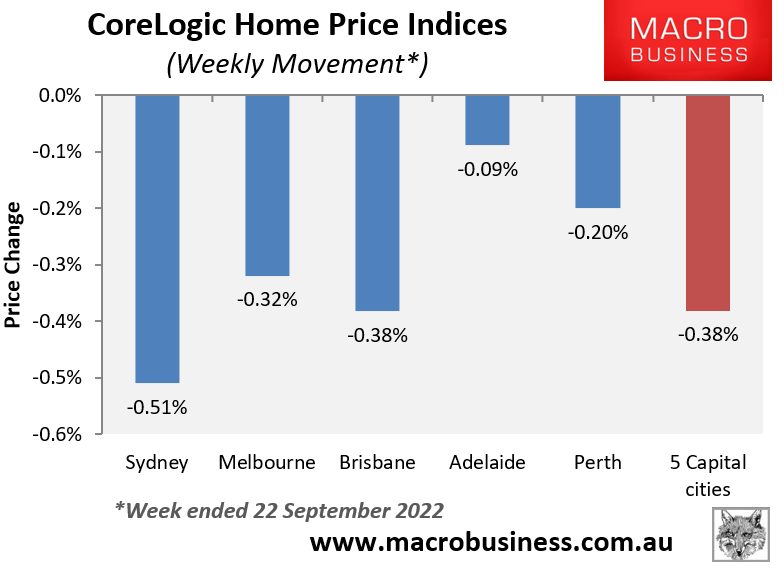

Every major Australian capital city recording falling values over the week, with Sydney once again leading the way:

Coast to coast house price falls.

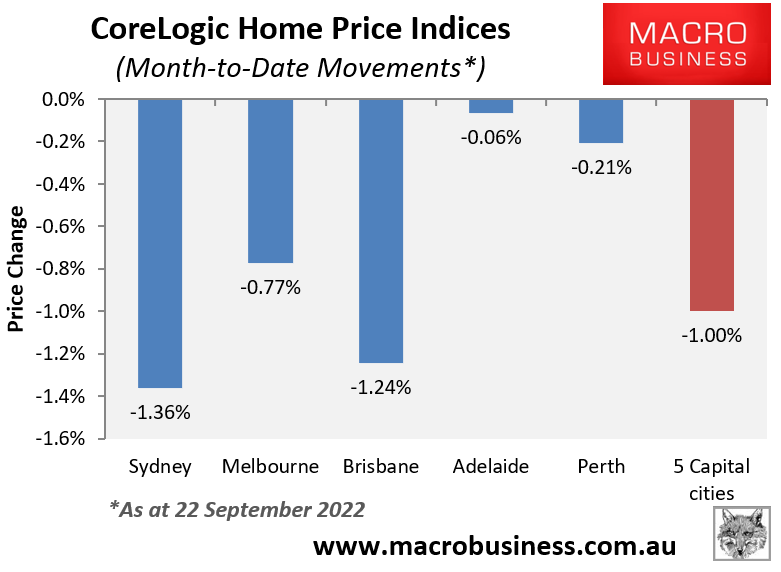

So far in September, dwelling values have fallen 1.0% at the 5-City aggregate level. Sydney (-1.36%), Brisbane (-1.24%) and Melbourne (-0.77%) have each registered significant price falls, whereas prices have fallen more modestly across Perth (-0.21%) and Adelaide (-0.06%):

The ‘Big three’ lead house price falls in September.

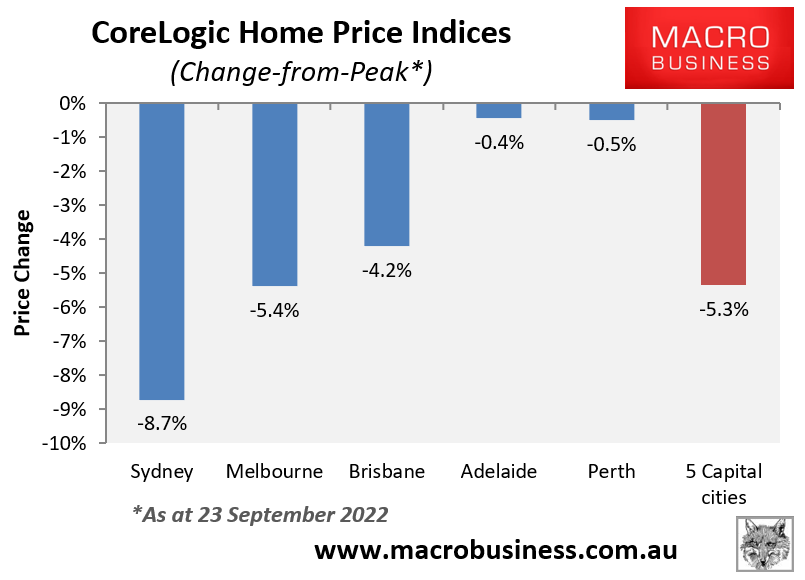

The declines from peak are shown in the next chart. Dwelling values have fallen by 5.3% at the 5-City aggregate level. Sydney is leading the way, with dwelling values down a hefty 8.7% from their mid-February peak. Melbourne (-5.4%) and Brisbane (-4.2%) have also suffered solid losses. By contrast, Perth (-0.5%) and Adelaide (-0.4%) have only recently joined the correction:

The larger the city, the larger the housing correction.

The correction has a long way to run given this month’s monetary policy statement from the Reserve Bank of Australia (RBA) stated that “the Board expects to increase interest rates further over the months ahead”.

Since there is a two to three-month lag between interest rate increases and their impacts on mortgage holders and the economy, Australian dwelling values should continue to fall at a swift pace.

CoreLogic’s records dating back to 1980 show that Australian capital city dwelling values have never declined by more than 11% peak-to-trough.

This record looks certain to be smashed in the next six months as the lagged impact of the RBA’s aggressive interest rate hikes, let alone further increases, take effect.

The upswing probably won’t arrive until the second half of 2023 after the RBA begins cutting rates to ward off recession. Then we will be off to the races again.