CBA: RBA “flying blind” with aggressive rate hikes

By Gareth Aird, head of Australian economics at CBA:

Key Points:

- Home borrowers have barely felt the impact of the RBA’s rapid 175bp of tightening since 4 May from a cash flow perspective.

- There is on average a three-month lag between an RBA rate hike and when CBA borrowers on variable rate mortgages experience an increase in their home loan repayments.

- The lag largely explains why the official spending data has remained strong, but consumer sentiment sits at levels associated with a recession or major negative economic shock.

- We expect consumer spending to slow materially as the lagged impact of rate hikes hits home borrower cash flow.

It is conventional wisdom that monetary policy works with a lag on demand and inflation. But less widely understood is the delay between an increase in the cash rate and the impact it has on home borrower cash flow.

The lag between an increase in the cash rate and the resultant upward adjustment in repayments for borrowers on variable rate home loans differs between lenders. But in general, the lags are longer than what would seem intuitive.

In a slow and elongated tightening cycle the lag between a change in the cash rate and the impact it has on borrower cash flow is less important. But a full appreciation and understanding of these lags is very important in a rapid and aggressive tightening cycle like the RBA has embarked on.

The RBA has put through an incredible amount of tightening in a short amount of time. The RBA increased the cash rate by 175bp between 4 May and 2August–over just three months. CBA and the consensus of economists expect the RBA to deliver another 50bp hike at the September Board meeting tomorrow (6/9). Such an outcome would mean the RBA has increased the cash rate by 225bp over just four months. A 50bp hike at the September Board meeting will take the cash rate to 2.35%-its highest level since 2015.

CBA is Australia’s biggest mortgage lender. Our mortgage book is ~25% of the total mortgage market. There is on average a three-month lag between an RBA rate hike and when CBA borrowers on standard variable rate mortgages experience an increase in their loans repayments. This means that the bulk of our borrowers have only felt the impact of one 25bp hike on their cash flow (or potentially as of this week the cumulative impact of the May 25bp rate hike and June 50bp rate increase).

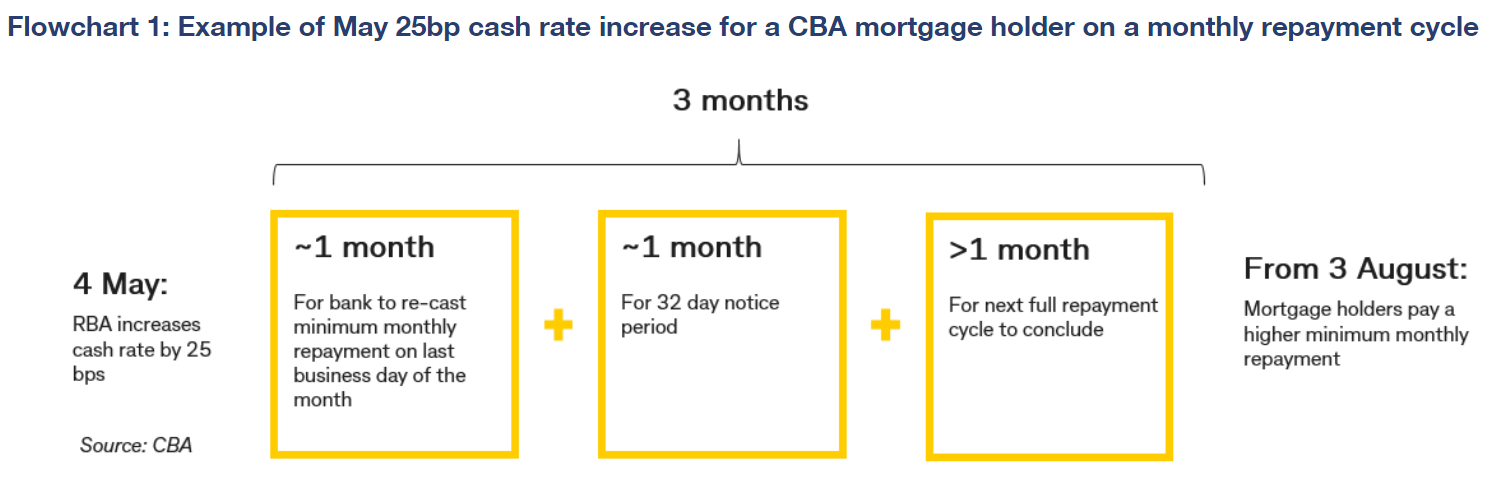

The flow chart below illustrates the delay in pass-through from the RBA’s first 25bp rate hike in May to a CBA borrower on a standard variable rate with a monthly repayment schedule (~75% of people).

Interest accrues from a lenders effective rate change date, which is typically ~2 weeks after the RBA increases the cash rate. This interest is added to a borrower’s outstanding debt. But from a cash flow perspective the impact is not felt for three months on average for a CBA customer.

The lags across other lenders vary. But we estimate that on average the lag is around two to three months across the major lenders (note that all home lenders must adhere to the National Credit Code).

The lag between rate hikes and the impact on cash flow helps to explain why consumer feelings and actions haven’t married up. Consumer sentiment sits at levels normally associated with a recession or negative economic shock. In contrast spending in the official data has been strong (latest is July ABS retail sales). But that is likely to change from here.

Many households with mortgages will need to adjust their spending patterns over the period ahead as the lagged impact of rate hikes negatively impacts their cash flow. Up until July most borrowers on floating rate mortgages had felt no impact from a cash flow perspective. This enabled them to continue to spend as they were previously, thus the official spending data has been strong.

The rapid pace at which the RBA has tightened policy, overlaid with a full appreciation of the lags between rate hikes and the cash flow impact on a home borrower, means there’s a degree to which the RBA Board is flying blind. It has simply been too early for the spending data to pick up the impact of the already delivered rate hikes. By extension this means it is also too early to see an impact of the rate hikes on labour market data, inflation or wages. But key tier 2 data, which contains a lot of forward-looking information, suggests the economy could slow quite materially from here, particularly given monetary policy is expected to be tightened further.

There is a clear risk that the RBA continues to tighten policy aggressively because it appears that demand in the economy is not slowing sufficiently to put the desired downward pressure on inflation. But that will occur in time as the rate hikes ‘kick in’. At CBA, for example, by December the impact of already announced rate rises on monthly cashflow for mortgage holders will be a four-fold increase compared to July.

Our base case sees the RBA raise the cash rate by 50bp to 2.35% at the September Board meeting tomorrow. We anticipate this will be the last 50bp hike. From there we expect one further rate hike of 25bp which would take the cash rate to 2.60% (around the RBA’s estimate of the neutral rate which is ~100bp above our estimate of neutral). The risks sits with a higher terminal rate of 2.85%.

We think that provided the RBA pauses for at least a few months in their tightening cycle when the cash rate is 2.60% or 2.85% the data will indicate that there is no need to continue to take the policy rate higher. Indeed, taking the cash rate higher would likely generate a hard landing in the economy.

Finally, were mind readers that there is a large proportion of fixed rate home loans that will expire over the next eighteen months. This creates natural tightening even with the RBA on hold (note that the average loan rate for a borrower rolling off a fixed rate loan over the next eighteen months is ~2.25%. This rate is significantly lower than the standard variable rate, which is likely to rise to 4.5-5.0% with a cash rate of 2.60%).

The Australian economy is largely in the RBA’s hands.