By Gareth Aird, head of Australian economics at CBA:

Key Points:

- The RBA will raise the cash rate at the September Board meeting. We expect another 50bp hike to 2.35%.

- The risks sits with a smaller increase (either 40bp or 25bp), but we consider that risk to be quite low.

- The Governor will deliver a speech on Thursday to the Anika Foundation on the Economic Outlook and Monetary Policy.

- The Governor is likely to reiterate that the RBA Board is “not on a pre-set path” and we expect the line to be maintained that the Board seeks to normalise monetary conditions in a way that “keeps the economy on an even keen”.

- There is a risk that the Governor hints that the pace of tightening could slow from next month (i.e. a further 50bp hike in October is not in their current plans, but rather a smaller hike).

- Inflation is elevated and the labour market is tight, but the forward looking indicators of the economy are slowing quickly and we expect further weakness in the data over the period ahead.

Another 50bp hike in September, but the policy outlook is complex The coming week is another big one for Australian financial market participants. There is the RBA September Board meeting on Tuesday. And on Thursday Governor Lowe delivers a speech to the Anika Foundation on the Economic

Outlook and Monetary Policy. A stack of domestic data will also be published, which includes the June quarter 2022 national accounts.

The rapid pace at which the RBA has tightened policy means there’s a degree to which the Board is flying blind. More specifically, it is too early for tier 1 economic data, which includes unemployment, inflation, wages and GDP, to pick up the impact of the already delivered rate hikes (recall that the RBA increased the cash rate by 175bp between 4 May and 2 August – over just three months). But key tier 2 data, which contains a lot of forward looking information, suggests the economy could slow quite materially from here, particularly given monetary policy is expected to be tightened further.

The crosscurrents in the domestic economic data released over the past month suggest the RBA has a tough task ahead as they seek to normalise monetary conditions in a way that “keeps the economy on an even keel”.

There is a case to be made to slow the pace of tightening at the September Board meeting and raise the cash rate by 25bp or 40bp. But we do not anticipate that outcome. Instead we expect the RBA to raise the cash rate by another 50bp next week, to 2.35%, which is the consensus call across the forecasting community.

We anticipate this will be the last 50bp rate hike by the RBA.

A recap of key data released over the past month

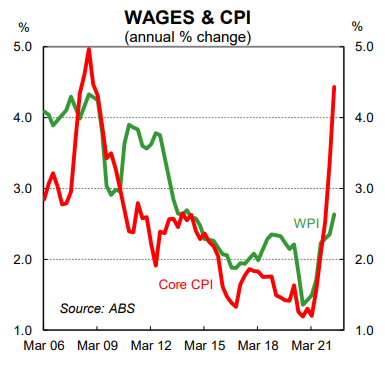

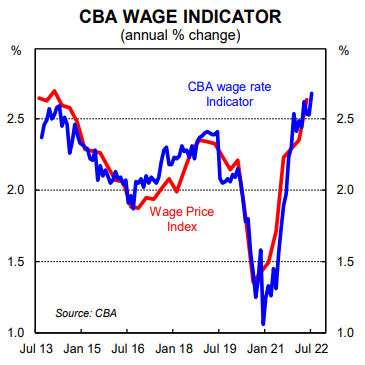

Wages growth continued to lift in Q2 22, albeit the pace of growth was modest. The Q2 22 WPI rose by 0.7% which took the annual rate to 2.6% (well below the ~3.5% level the RBA previously nominated that they consider consistent with inflation within the target band over the medium term). The RBA want wages growth up and inflation down – an unusual place for a central bank to find itself.

The July labour force survey was a mixed bag. Employment decreased by 41k over the month but the unemployment rate edged lower to 3.4% as the participation rate dropped sharply by 0.4ppts to 66.4%.

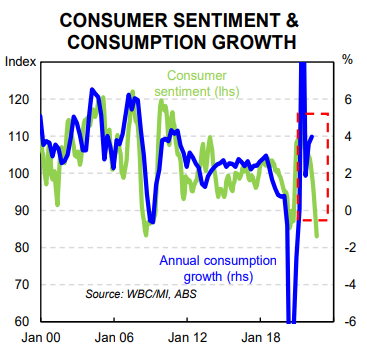

Retail trade rose by a strong 1.3%/mth in July, which implies the consumer is resilient. But in contrast the August WBC/MI consumer sentiment index printed at just 82.2 (a level normally associated with a major negative economic shock or recession).

The NAB July Business survey was reasonably strong. But the S&P Flash August PMIs, which are a timelier read on the private economy, indicated a contraction in business activity over August (the Flash Composite PMI fell to 49.8 in August).

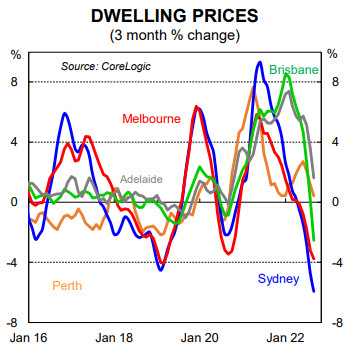

The pace of home price falls continued to accelerate in August. National dwelling prices, as measured by the Corelogic 8 capital city benchmark, fell by 1.6% in August and turnover further slowed. The housing market is probably not on the RBA’s radar at this juncture. But it will be soon. The RBA does not target dwelling prices and they have made that explicitly clear. But home prices cannot be divorced from the broader economy and changes in home prices influence the economic outlook. Indeed they are a forward looking indicator (changes in home prices impact wealth, consumer confidence, spending decisions and employment). Housing turnover also impacts spending and price outcomes as turnover and consumption are positively correlated. Less turnover in the housing market means less spending on household goods, all else equal.

Other housing-related data was weak over the past month. Building approvals, which are highly volatile month-to-month, slumped by 17.7%. Residential construction was down significantly in Q2 22 and will be a drag on the economy from here. New lending for housing excluding refinancing collapsed by 8.5% in July.

Capex intentions remained solid for 2022/23 and indicate businesses as a collective are optimistic on the economic outlook. There is a risk that some capex plans are shelved or put on hold if demand in the economy slows too quickly. It is worth noting an increase in business investment adds to demand in the short run (and inflation) but in the long run boosts supply (downward pressure on inflation).

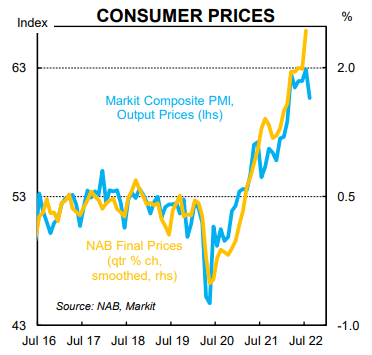

Inflation gauges in various private surveys over the past month indicate the inflationary pulse remained strong in Q3 22. But that should come as no surprise. RBA policy tightening to date has had no time to impact price changes in the economy.

The RBA Board decision and outlook

The RBA Board will have all of this economic information on hand when they meet on Tuesday 6 September. And the recent hawkish speech by US Fed Chair Jerome Powell, delivered at Jackson Hole, might well feed into the Board’s thinking on the outlook for monetary policy in Australia.

On the one hand the Board may feel that the US Federal Reserve will do some of the heavy lifting on the inflation front by putting downward pressure on US demand and in turn aggregate global demand and tradables inflation. But on the other hand Powell’s rhetoric may mean the Board feels a greater sense of urgency to bring down inflation. This would raise the risk that the RBA continue for a little longer with aggressive 50bp rate hikes (note this is not our base case and we do not believe the RBA need to go down this path).

The Australian economy is not in the same place as the US economy presently. We do not have a “wage-price spiral” and both inflation and wages growth are running at materially lower levels than in the US. We also have a much more leveraged household sector than the US and a much more direct and potent transmission mechanism from the policy rate to home borrowers given the structure of our mortgage market. Finally the RBA have a higher inflation target of 2-3% than the Fed’s target of 2%.

Our base case sees the RBA raise the cash rate by 50bp to 2.35% at the September Board meeting. We anticipate this will be the last 50bp hike. From there we expect one further rate hike of 25bp which would take the cash rate to 2.60% (around the RBA’s estimate of the neutral rate which is ~100bp above our

estimate of neutral). The risks sits with a higher terminal rate of 2.85%.

We think that provided the RBA pause for at least a few months in their tightening cycle when the cash rate is 2.60% or 2.85% the data will indicate that there is no need to continue to take the policy rate higher. Indeed taking the cash rate higher would likely generate a hard landing in the economy.

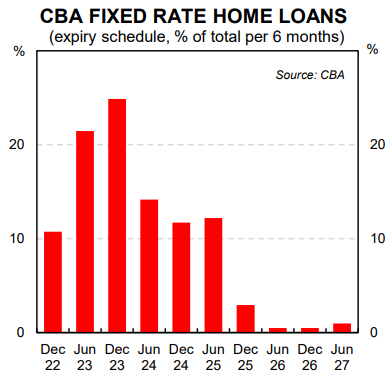

There is a large proportion of fixed rate home loans that will expire over the next eighteen months. This creates natural tightening even with the RBA on hold (note that the average loan rate for a borrower rolling off a fixed rate loan over the next eighteen months is ~2.25%. This rate is significantly lower than the standard variable rate, which is likely to rise to 4.5-5.0% with a cash rate of 2.60%).

Finally we note and recognise that consumer feelings and actions don’t currently marry up. But we believe that is explained in large part by the lag between changes in the cash rate and the impact it has on monthly cash flow for borrowers on a floating rate mortgage. At CBA, for example, there is on average

a three month lag between RBA rate hikes and when a borrower on a minimum mortgage repayment schedule experiences an increase in their mortgage payment.

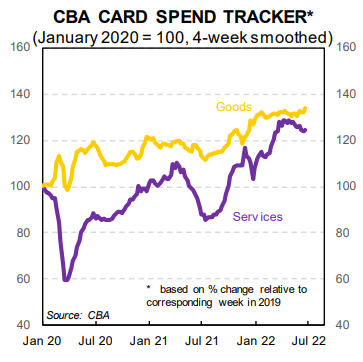

Our timelier CBA Credit & debit card spending data suggests nominal spending across the economy flat-lined in August (the implication is the volume of spending contracted). Consumption is expected to further weaken as the lagged impact of rate hikes impacts aggregate demand.

The Australian economy is largely in the RBA’s hands.