The bizarrely silent Chinese crash of the century rolls on today. Societe General has a few charts.

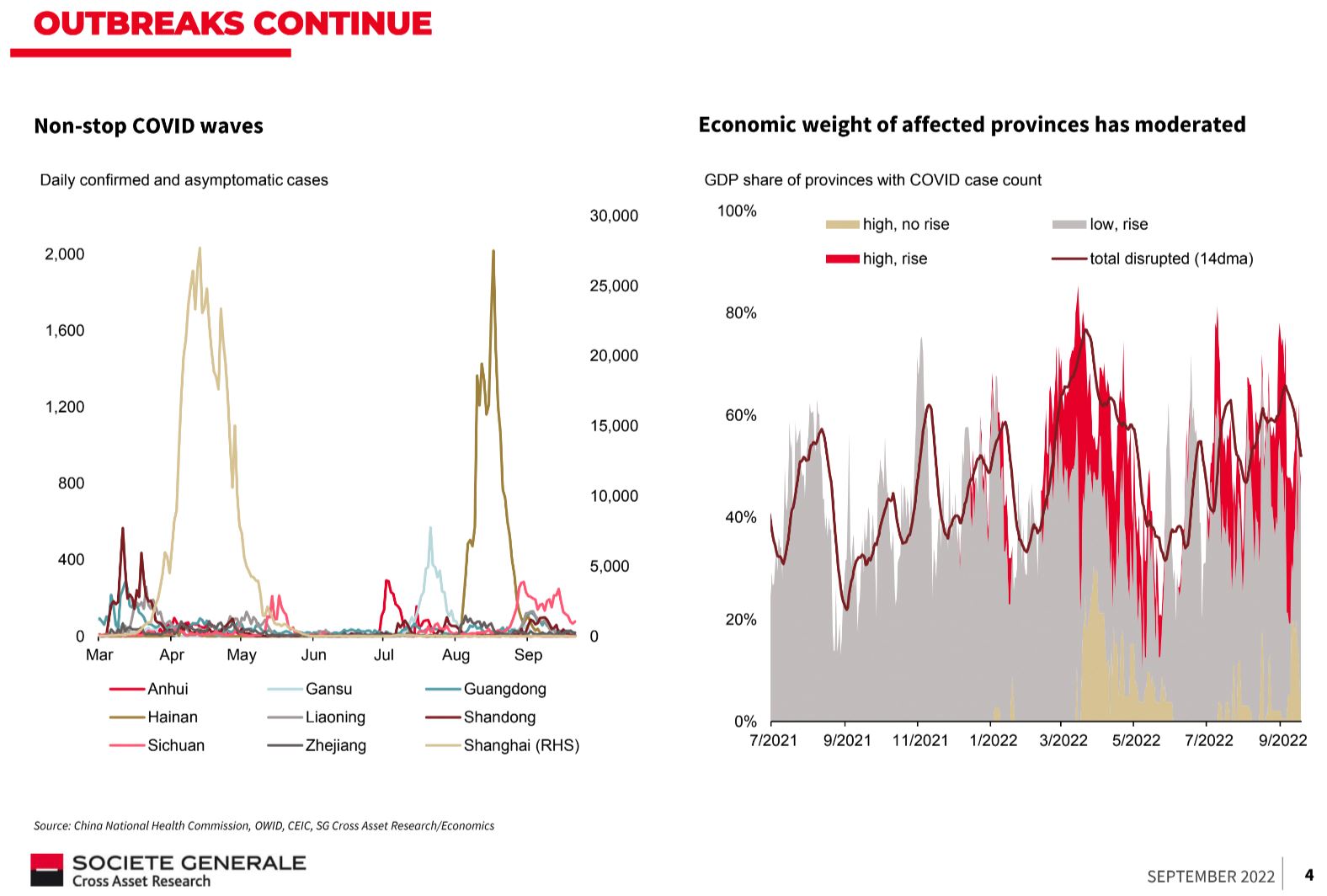

Zero-COVID remains:

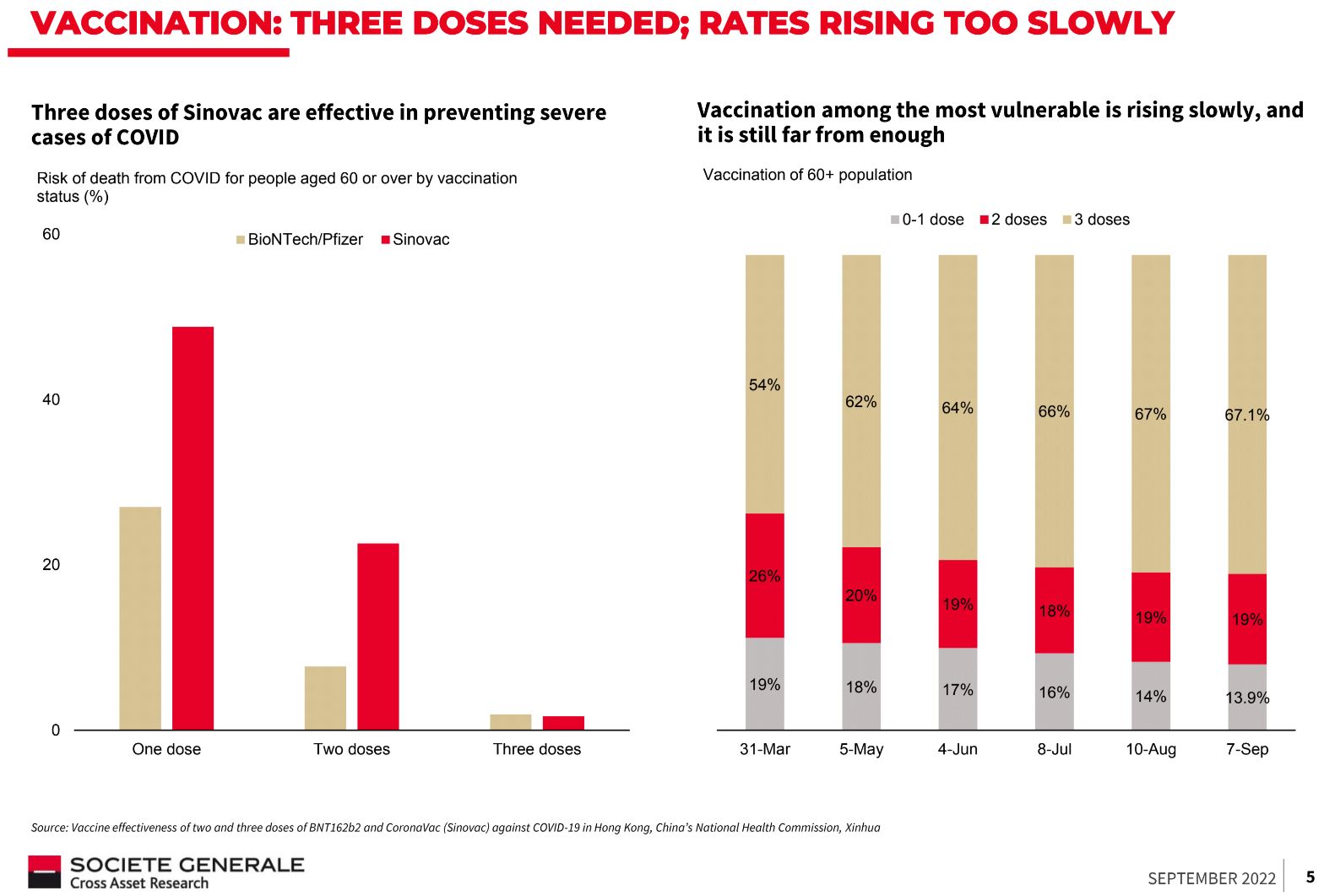

No progress in vaccinations:

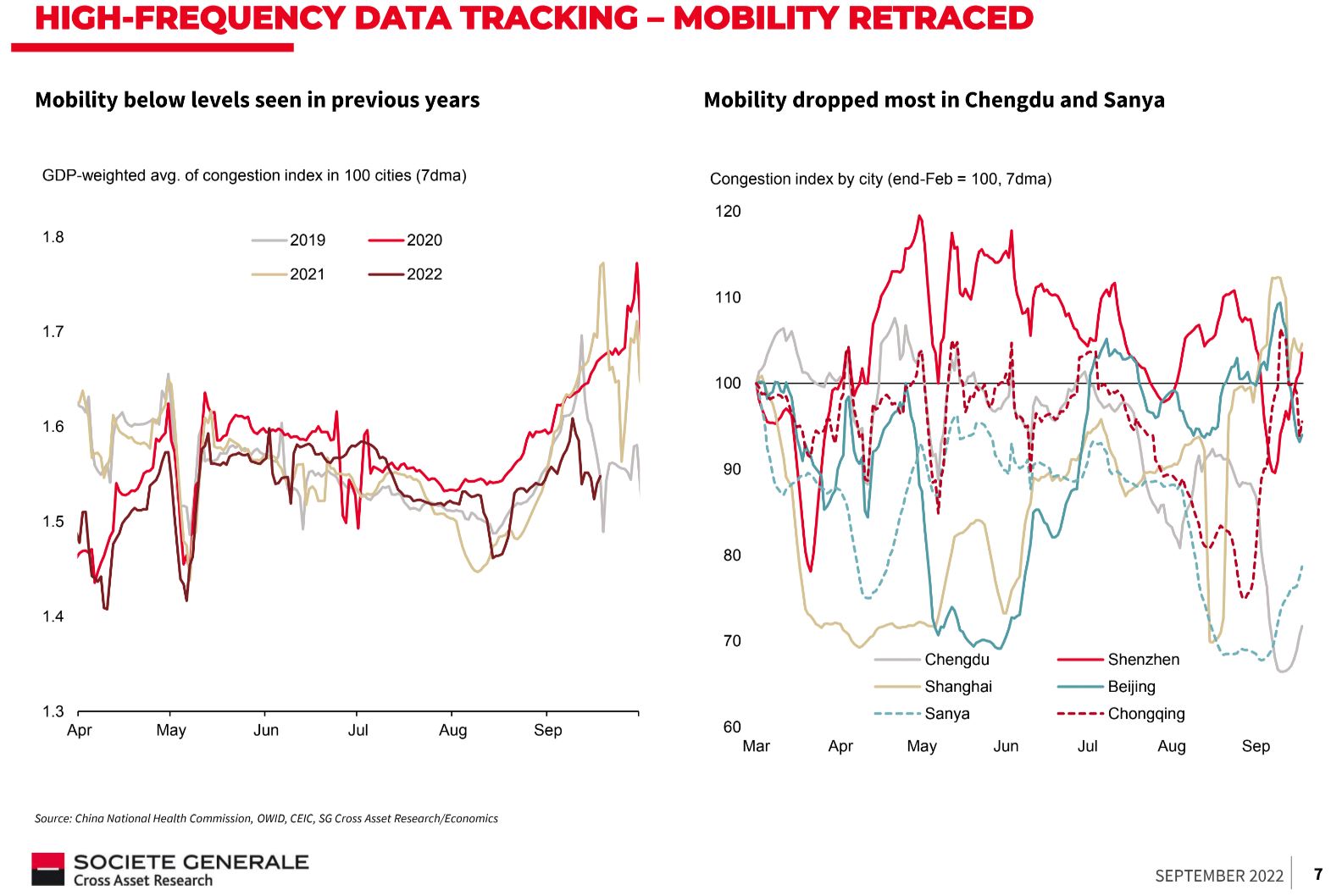

Mobility stuffed:

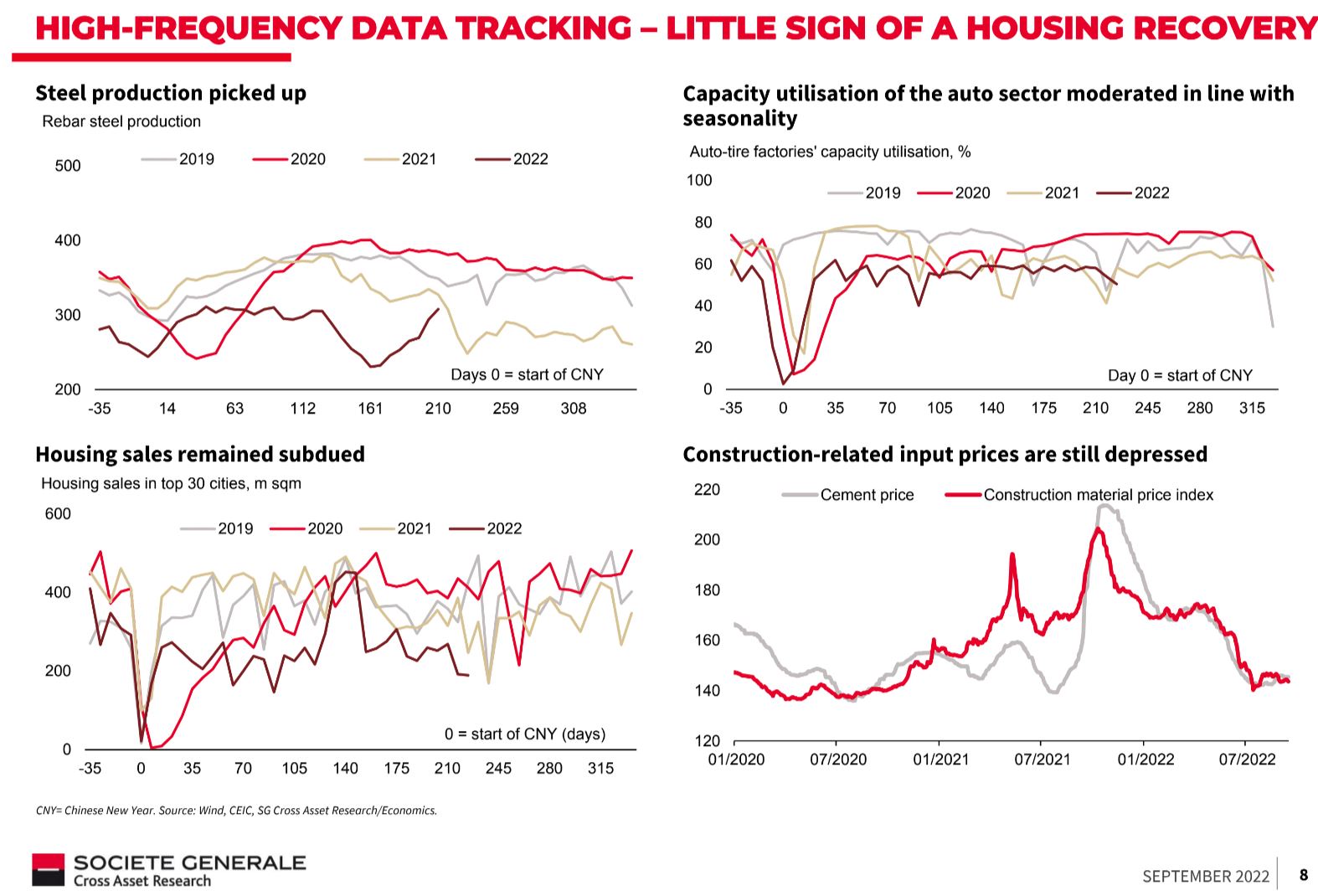

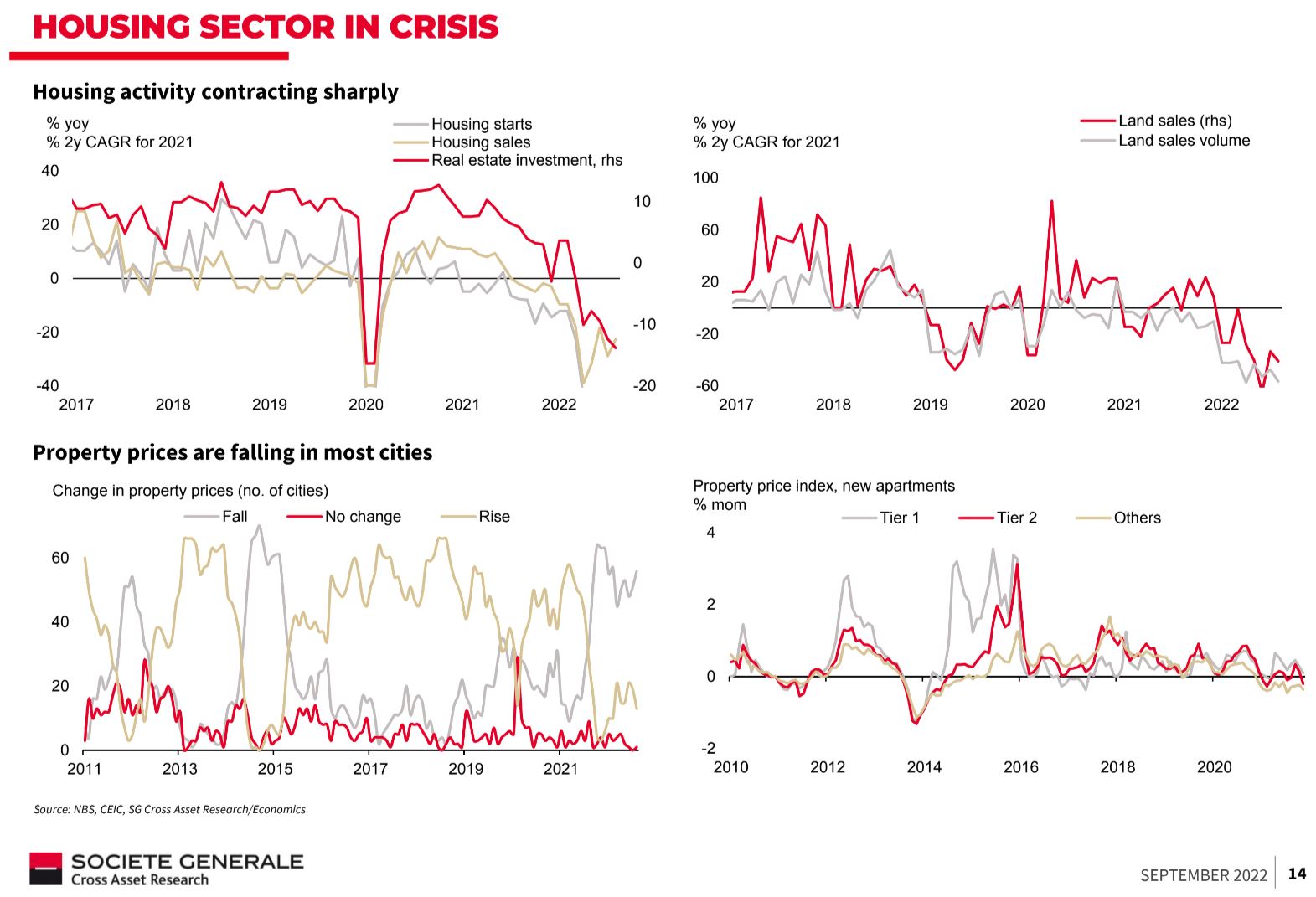

Property buggered:

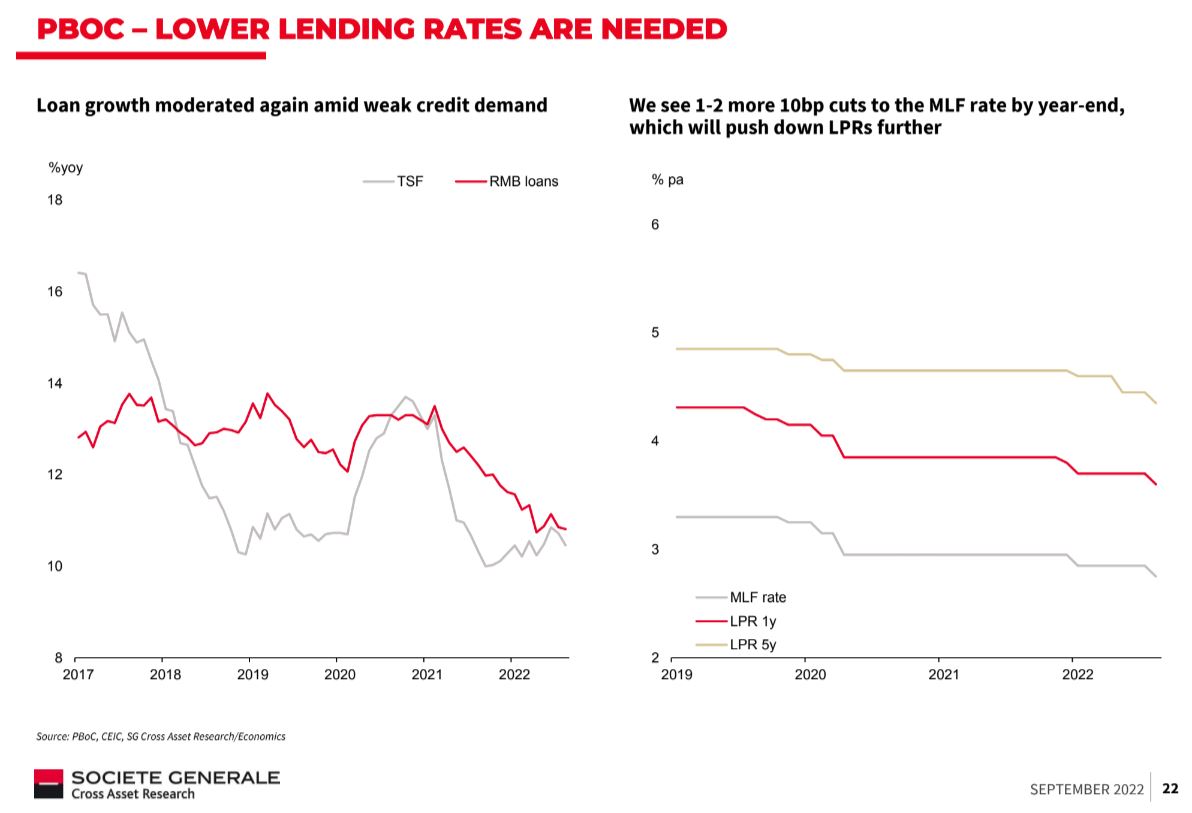

Liquidity trap:

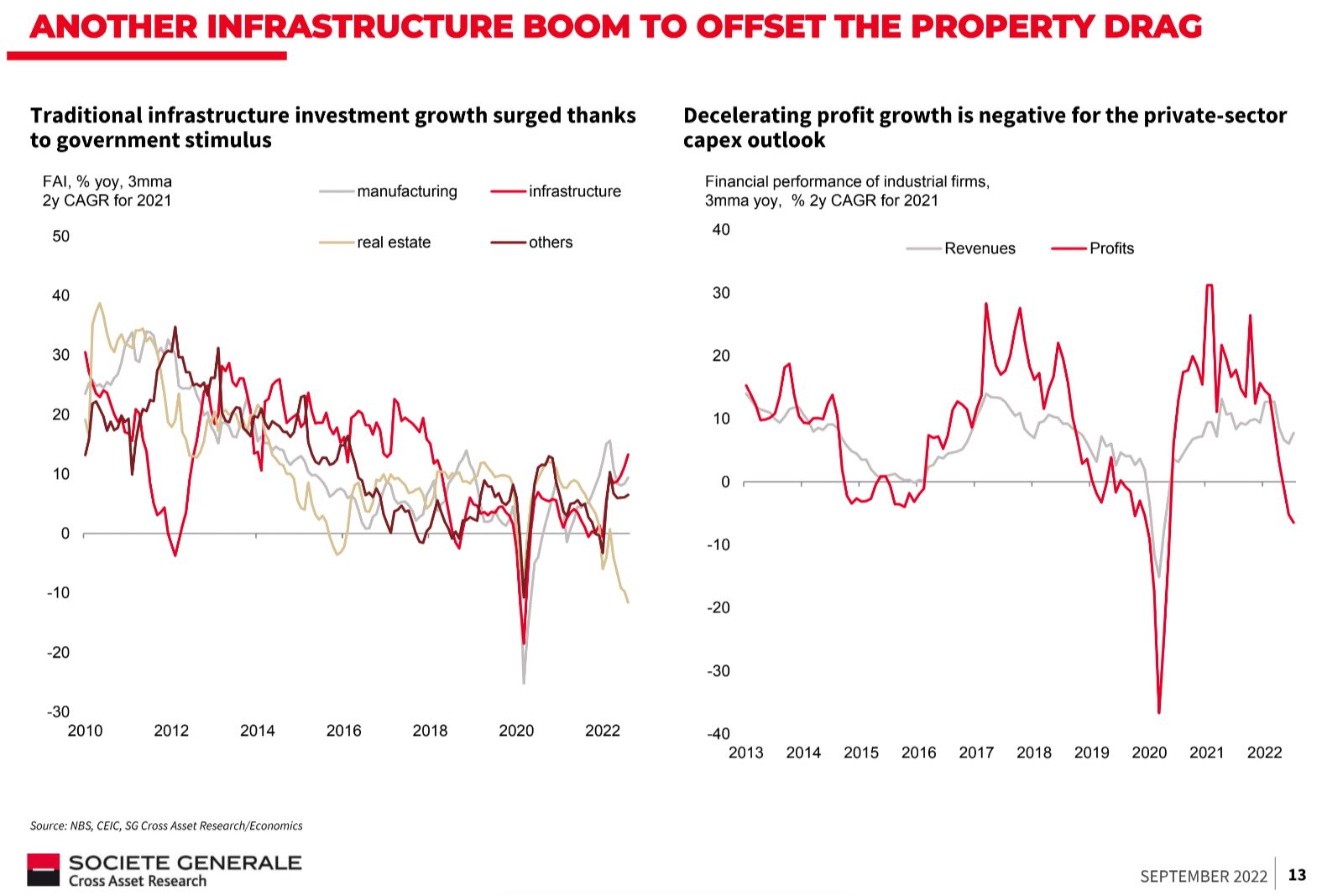

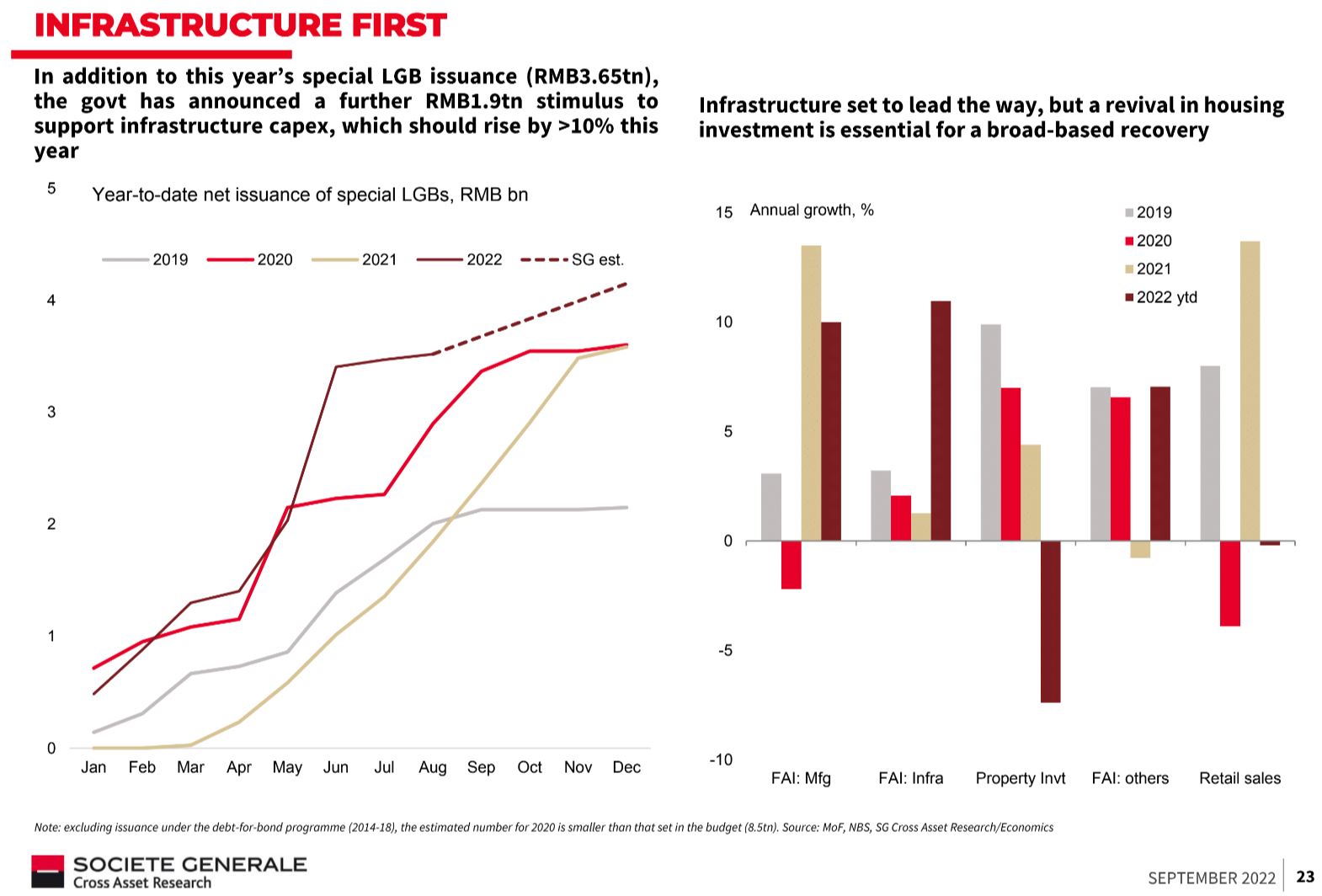

Bridges to nowhere an offset:

But not enough:

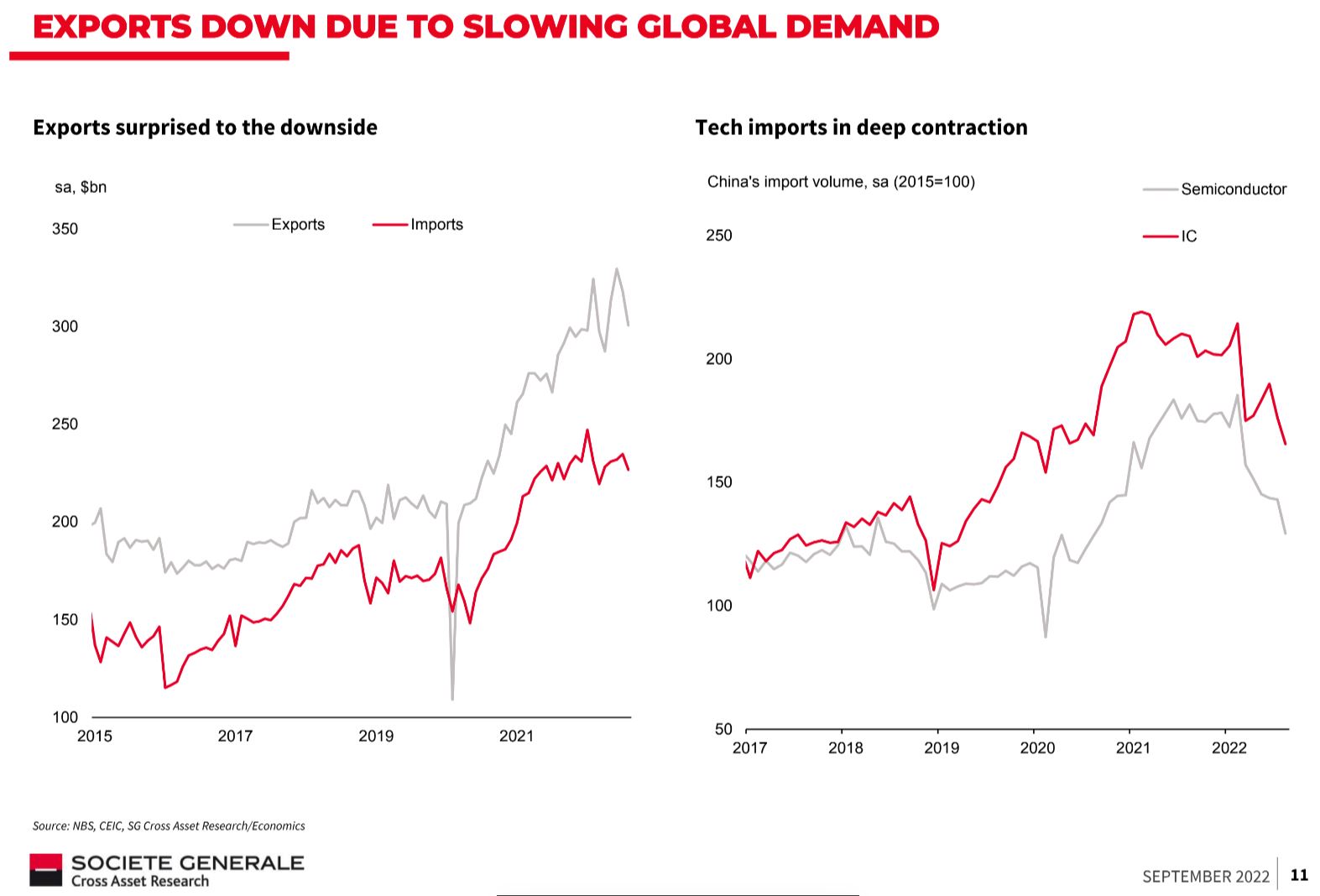

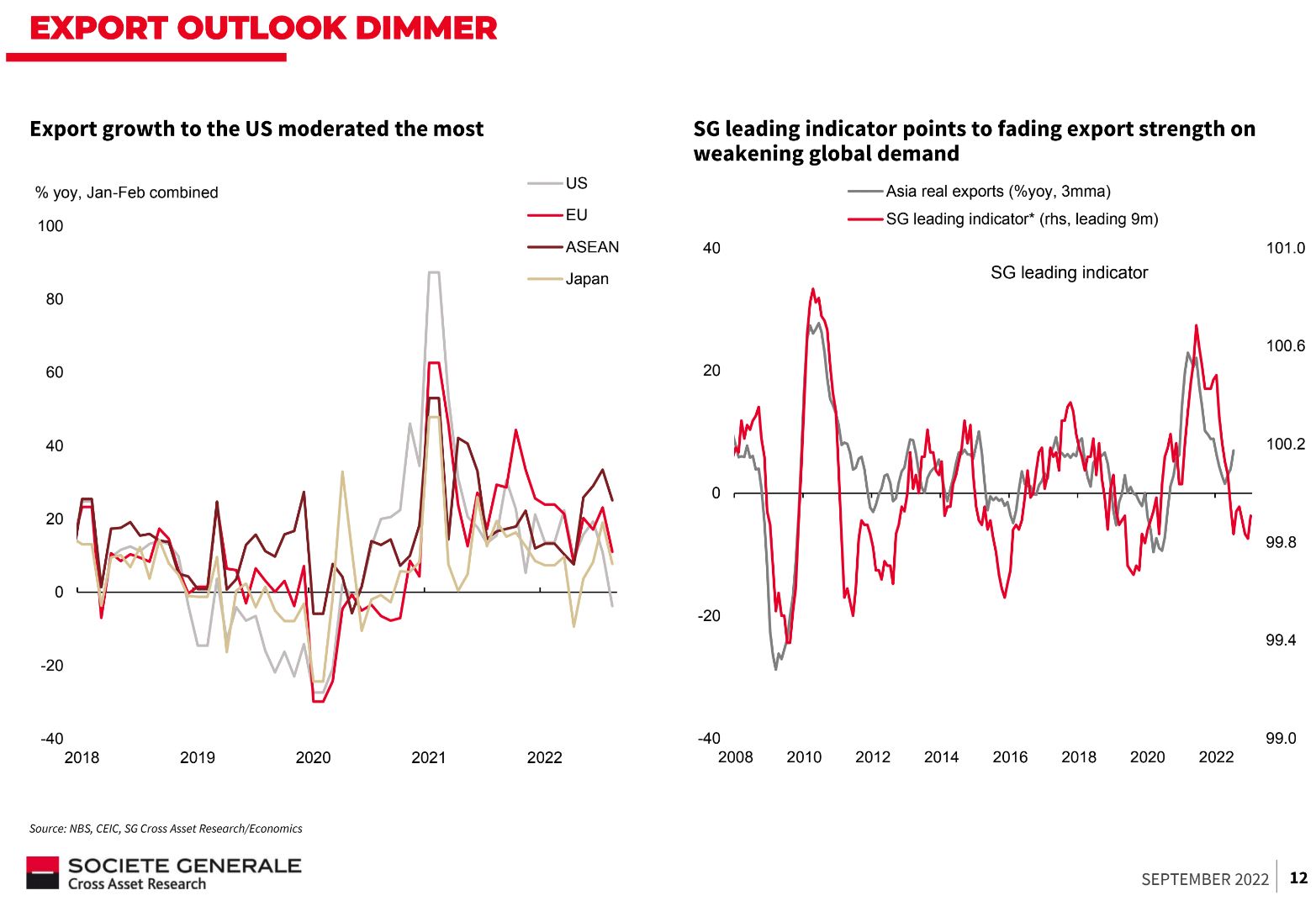

And an export shock just starting:

In 1989, Japan’s great catch-up development period ended in an immense real estate crash, liquidity trap, endless bridges to nowhere, and growth that shunted lower from 5% like clockwork to 2%.

Underneath all of those forces was another: demographics, which had turned nasty for Japan, and now the same has come to bear in China. Andy Xie sums it nicely:

China’s property bubble is deflating quickly. The vast industry and local governments are trying to revive it. But it won’t work. The sector is beset by developers’ financing woes and a massive supply overhang amid high household debt, a property affordability crisis and, crucially, a collapse in the rate of marriage.

…marriages plunged to a record low of 7.6 million last year, roughly half of the peak of 13.5 million in 2013. That year, 1.3 billion square metres of new residential properties – roughly 13 million flats – were sold, household debt was low at 16.6 trillion yuan (US$2.4 trillion), and grandparents were rich in savings. By last year, household debt had ballooned to 71.1 trillion yuan, over 140 per cent of disposable household income, and the grandparents had been bled dry.

…Marriage is the only significant driver of demand for property. With about 7 billion square metres in residential property under construction and unsold, if every marriage leads to a property purchase and the number of marriages doesn’t fall further, it would still take about 10 years to digest the inventory. Given that both assumptions are wildly optimistic, and that land banks, meanwhile, will only add to the inventory, it will be a long slog before the market returns to stability.

Decades of deflation, most obviously in commodity prices, followed Japan going ex-growth.

Now it is China’s turn.