Melbourne’s house price bust has hit a new milestone, according CoreLogic’s daily dwelling values index.

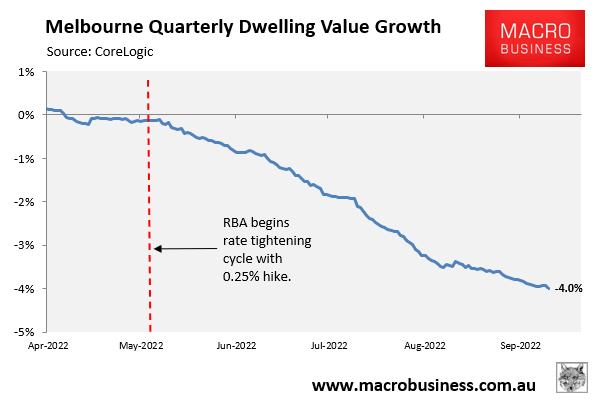

The quarterly rate of value decline accelerated to 4.0% as of 10 September – the fastest rate of decline since February 2019:

Fastest quarterly decline since February 2019.

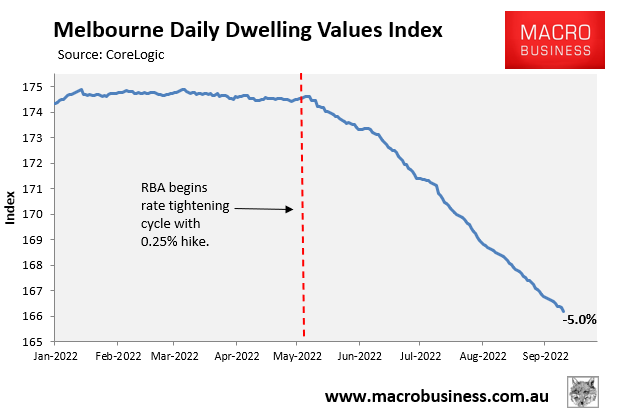

Melbourne’s peak-to-trough decline has now hit 5.0%, with 4.8% of that fall occurring following the Reserve Bank of Australia’s (RBA) first interest rate hike in early May:

Sharp price fall following RBA rate hikes.

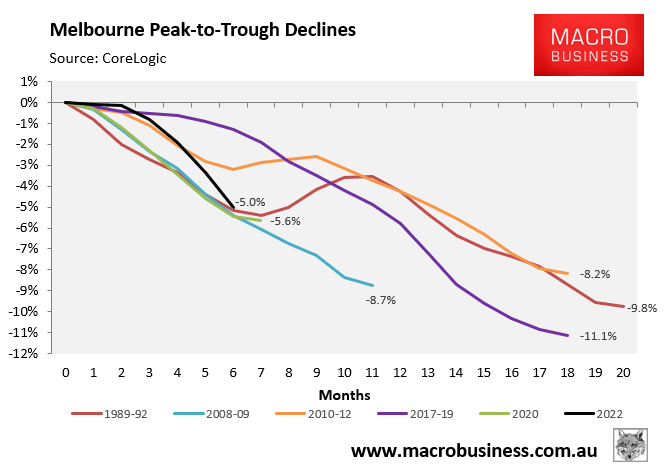

The following chart plots the current decline (shown in black) against prior price corrections using the CoreLogic index:

Current price decline will soon become Melbourne’s fastest on record.

Melbourne’s current 5.0% correction has a long way to go before it catches the major busts recorded in 2017-19 (11.1% over 19 months) and 1989-92 (9.8% over 21 months). However, the pace of decline six months in is on par with the three fastest prior episodes (i.e. 1989-92, 2008-09 and 2020). The current rate of decline is also accelerating, meaning it will soon overtake the prior episodes.

Ultimately, how far Melbourne house prices fall will depend on how aggressively the RBA hikes interest rates, given higher mortgage rates lower borrowing capacity and reduce housing demand.

In last week’s monetary policy statement accompanying the 0.5% rate hike, RBA governor Phil Lowe noted that “the Board expects to increase interest rates further over the months ahead” because inflation “is expected to increase further over the months ahead”.

As such, mortgage rates will continue to rise from here, which will further lower borrowing capacity and reduce home buyer demand. This will inevitably push house prices lower.

The bottom won’t arrive until after the RBA stops increasing rates, whenever that is.