RBA’s aggressive rate hikes kill home buyer demand

An article published at News.com.au claims that large numbers of prospective first home buyers have been eliminated from the market because of the Reserve Bank of Australia’s (RBA) aggressive interest rate hikes, which have shrunk borrowing capacity.

This has occurred because the Australian Prudential Regulatory Authority’s mortgage serviceability buffer is set at 3% over the presiding mortgage rate. Accordingly, as mortgage rates lift, prospective borrowers are re-rated at the higher interest rate, reducing how much they can borrow:

“Since the interest rates have gone up considerably over the past five months… the assessment rate for each bank has also risen,” [ICU Finance Group director Arlton D’Souza] said.

“On average, it’s about three per cent above the rate quoted, which could throw a lot of first-home buyers out of the market.”

Leading auctioneer, Tom Panos, made similar observations in yesterday’s YouTube stream:

“Every day, buyers are being re-rated which means they may have less purchasing power”…

“Every time there is a rate rise, borrowing capacity drops down”.

The reduction in borrowing capacity is easily illustrated via a mortgage calculator.

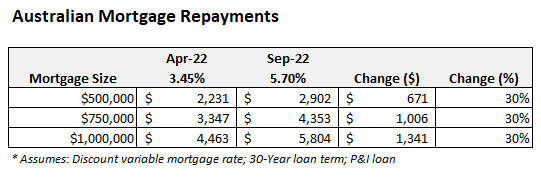

Before the RBA began hiking interest rates in early May, Australia’s average discount variable mortgage rate was 3.45%.

After last week’s 0.5% official cash rate increase, the discount variable mortgage rate will rise to 5.70%, which implies a 30% lift in mortgage repayments versus their level in April before the RBA’s first rate hike:

Australian mortgage repayments will rise 30% from their pre-tightening level.

Viewed another way, the increase in mortgage rates will reduce borrowing capacity by 30%, other things equal.

There is more pain to come, too, with last week’s RBA monetary policy statement noting “the Board expects to increase interest rates further over the months ahead”.

The above table illustrates why mortgage rates are the biggest short-term driver of house prices, and why the RBA’s aggressive monetary tightening will drive Australian house prices sharply lower.

Interest rate hikes raise the cost of debt, lower borrowing capacity and stifle buyer demand. It is as simple as that.